Few investment sectors have undergone as dramatic a reassessment as global aerospace and defense over the past four years. For much of the post-Cold War era, defense budgets in Western Europe stagnated as governments prioritized social spending in a relatively stable security environment.

That era has come to an abrupt end. Russia's full-scale invasion of Ukraine in February 2022, combined with China's sustained military build-up and a broader deterioration in the global rules-based order, has forced a fundamental rethink of defense posture across the North Atlantic Treaty Organization (NATO) alliance.

The financial implications of this strategic shift are profound. Governments across 32 NATO member states are committing to spend more on defense, and dramatically more on a decade-long trajectory expected to inject trillions of additional dollars into defense budgets.

For investors, this creates a confluence of policy-driven demand, technological innovation, and financial stability not seen very often in any industrial sector.

In our view, the Transatlantic Defense ETF (NATO) is designed to provide exposure to this structural shift in global defense spending, capturing companies that are positioned to benefit from rising procurement budgets, modernization programs, and evolving security priorities across the alliance.

By attempting to provide diversified exposure to aerospace and defense companies headquartered in North Atlantic Treaty Organization (NATO) member countries, NATO allows investors to participate in the sector’s evolving dynamics.

Key Takeaways

NATO commitments and sustained geopolitical tensions are driving multi-year increases in military budgets, shifting the sector from cyclical to structurally supported growth.

Institutional allocations and investor participation are expanding rapidly, reflecting growing recognition of defense as a long-duration investment theme.

#1 Unprecedented Surge in NATO Defense Spending

The single most powerful investment driver for NATO-aligned defense companies is the historic commitment to increased defense spending made by alliance members.

