Article by Ayesha Shetty

Why Lithium & Battery Metals?

April 14, 2026 | Industry / Commodity Producers

The global energy system is undergoing a structural shift. Electrification is accelerating across transport, power, and industry, while digital infrastructure - from AI data centres to cloud computing - demands increasingly reliable energy storage.

At the centre of this transformation lies a group of materials that are rapidly moving from niche inputs to strategic resources: lithium and battery metals.

Once primarily used in consumer electronics, lithium has become a foundational component of modern energy systems. Alongside nickel, cobalt, and graphite, it forms the backbone of rechargeable batteries that power electric vehicles (EVs), stabilize renewable energy grids, and enable portable electronics.

As demand scales across multiple sectors simultaneously, lithium is becoming more deeply embedded within the systems driving this transition.

The Themes Lithium & Battery Metal Miners ETF (LIMI) is designed to provide exposure to companies positioned within this evolving segment of the energy landscape.

By attempting to provide diversified exposure to companies engaged in lithium and battery metals mining, explorations, refining, and royalties, LIMI may allow investors to participate in the long-term structural trends shaping the lithium and battery metals market.

Key Takeaways

Lithium is emerging as a core material in the energy transition, with demand extending beyond electric vehicles into power systems, storage, and digital infrastructure, supported by rising policy focus and industrial investment.

The trajectory of the lithium market will depend not only on demand growth, but on how supply chains evolve, how quickly new capacity comes online, and how investors access the sector across an increasingly integrated value chain.

#1 Electrification Is Driving Demand Growth

The most important shift in lithium demand today is being driven by electrification. What was once a niche material used in ceramics, lubricants, and pharmaceuticals has become a core input into energy systems, as electric vehicles scale and reshape the demand profile for battery metals.

