The architecture of the modern economy is being rebuilt in the cloud.

From the systems that power financial transactions and healthcare records to the infrastructure running artificial intelligence at scale, cloud computing has moved well beyond its origins as a data-storage convenience. It is now the foundational layer upon which enterprise technology, digital commerce, and national security increasingly depend.

At the centre of this transformation lies a diverse ecosystem of companies spanning digital security, e-commerce infrastructure, data architecture, internet infrastructure, and data support whose revenues are structurally tied to the expansion of cloud computing.

As enterprises digitise operations, governments modernise their systems, and AI workloads demand ever-greater compute resources, this ecosystem is positioned at the intersection of some of the most consequential technology trends of the decade.

The Themes Cloud Computing ETF (CLOD) is designed to provide exposure to companies positioned within this evolving segment of the technology landscape.

By attempting to provide diversified exposure to the 50 largest companies by market capitalisation that derive their revenues from digital security, e-commerce infrastructure, data infrastructure, data architecture, internet infrastructure, and data support, CLOD may allow investors to participate in the long-term structural trends shaping the global cloud computing market.

Key Takeaways

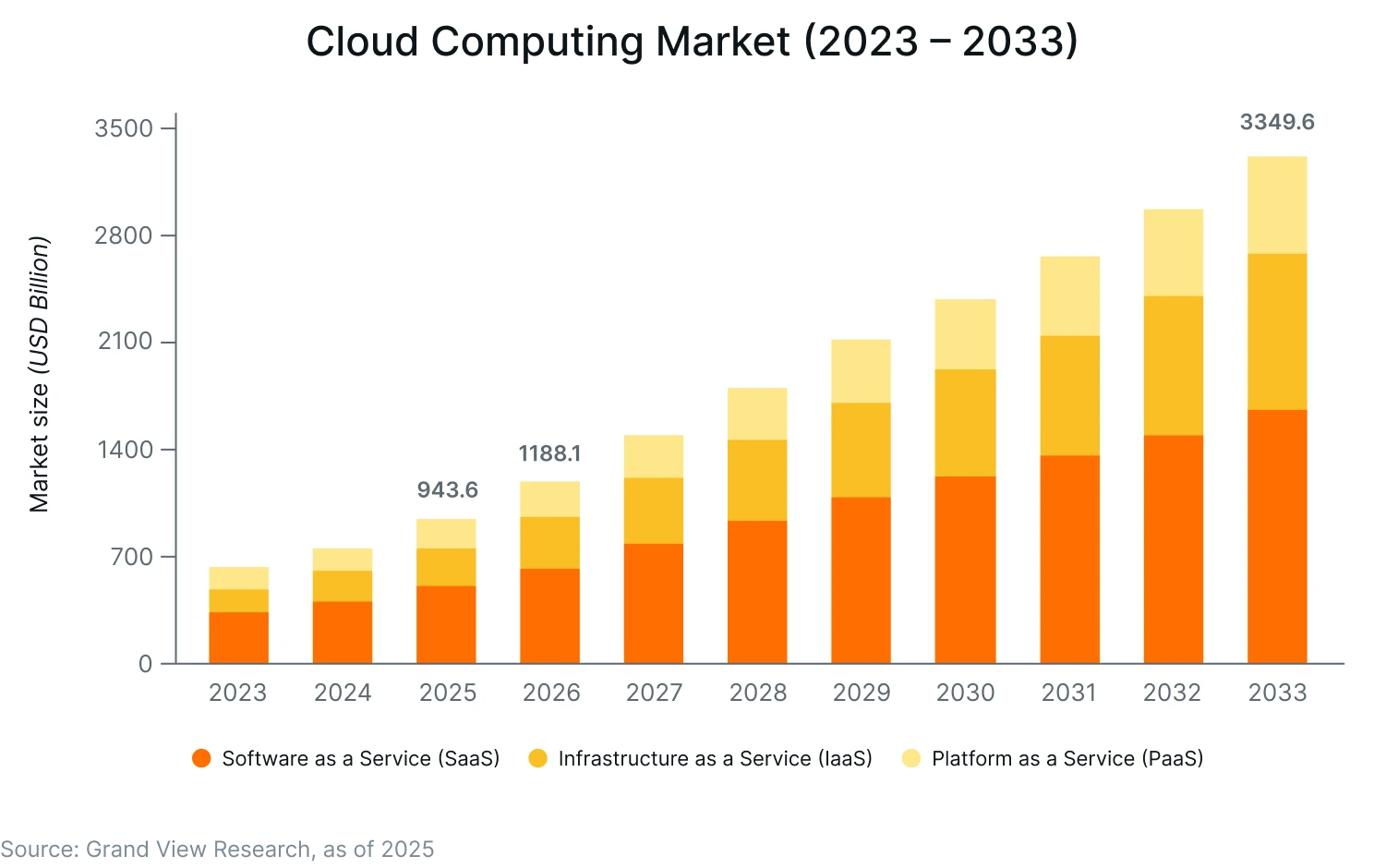

The global cloud computing market is projected to grow from US$943.6 billion in 2025 to US$3.35 trillion by 2033, highlighting the increasing scale and strategic importance of cloud infrastructure.