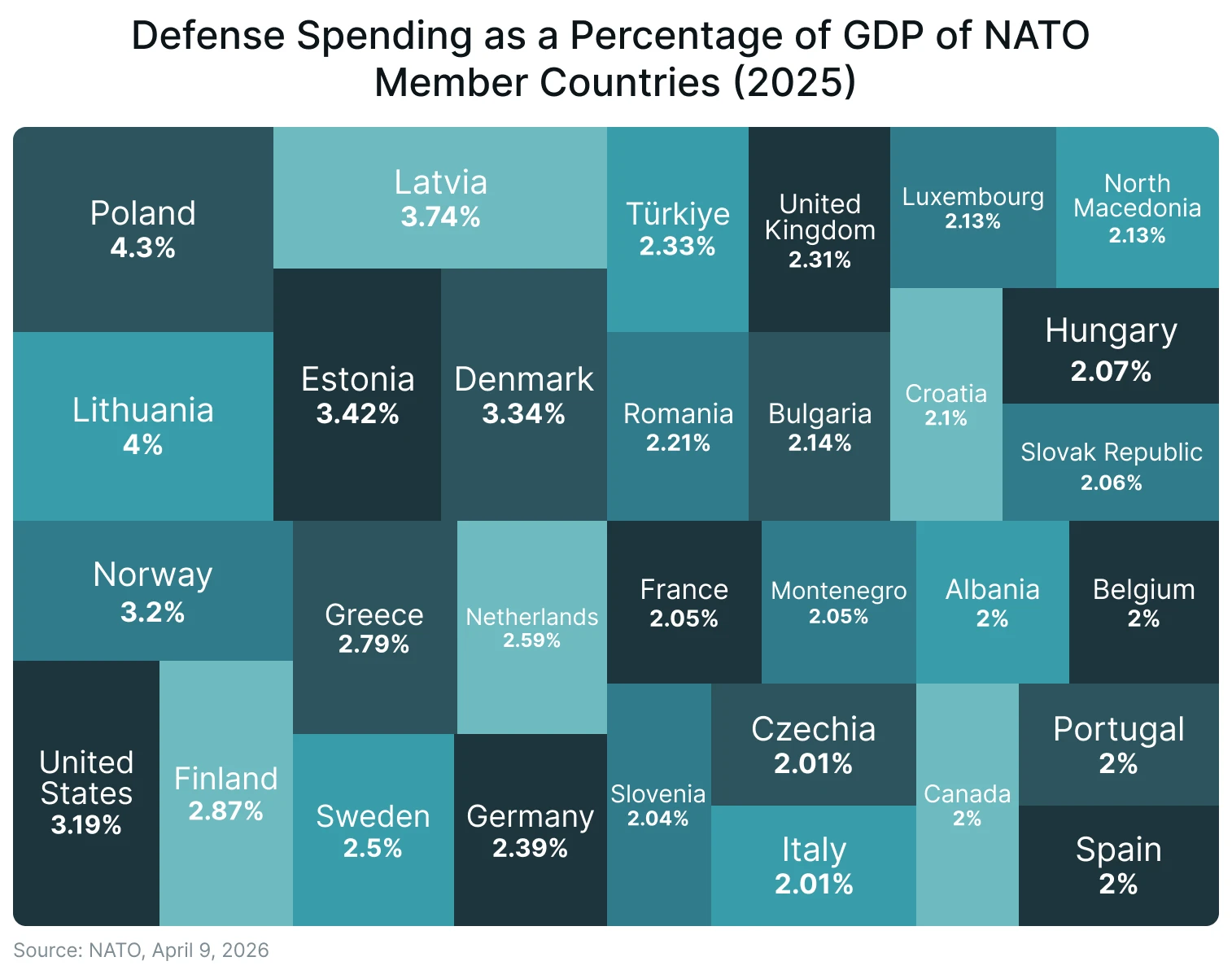

In 2025 alone, European allies and Canada increased defense spending by 20% from the previous calendar year, with all allies now exceeding the previous defense spending target of 2% of GDP. For the first time in recorded NATO history, a European ally, Norway, surpassed the United States in defense spending per capita.1

More significant is the commitment made at the June 2025 NATO Summit in The Hague. NATO allies committed to investing 5% of GDP annually on core defense requirements and defense-and security-related spending by 2035, allocating at least 3.5% of GDP on core defense requirements and meeting NATO Capability Targets. European allies and Canada invested a combined total of more than USD 574 billion (adjusted to 2021 prices) in defense in 2025.2

The scale of additional investment required is staggering. Based on GDP projections, if all NATO allies met the 3.5% target in 2035, they would need to allocate around US$ 1.4 trillion more in annual military spending than they did in 2024, putting total NATO annual military spending at US$ 2.9 trillion.3

The 5%-of-GDP level will comprise at least 3.5% of each ally's GDP to be spent on core defenses, including equipment and personnel, and 1.5% of their GDP toward civil preparedness, defense innovation, and other security priorities. The funding commitment is expected to add US$ 1 trillion to NATO's defense resources annually when reached by 2035.4

For investors, these are not aspirational political statements, they are codified government budget commitments with legal and parliamentary backing in many member states. Poland has become NATO's top defense spender by GDP, with plans to reach 4.7% in 2025.5

#2 Sustained Geopolitical Demand as a Structural Growth Driver

Defense spending is ultimately a function of perceived threat. The current security environment provides near-certainty that demand for defense equipment and services will remain elevated for at least a decade.

As Russia has poured resources into funding its invasion and ongoing operations, NATO allies have sought to boost their own defense capabilities in light of the threat on their borders.6

The threats are concrete and ongoing: in September 2025, Russian drones and planes violated the airspace of Estonia, Finland, Latvia, Lithuania, Norway, Poland, and Romania, prompting NATO to launch Eastern Sentry, an enhanced vigilance activity bolstering its eastern flank posture.7

Meanwhile, Russian sabotage attacks in Europe tripled between 2023 and 2024, targeting defense facilities, logistics hubs, and critical infrastructure across Germany, Poland, and the Baltic states.8 In response, Poland launched its US$2.5 billion East Shield defensive network spanning 700 kilometers along its borders with Russia and Belarus.9