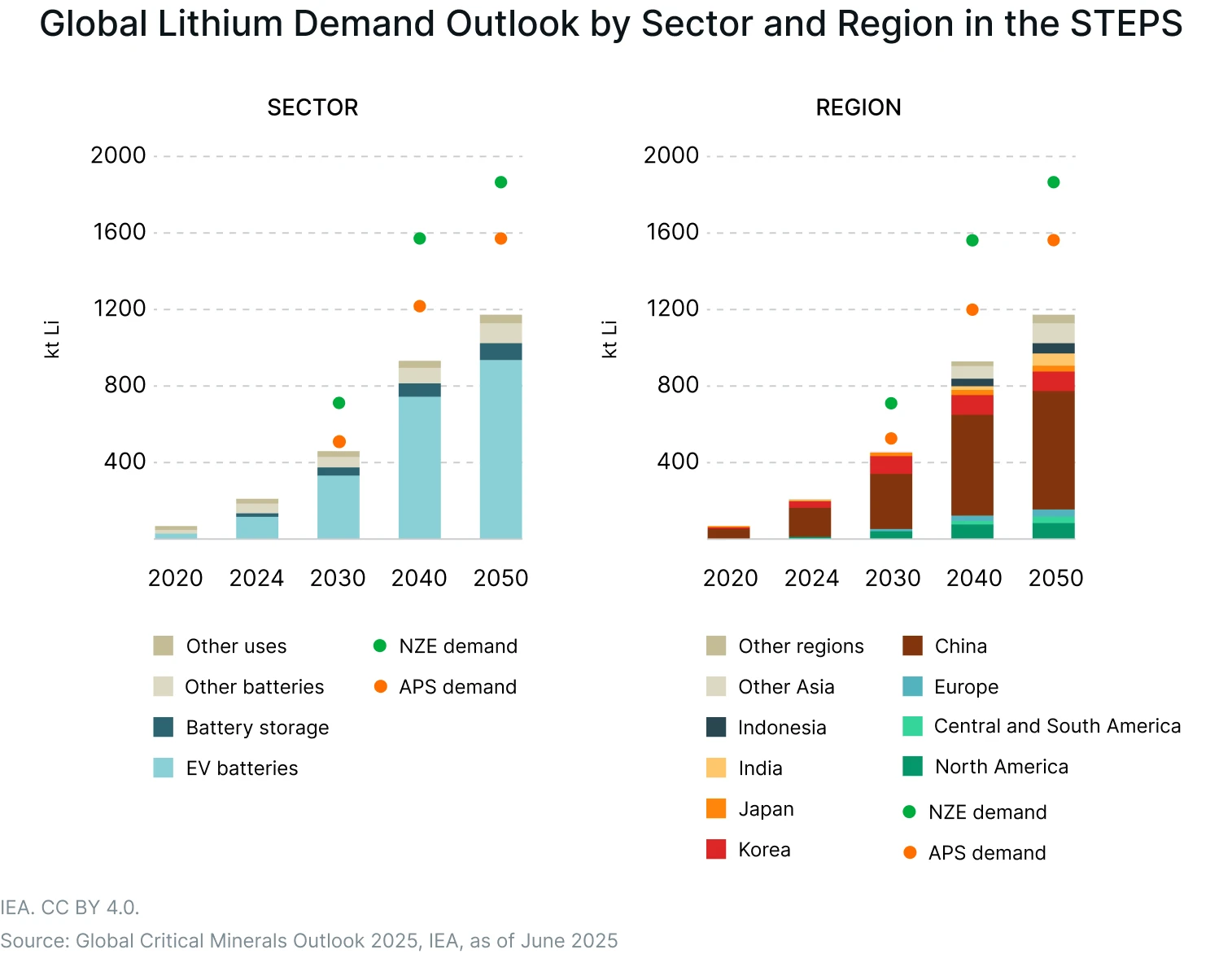

This transition is already visible in the data. According to the International Energy Agency, lithium demand rose by nearly 30% in 2024, far exceeding the growth rates seen in the previous decade.1

Electric vehicles remain the largest contributor to this shift. As EV adoption has increased across major markets, battery production has expanded alongside it. Each vehicle requires a meaningful quantity of lithium, and larger battery capacities have contributed to higher material intensity per unit. This combination has increased total lithium requirements beyond what would be implied by unit growth alone.

The scale of change is evident over a longer timeframe. Lithium demand has tripled since 2020, rising from around 60 kt to over 200 kt in recent years.1 Under IEA’s stated policy scenarios, demand reaches approximately 700 kt by 2035, with electric vehicles accounting for a substantial share of incremental demand.1 Across this period, electrification-related applications account for the majority of demand growth, indicating a shift in how lithium is consumed across sectors.1

This demand profile is also geographically concentrated. China currently accounts for a significant share of global lithium consumption, supported by its position in battery and cathode manufacturing. Other regions, including Japan and Korea, also contribute meaningfully.

Over time, additional regions, including the United States, Europe, and parts of Asia, are expected to increase their participation in battery manufacturing, contributing to a broader distribution of demand.

Taken together, these trends reflect a change in the underlying drivers of lithium demand. Lithium is increasingly embedded in the build-out of electrified systems, and its demand trajectory is closely tied to the pace of that transition. While near-term market dynamics may fluctuate, the underlying direction of travel is being set by the scale and speed of global electrification.

#2 Energy Storage Is Expanding Lithium’s Demand Base

While electric vehicles remain the largest source of lithium demand, energy storage systems are emerging as an additional and increasingly visible component of consumption. As renewable energy penetration increases across power systems, storage is being deployed to manage variability, balance supply and demand, and support grid stability.

Battery energy storage systems (BESS) store surplus electricity during periods of excess generation and release it when demand rises, enabling intermittent sources such as solar and wind to be integrated more effectively into power systems.2