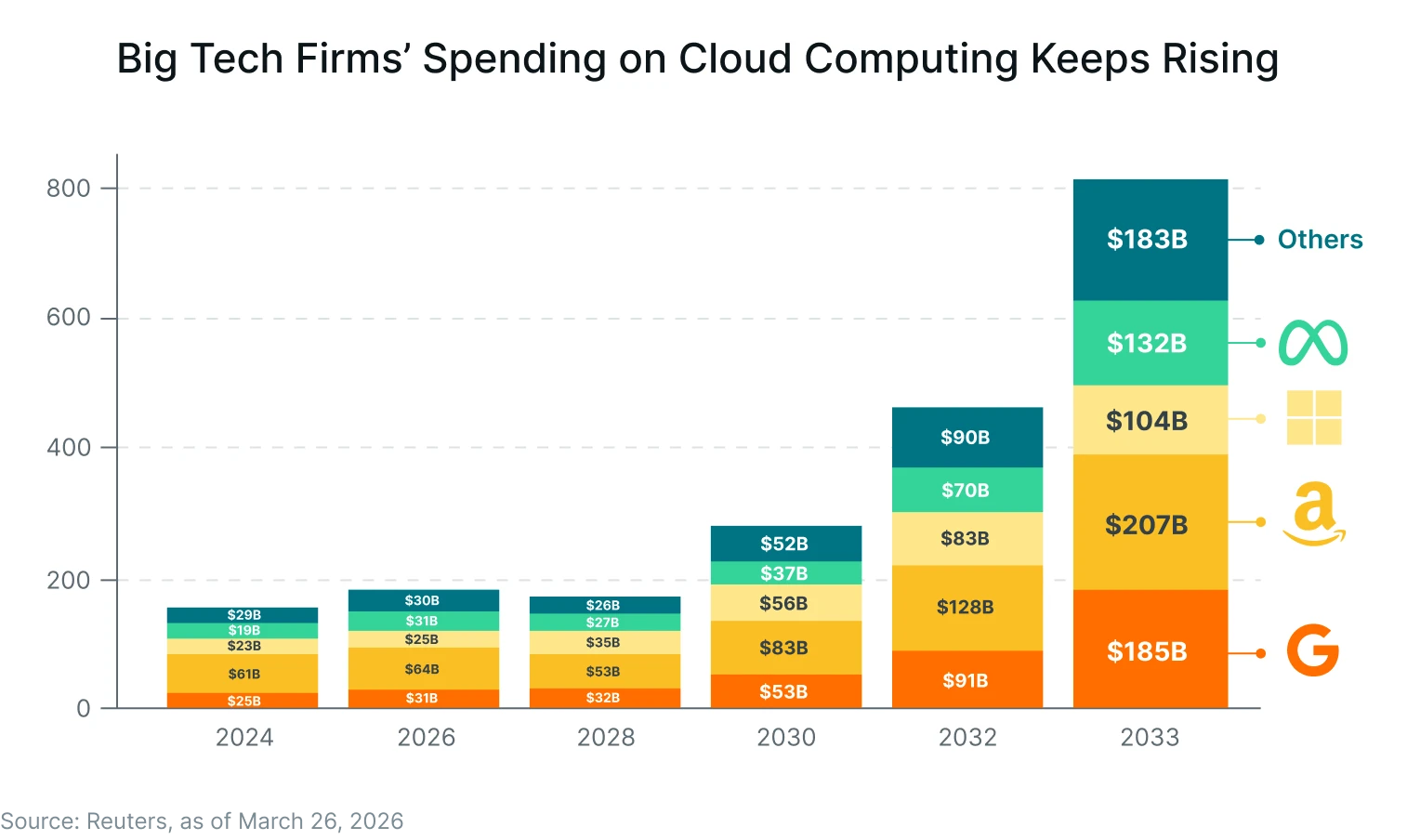

AI is accelerating cloud investment at an unprecedented pace, with Amazon, Microsoft, Alphabet, and Meta alone expected to spend approximately US$630 billion on data centres and AI chips in 2026.

Cloud adoption now extends across cybersecurity, e-commerce, data infrastructure, and AI-enabled enterprise software, creating a diversified ecosystem tied to long-term digital transformation trends.

#1 The Cloud Computing Market Has Reached Structural Scale

The most important context for understanding cloud computing as an investment theme is the scale it has already achieved, and the pace at which that scale continues to grow.

The global cloud computing market was estimated at US$943.65 billion in 2025 and is projected to grow at a CAGR of 16% to reach US$3.35 trillion by 2033, driven by the ongoing shift from legacy on-premise infrastructure to more scalable, flexible, and cost-efficient cloud environments.¹

What was once viewed as a disruptive technology layer has increasingly become foundational enterprise infrastructure, underpinning everything from data storage and cybersecurity to e-commerce, digital collaboration, and artificial intelligence.

That shift is evident in enterprise adoption trends. According to McKinsey, more than 95% of enterprise organisations now have a cloud footprint, while the share of enterprise workloads running in the public cloud has risen from 32% in 2018 to 52% in 2025.2