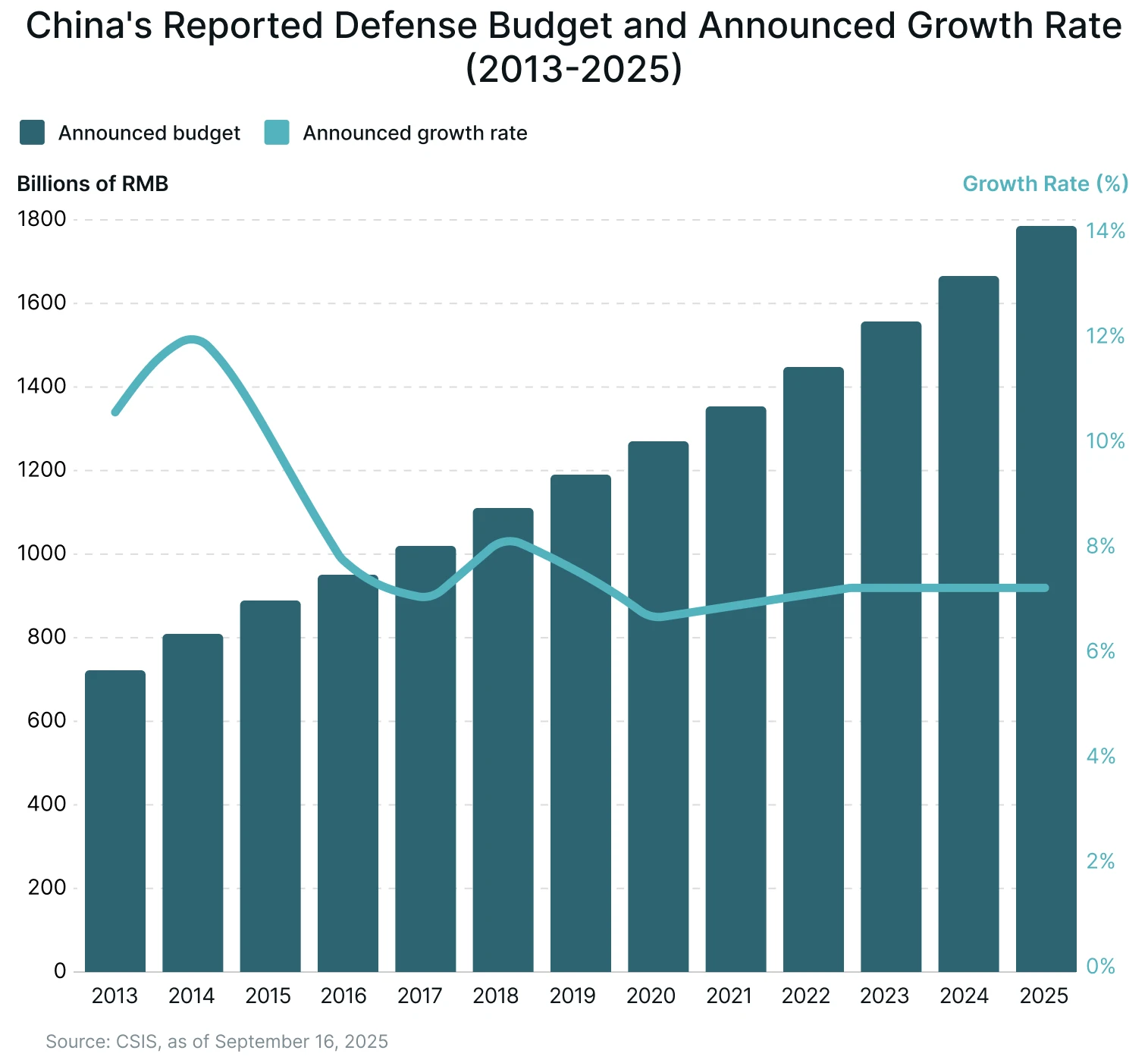

Russia is not the only driver. China announced a 7.2% increase in its defense budget for 2025, the tenth consecutive year of uninterrupted growth, bringing planned expenditure to approximately US$ 249 billion.10 Over the past decade, China's defense spending has increased by over 50%, averaging roughly 8% annual growth and funding a sustained build-up of advanced missile systems, fighter jets, and naval vessels.11

Apart from this, the Council on Foreign Relations rates both a Taiwan Strait crisis and a Russia-NATO clash as having an even probability of occurring in 2026, each with the potential to draw the United States into direct military conflict.12 Doubts about the credibility of NATO's Article 5 guarantee have further accelerated pressure on European states to invest independently in their own defense.13

For investors, this threat environment reflects more than a short-term spike. With global defense spending having crossed US$ 2.6 trillion and major program backlogs extending close to a decade, it points to a defense spending environment that appears structural rather than cyclical in nature.14

#3 An Expanding and Structurally Protected Defense Equipment Market

The same geopolitical pressures driving NATO’s spending surge are also determining who captures that spend.

The structural advantages have been built over decades. Established contractors are already integrated into alliance platforms, logistics systems, and command structures, making them the default choice as European militaries accelerate modernization.

The scale of demand is significant, and accelerating.

Arms imports by European states have more than tripled (+210%) between 2016–20 and 2021–25, making Europe the largest destination for global arms imports, accounting for 33% of total global demand. Within NATO, procurement remains highly concentrated: the 29 European NATO member states increased arms imports by 143% in 2021–25, with the United States accounting for 58% of those imports.15

This concentration is not incidental, it reflects structural dependence. The United States remains the dominant global supplier, accounting for 42% of total arms exports, with Europe emerging as its largest export market for the first time in two decades.15 Procurement decisions are therefore anchored in long-standing transatlantic defense relationships rather than purely competitive dynamics.