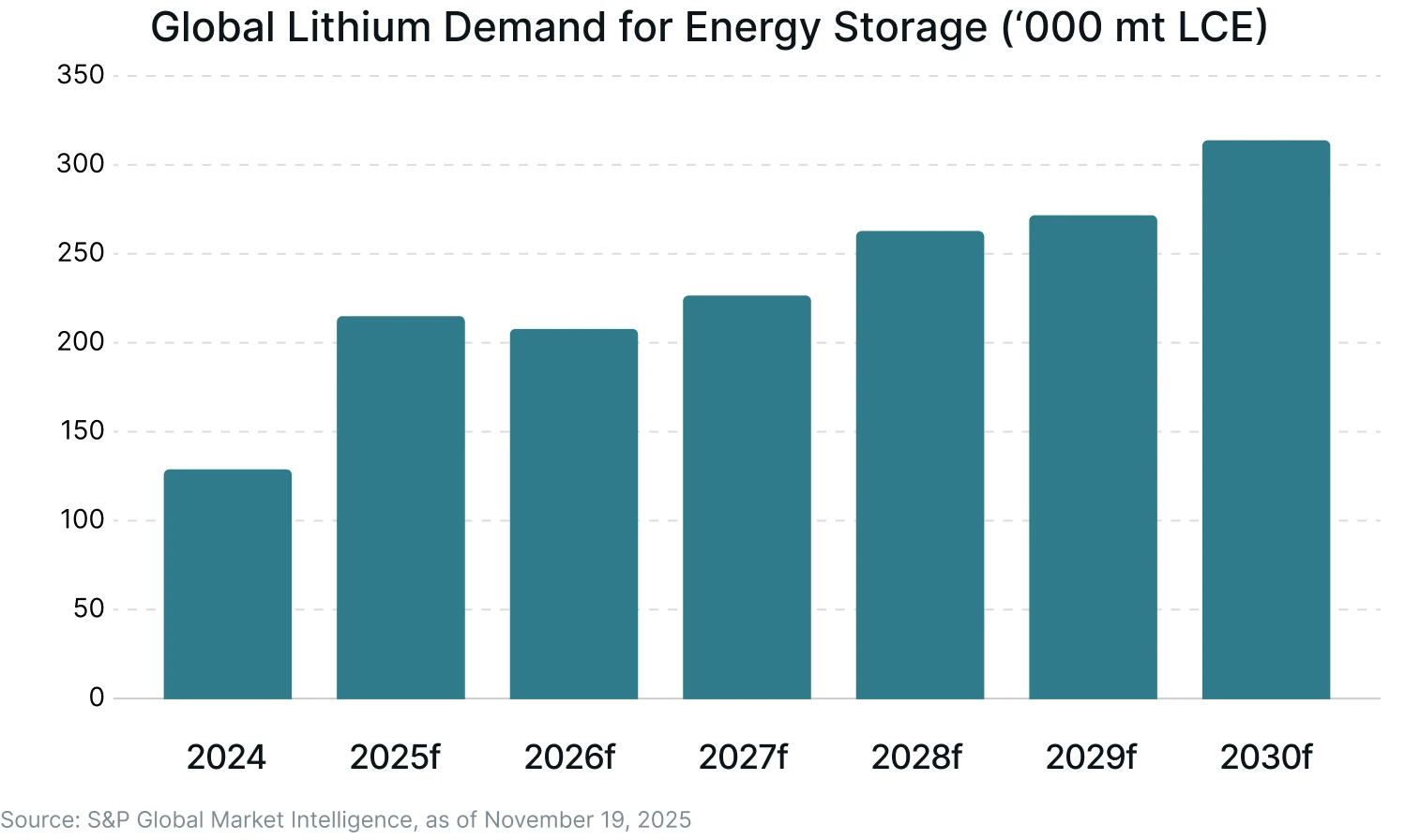

This functional role has translated into measurable demand growth. Lithium consumption for energy storage is forecast to increase by as much as 90% year over year to 380,000 mt in 2025, according to an estimate by Albemarle, the world's largest lithium producer.2

At a regional level, deployment trends have been uneven but pronounced. In the United States, energy storage installations increased by over 140% year-on-year through much of 2025, reflecting rising electricity demand and investment in grid resilience.2 Additional demand has also been linked to the expansion of data centres and digital infrastructure, which require stable and continuous power supply.

Looking ahead, S&P Global estimates lithium demand from energy storage at around 209,000 tonnes in 2026, before increasing to approximately 312,000 tonnes by 2030, implying a ~45% increase over the period.2

At the same time, near-term demand remains sensitive to policy changes and installation cycles. Global storage installations are expected to decline by 2.7% in 2026, largely due to changes in Chinese policy, which previously supported a significant share of global deployment.2

#3 Strategic Investment and Industrial Alignment Are Reshaping the Lithium Ecosystem

As demand for lithium expands across electric vehicles and energy systems, the focus is increasingly shifting towards how this demand is supported through investment and supply chain development. Alongside these demand drivers, lithium markets are being shaped by long-term strategic investment and industrial alignment.

Governments and corporations are taking a more active role in securing access to lithium, reflecting its growing importance within energy systems and supply chains. In North America, policy support for domestic supply has become more visible. In 2025, the U.S. government took a 5% stake in Lithium Americas’ Thacker Pass project, one of the largest lithium deposits globally, alongside financial support for its development.3 This follows broader efforts to support domestic mining and reduce reliance on external supply chains.