Public cloud consumption has also expanded sharply, growing from approximately US$ 90 billion in 2019 to US$335 billion in 2024.2 The market has therefore moved well beyond early-stage experimentation and into operational dependency, with cloud increasingly serving as the default architecture for enterprise IT.

The economic implications of this transition are becoming increasingly significant. Research published by AWS and Telecom Advisory Services estimated that cloud adoption contributed more than US$1 trillion to global GDP in 2023, with cumulative economic impact projected to exceed US$12 trillion between 2024 and 2030.3

Much of that expansion is expected to be driven by cloud-enabled AI applications, which require scalable compute, storage, and networking infrastructure that traditional on-premise systems often cannot efficiently provide.

The composition of cloud spending is evolving too. While Software as a Service (SaaS) remains the largest segment by revenue, Infrastructure as a Service (IaaS) encompassing compute, storage, and networking is emerging as the fastest-growing layer, supported by accelerating AI workloads and continued enterprise migration to the cloud.¹

What this data reflects is a market that has transitioned from disruption to infrastructure. Cloud computing is no longer competing with traditional IT for budget share. In most large enterprises, it is the IT strategy.

#2 AI Is Generating Unprecedented Infrastructure Investment

If the scale of the cloud market establishes the foundation, the AI infrastructure investment cycle is the catalyst accelerating it.