Forward order pipelines further reinforce this positioning. European countries had 466 F-35 combat aircraft on order or preselected for order as of end-2025, underscoring the long-term lock-in of supplier relationships and platform ecosystems.15

Policy direction is now amplifying this structural bias. The European Defence Industrial Strategy sets a target for at least 40% of defence equipment procurement to be conducted collaboratively by 2030, reinforcing intra-alliance sourcing and further concentrating spending within NATO-aligned industrial ecosystems.16

For investors, the implication is clear: this is not just a growing market, but a structurally protected one. NATO-country defense companies are not merely benefiting from higher budgets, they are embedded within procurement systems that favour trusted, certified, and interoperable suppliers.

These advantages create high barriers to entry, limit competitive disruption, and ensure that incremental spending disproportionately accrues to established players.

#4 Revenue Stability Through Long-Term Government Contracts and Backlogs

One of the most distinctive financial characteristics of aerospace and defense companies and one that sets them apart from most industrial sectors is the structural predictability of their revenue, derived from multi-year government contracts and large order backlogs.

The sector's resilience is underpinned by long-term contracts and predictable revenue streams, particularly in defense, while commercial aerospace benefits from pent-up demand for new aircraft and supply chain stabilization.

Due to the industry's nature, which involves long-term contracts, large-scale government agreements, and complex project fulfilment timelines, the order backlog can represent several years' worth of work providing investors with visibility into a company's future revenue, cash flow, and profit potential.

The scale of current backlogs illustrates this vividly, with full-year 2025 results across major NATO-country primes setting successive records. Lockheed Martin ended 2025 with a record backlog of US$ 194 billion roughly 2.5 times its annual sales generating free cash flow of US$ 6.9 billion, with its CEO describing 2025 as a year of "unprecedented demand."17

RTX Corporation closed 2025 with a total backlog of US$ 268 billion, including US$ 107 billion tied to defense programs, on full-year sales of US$ 88.6 billion, up 10% year-on-year, with free cash flow of US$ 7.9 billion, up US$ 3.4 billion from the prior year.18

This revenue visibility translates directly into shareholder returns. General Dynamics raised its quarterly dividend by 5.6% following its record 2025 backlog announcement, extending an uninterrupted streak of 27 consecutive years of dividend payments.19

Lockheed Martin reported full-year 2025 net earnings of US$ 5 billion, or US$ 21.49 per share, supported by 6% year-over-year sales growth and free cash flow well above prior expectations.17

#5 Expanding Institutional Capital Flows

The broadening of the institutional investor base for aerospace and defense companies represents a structural shift in how capital is being allocated to the sector, one that is visible and measurable in fund flow data across both public and private markets.

US investors are seeking to capitalise on a world engulfed in conflict, increasing exposure to the defense industry in a bet on surging military spending in the coming years. Annual commitments by U.S. public pension plans to defense-focused private equity funds have more than doubled between 2022 and 2025.20

The trend has continued into 2026, with commitments to defense-focused funds rising at a double-digit pace in the first quarter, even as allocations to the broader private equity market continued to decline.

US-listed defence-focused exchange traded funds have reported net inflows of US$ 4.8 billion in the first quarter this year, up from US$ 283 million a year earlier and outflows of US$ 0.15 million two years ago.20

In Europe, a parallel expansion is underway. Assets under management in defense-themed mutual funds and ETFs registered for sale in Europe have grown from €1.8 billion at end-2024 to €16.5 billion by October 2025, a nearly ninefold increase in under a year, with March 2025 recording the highest single-month net inflow of €2.5 billion on record since the first defense-themed product launched in October 2017.21