At the same time, capital is entering the sector from outside traditional mining. Energy companies including Chevron and Exxon Mobil have acquired acreage in lithium-rich regions such as the Smackover Formation, while oilfield services firms like Halliburton are exploring lithium extraction technologies, including geothermal-based production.4 These developments indicate a widening set of participants across the lithium value chain.

In Europe, policy support is also shaping supply development. Germany has committed over €100 million to advance domestic lithium production, including support for projects such as Vulcan Energy’s geothermal lithium initiative.5 This reflects broader efforts to localise supply and support battery manufacturing ecosystems.

These investments are occurring alongside a broader expansion of downstream capacity. Battery manufacturing continues to scale across regions, supported by both public funding and private capital. In the United States alone, over 30 gigafactories are planned, under construction, or operational by 2025, reflecting a significant increase in domestic battery capacity.4

These developments show how growing demand is being matched by capital, policy support, and supply chain buildout, linking lithium more closely to broader industrial and energy systems.

#4 Tightening Supply Dynamics

As lithium demand broadens beyond transport into power systems, supply dynamics reflect both rapid capacity expansion and emerging constraints across mining and refining. For investors, this interaction between growing demand and constrained supply is a key factor shaping market outcomes.

The current project pipeline indicates a material increase in output. Announced projects suggest global lithium production could double by 2030, supported by both new mines and larger-scale operations, with median project output rising from around 1,900 tonnes to approximately 2,700 tonnes of lithium.1

At the same time, supply remains geographically concentrated. Australia, Chile, and China account for a dominant share of global production, with additional reserves concentrated in Argentina and Zimbabwe.1

Despite this expansion, scaling supply presents challenges. Project development timelines, capital requirements, and infrastructure constraints influence how quickly new supply can be brought online. Under base-case assumptions, supply is expected to remain above primary demand into the late 2020s, before requiring additional project development to meet projected demand levels.1

Independent estimates suggest that under accelerated transition scenarios, supply-demand balances could tighten later in the decade, requiring substantial incremental investment in mining and refining capacity.6

Recent market indicators reflect these dynamics. Battery-grade lithium carbonate prices rose to around US$24,000 per metric ton in early 2026, following earlier declines, alongside tightening inventories and continued demand from transport and energy applications.7 This reflects how shifts in supply conditions can influence pricing over shorter timeframes.

Supply chains are also shaped by concentration in processing capacity. China processes the majority of hard-rock concentrate, reinforcing its role in downstream conversion.1 Efforts to diversify supply chains are underway, but refining capacity remains more concentrated than upstream production.6

Geopolitical factors add another layer to supply dynamics. Resource concentration, combined with trade policies and strategic investments, influences how lithium is produced, processed, and distributed across regions.6

For investors, these dynamics point to a market where supply constraints, project execution, and geographic concentration can influence pricing and availability, particularly as demand continues to scale across energy and transport systems.

#5 Investor Access Is Expanding Across the Lithium Value Chain

As lithium markets evolve, investor access is also broadening, reflecting the increasing integration of lithium across the energy and industrial ecosystem. Exposure to lithium is no longer limited to upstream mining companies, but extends across refining, battery manufacturing, and diversified industrial participants.

At the upstream level, listed mining companies provide direct exposure to lithium production, with operations concentrated in regions such as Australia, Chile, and emerging markets like Argentina.1 However, access to lithium is not uniform, as many assets are controlled by a relatively small group of producers and, in some cases, state-linked or privately held entities.

Midstream and downstream segments offer additional points of access. Lithium refining and chemical processing, dominated by a limited number of players, particularly in China, represent a critical part of the value chain, linking raw material extraction to battery production.1

Further downstream, battery manufacturers and component suppliers provide indirect exposure, with demand tied to electric vehicles, energy storage, and broader electrification trends.

The investment landscape has also expanded through market-linked instruments. Exchange-traded funds (ETFs) and thematic strategies now provide diversified* exposure to lithium and battery metals, spanning multiple segments of the value chain. These vehicles allow investors to participate in the broader ecosystem without relying on single-asset or single-company exposure.

At the same time, access remains shaped by structural factors. Geographic concentration, ownership structures, and supply chain integration influence how capital flows into the sector. In some cases, strategic investments and long-term supply agreements between automakers, battery producers, and mining companies limit the availability of material through open markets.