AI workloads from large-scale model training to real-time inference run predominantly on cloud infrastructure, and the race to develop and deploy AI at scale has triggered a capital commitment without precedent in the modern technology industry.

Just four companies - Amazon, Microsoft, Alphabet, and Meta, are projected to spend approximately US$ 630 billion on data centres and AI chips in 2026 alone, according to Morgan Stanley estimates.

That figure is more than four times the 2023 level, and is equivalent to roughly 2.2% of US GDP. They currently operate roughly 600 data centre facilities globally, with a further 544 in planning or under construction.⁴

Widening the lens to the top 11 cloud and infrastructure providers including Oracle and CoreWeave total 2026 capital expenditure reaches US$ 811 billion.⁴

McKinsey's analysis of this buildout puts the physical scale in context: US power capacity is projected to grow from approximately 30 GW in 2025 to more than 90 GW by 2030, a CAGR of approximately 22%.⁵

Hyperscalers are expected to capture around 70% of that capacity, with the remainder flowing to colocation providers, specialist infrastructure operators, and the broader ecosystem of companies building and powering these facilities.⁵

For the ecosystem of companies that design, build, connect, operate, and secure this infrastructure, the scale of committed capital represents a significant and durable revenue backdrop.

#3 Enterprise Digital Transformation is Making Cloud Infrastructure the Default

Infrastructure investment establishes the supply side of the cloud computing opportunity. What makes the theme structurally compelling over the long run is the demand side - the degree to which enterprise cloud adoption is deepening, delivering measurable returns, and expanding in scope with each new cycle of technology.

The evidence of deepening adoption is measurable. IBM's 2025 survey of 3,500 senior executives across ten EMEA countries found that 66% reported their organisations had already achieved significant operational productivity improvements from AI with software development and IT, customer service, and procurement leading the areas of measurable gain.6

Approximately one in five respondents said their organisation had already realised its AI ROI goals, with a further 42% expecting to do so within twelve months.6 These results describe enterprises that are not evaluating cloud-enabled AI as a future investment but managing its returns as a present-tense reality.

The same IBM survey found that 92% of senior executives expect agentic AI - systems that autonomously plan and execute multi-step tasks to deliver measurable ROI within two years.6

Agentic AI workloads are cloud-native by design: they require the elastic compute, real-time data access, and interconnected services that only cloud platforms can provide at scale. As adoption of these systems grows, the demand they generate for underlying cloud infrastructure scales with them.

Gartner captures this trajectory in concrete terms: 40% of enterprise applications will incorporate task-specific AI agents by end-2026, up from less than 5% in 2025.7

Each of those integrations deepens an enterprise's reliance on cloud-native platforms, data pipelines, and security frameworks and tends to generate demand for further cloud capability rather than less.

#4 Cybersecurity: A US$ 240 Billion Spend Growing in Step with Cloud Adoption

Cloud adoption and cybersecurity spending move together. Every workload migrated to the cloud, every application made accessible over the internet, and every user granted remote access creates a new potential vulnerability.

As cloud environments grow in scale and complexity, so does the market for securing them and that relationship shows up clearly in the data.

Gartner forecasts worldwide end-user spending on information security will reach US$240 billion in 2026, up from US$213 billion in 2025.8 That 12.5% year-over-year increase is being driven by three converging forces: a rising and increasingly sophisticated threat environment, the growing use of AI by both attackers and defenders, and regulatory pressure that has made security investment a compliance requirement rather than a discretionary budget line.8

The AI dimension of this dynamic is particularly relevant for the cloud computing ecosystem. As enterprises deploy AI across their cloud environments, they introduce new attack surfaces that require new forms of defence from securing AI model inputs and outputs to protecting the data pipelines that feed them.

Gartner's forecast reflects that expanding scope: security spending is not simply growing in absolute terms, it is growing because the perimeter that needs to be secured is expanding with every new cloud workload and every new AI integration.