How to Play It

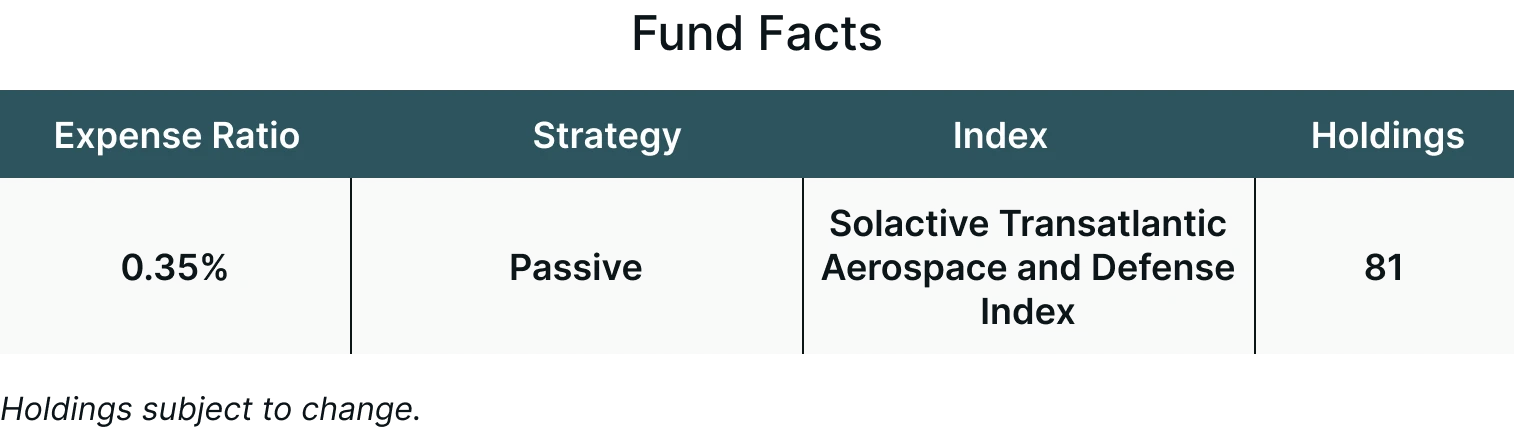

The Themes Transatlantic Defense ETF (NATO) seeks to track the Solactive Transatlantic Aerospace and Defense Index (SOLNATON), which identifies aerospace and defense companies headquartered in North Atlantic Treaty Organization (NATO) member countries.

NATO seeks to provide investment results that correspond generally to the price and yield performance, before fees and expenses, of the SOLNATON Index.

Conclusion

Rising geopolitical tensions and formal defense commitments are reshaping aerospace and defense into a structurally supported growth sector, with spending not only increasing but becoming more durable as governments prioritize long-term military readiness.

In this environment, the sector offers a compelling combination of structural growth and earnings visibility, underpinned by long-term contracts and robust order pipelines.

Even so, the pace and durability of this growth will depend on policy direction, procurement execution, and the evolving global security landscape.

Assessing how these dynamics translate into sustained contract flow and expanded industrial capacity will be key to understanding the durability of this cycle.

Ultimately, the sector’s long-term trajectory will be defined not just by the scale of spending, but by how effectively it is converted into deployable capability.

For more information about the fund, including fees/expenses, holdings, standardized performance, risks and more, please visit https://themesetfs.com/etfs/nato.

Footnotes:

*Diversification does not eliminate risk. Investors cannot directly invest in an index.

1Atlantic Council, NATO Defense Spending Tracker, April 9, 2026

2NATO, Defence Expenditures and NATO’s 5% commitment, as of April 10, 2026

3SIPRI, NATO’s new spending target: challenges and risks associated with a political signal, as of June 27, 2025

4Share America, New Defense Spending Strengthens NATO, as of August 12, 2025

5European Parliamentary Research Service, EU Member States' Defence Budgets, as of May 2025

6CSIS, Defense Budgets in an Uncertain Security Environment, as of September 16, 2025

7NATO, Strengthening NATO’s Eastern Flank, as of October 23, 2025

8NATO, Deterrence on NATO’s Eastern Flank, as of November 17, 2025

9Military.com, Germany to Construct Defenses in Poland, Deploy More Troops to Lithuania as Russian Threat to NATO Grows, as of December 17, 2025

10The State Council, The People’s Republic of China, China to increase defense budget by 7.2 percent in 2025, marking single-digit growth for 10th year, as of March 05, 2025

11American, Enterprise Institute, China’s Defense Budget Has Only One Trajectory: Up, as of March 08, 2024

12Council on Foreign Relations, Conflicts to Watch in 2026, as of December 2025

13Chatham House, Global security continued to unravel in 2025. Crucial tests are coming in 2026, as of December 12, 2025

14United Nations, The True Cost of Peace

15SIPRI, Trends In International Arms Transfers, 2025, as of March 2026

16European Parliament, European defence industrial strategy, as of September 2024

17Lockheed Martin, Lockheed Martin Reports Fourth Quarter and Full Year 2025 Financial Results, as of January 29, 2026

18RTX, RTX Reports 2025 Results and Announces 2026 Outlook, as of January 27, 2026

19Yahoo Finance, How Record Backlog and Dividend Hike At General Dynamics (GD) Has Changed Its Investment Story, as of February 15, 2026

20Financial Times, US investors boost defence exposure as global wars fuel spending boom, as of April 19, 2026

21LSEG, Defence-Themed ETFs and Mutual Funds: Hype or Real Investment Opportunity?, as of December 11, 2025

Article by Ayesha Shetty

Author is a contractor of Leverage Shares LLC, a U.S. affiliate of Themes Management Company LLC. Leverage Shares LLC provides certain services to Themes under an intercompany services agreement.