How to Play It

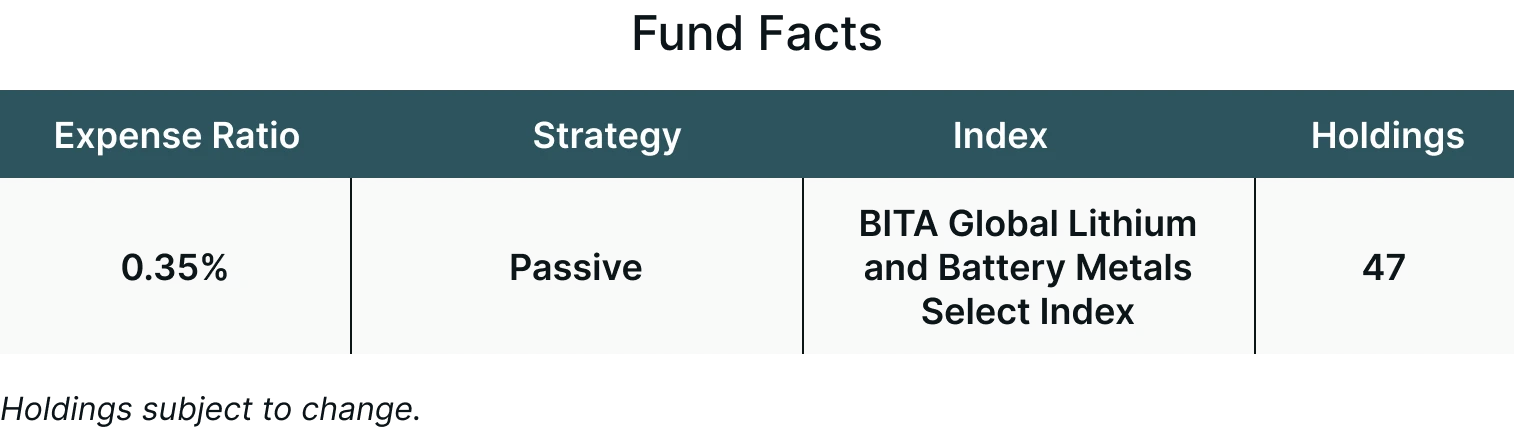

The Themes Lithium & Battery Metal Miners ETF (LIMI) seeks to track the BITA Global Lithium and Battery Metals Index (BGLISI), which identifies companies that derive their revenues from lithium and battery metals mining, explorations, refining, and royalties.

LIMI seeks to provide investment results that correspond generally to the price and yield performance, before fees and expenses, of the BGLISI Index.

Conclusion

Lithium is increasingly tied to the broader shift towards electrification, with demand linked not just to individual end markets, but to the expansion of energy systems, transport, and digital infrastructure.

As these systems scale, battery metal is expected to become embedded within the underlying architecture rather than remain a standalone commodity, connecting it more closely to long-term economic and technological trends.

For investors, exposure to lithium reflects participation in these structural shifts, but the outcome remains linked to how demand evolves across sectors, alongside the influence of policy frameworks, pricing cycles, and supply chain development.

For more information about the fund, including fees/expenses, holdings, standardized performance, risks and more, please visit https://themesetfs.com/etfs/limi.

Footnotes:

*Diversification does not eliminate risk. Investors cannot directly invest in an index.

1IEA, Global Critical Minerals Outlook 2025, as of June 2025

2S&P Global, Battery Storage to Drive Lithium Demand Growth Globally, as of January 8, 2026

3US Department of Energy, Thacker Pass, as of March 2026

4Sprott, Lithium Gains Momentum in 2025, as of December 2, 2025

5EIB, Vulcan Energy Secures €250 million EIB Financing for Landmark Lithium Project, as of December 3, 2025

6Wood Mackenzie, Lithium Demand Could Exceed 13 million tonnes by 2050 as Energy Transition Accelerates, as of March 3, 2026

7Carbon Credits, Lithium Prices Climb Again in 2026, Sending Stocks Upward, as of March 23, 2026

Article by Ayesha Shetty

Author is a contractor of Leverage Shares LLC, a U.S. affiliate of Themes Management Company LLC. Leverage Shares LLC provides certain services to Themes under an intercompany services agreement.