For the cloud computing investment theme, digital security represents one of the most structurally stable revenue streams within the ecosystem. Companies providing identity management, threat detection, cloud access security brokering, and compliance automation generate revenues that are contractual, recurring, and tied directly to enterprise cloud usage volumes.

As cloud environments become more complex and AI more deeply embedded, the demand for cloud-native security solutions scales alongside them making security spending not a separate consideration but an intrinsic cost of cloud operations.

#5 The Cloud Value Chain Offers Diversified Structural Exposure

One of the distinguishing features of cloud computing as an investment theme is the breadth of its value chain.

Rather than concentrating exposure in a single platform or product cycle, the cloud ecosystem spans six distinct revenue-generating segments each benefiting from the same underlying growth drivers but generating revenue through different business models, serving different customers, and responding to different parts of the technology stack.

Data Infrastructure encompasses the storage, compute capacity, and data centre hardware that underpins everything else. As inference workloads become the dominant form of AI compute, requiring distributed, lower-latency facilities closer to end users, the geographic footprint of data infrastructure investment broadens alongside the opportunity.⁵

Data Architecture covers the platforms, databases, orchestration tools, and analytics systems through which organisations extract intelligence from their data. As enterprises operate across hybrid and multi-cloud environments and integrate AI into their workflows, the tooling required to manage, govern, and move data across those environments becomes progressively more critical.

Internet Infrastructure content delivery networks, DNS providers, networking hardware, and interconnection services forms the physical and logical layer over which cloud services reach users.

McKinsey's analysis notes that as hyperscalers expand into tier 2 markets to access power more quickly, power can be secured 12 to 24 months faster than in constrained tier 1 hubs, at land costs up to 70% lower.⁵ This geographic expansion broadens the infrastructure opportunity and the range of companies that benefit from it.

E-Commerce Infrastructure provides the payment gateways, logistics platforms, fulfilment systems, and merchant tooling that underpin digital retail a sector that relies entirely on cloud-based systems to manage transaction volumes, inventory in real time, and increasingly personalised customer experiences.

Digital Security and Data Support complete the ecosystem. Security, as explored in the previous section, generates recurring revenue tied structurally to enterprise cloud usage and is forecast to reach US$240 billion in 2026.8

Data support encompasses the monitoring, compliance, backup, and operational continuity services that cloud environments require to function reliably at enterprise scale.

Taken together, these six segments present an opportunity that does not require concentrating exposure in a single winner. They are all participants in the same long-run structural expansion operating under different revenue models, serving different customers, but collectively tied to the same fundamental drivers.

How to Play It

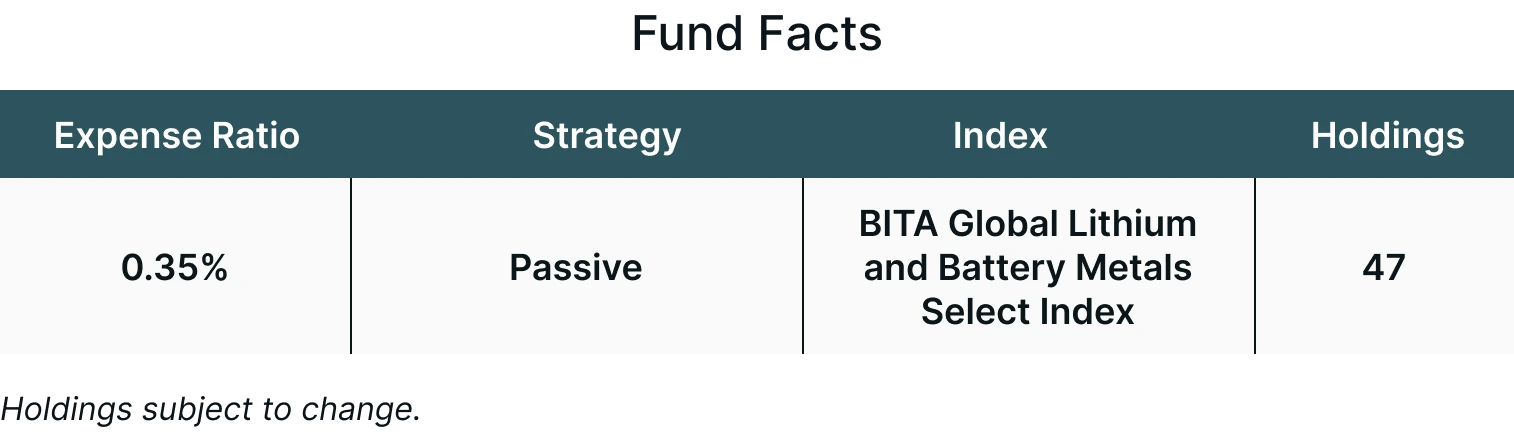

The Themes Cloud Computing ETF (CLOD) seeks to track the Solactive Cloud Computing Index (SOLCLOUN), which identifies the largest 50 companies by market capitalization that derive their revenues from digital security, e-commerce infrastructure, data infrastructure, data architecture internet infrastructure, and data support.

CLOD seeks to provide investment results that correspond generally to the price and yield performance, before fees and expenses, of the SOLCLOUN Index.

Conclusion

Cloud computing has moved well beyond its origins as a cost-efficiency tool for enterprise IT. It now sits at the centre of a broader structural transition reshaping how businesses store data, deploy applications, secure digital systems, and integrate artificial intelligence into everyday operations.

The scale of investment flowing into the sector reflects this shift. Hyperscalers, semiconductor firms, cybersecurity providers, and data infrastructure companies are collectively deploying capital at levels rarely seen in the technology industry, driven by sustained demand for computing power, storage, connectivity, and AI-enabled services.

At the same time, enterprise cloud adoption remains uneven across industries and geographies, suggesting that the transition is still unfolding rather than fully mature.

Near-term constraints including energy availability, supply chain bottlenecks, and the operational challenges of scaling infrastructure globally are likely to influence the pace and distribution of growth. Yet these constraints exist alongside continued expansion in data creation, AI workloads, digital commerce, and enterprise digitisation, all of which reinforce the strategic importance of cloud infrastructure.

For investors, the theme offers exposure to a technology ecosystem that increasingly underpins both digital innovation and real-world economic activity, positioning it as one of the more consequential infrastructure layers of the modern economy.

For more information about the fund, including fees/expenses, holdings, standardized performance, risks and more, please visit https://themesetfs.com/etfs/clod.

Footnotes:

*Diversification does not eliminate risk. Investors cannot directly invest in an index.

1Grand View Research, Cloud Computing Market Size & Share Analysis 2026–2033, 2025

2McKinsey & Company, Riding the Hyperscaler Wave: The Investment Opportunity in Cloud Ecosystems, as of September 19, 2025

3Amazon Web Services & Telecom Advisory Services, Cloud Adoption and AI: Economic Impact Studies, as of November 26, 2024

4Reuters Breakingviews (Karen Kwok), How Big Tech's $630 Bln AI Splurge Will Fall Short, as of March 26, 2026

5McKinsey & Company, The Next Big Shifts in AI Workloads and Hyperscaler Strategies, as of December 17, 2025

6IBM, The Race for ROI: Two-thirds of EMEA Enterprises Report Significant Productivity Gains from AI, as of October 28, 2025

7Gartner, Gartner Predicts 40% of Enterprise Apps Will Feature Task-Specific AI Agents by 2026, as of August 26, 2025

8Gartner, Gartner Forecasts Worldwide End-User Spending on Information Security to Total $213 Billion in 2025, as of July 29, 2025

Article by Ayesha Shetty

Author is a contractor of Leverage Shares LLC, a U.S. affiliate of Themes Management Company LLC. Leverage Shares LLC provides certain services to Themes under an intercompany services agreement.