Article by Ayesha Shetty

Why Uranium & Nuclear Energy?

March 9, 2026 | Industry / Commodity Producers

Nuclear energy is moving back into focus as countries seek reliable, low-carbon power to complement renewables. This shift is gaining momentum as electricity demand rises, driven by electrification, AI data centres, and industrial growth, strengthening the case for new nuclear capacity.

The Themes Uranium & Nuclear ETF (URAN) is designed to provide exposure to this evolving segment of the energy landscape.

By attempting to provide diversified exposure to companies engaged in uranium mining and production and nuclear energy, equipment, technology, and infrastructure, URAN may allow investors to participate in the long-term structural trends shaping the uranium and nuclear energy market through a single, liquid investment vehicle.

Key Takeaways

Structural demand tailwinds from electrification, digital infrastructure, and energy-security priorities are reinforcing nuclear power’s role in the global energy mix while uranium supply growth remains gradual after years of underinvestment.

Expanding government support for nuclear capacity and fuel-cycle security, alongside long mine development timelines, is likely to keep policy direction and supply responsiveness central to the uranium market outlook.

#1 Exploding Nuclear Energy Demand

Nuclear power continues to play a central role in the global electricity mix, supported by demand for reliable, low-carbon baseload generation.

Today, nuclear power generates roughly 9% of the world’s electricity from about 440 reactors, underscoring its established position in the global energy system.1

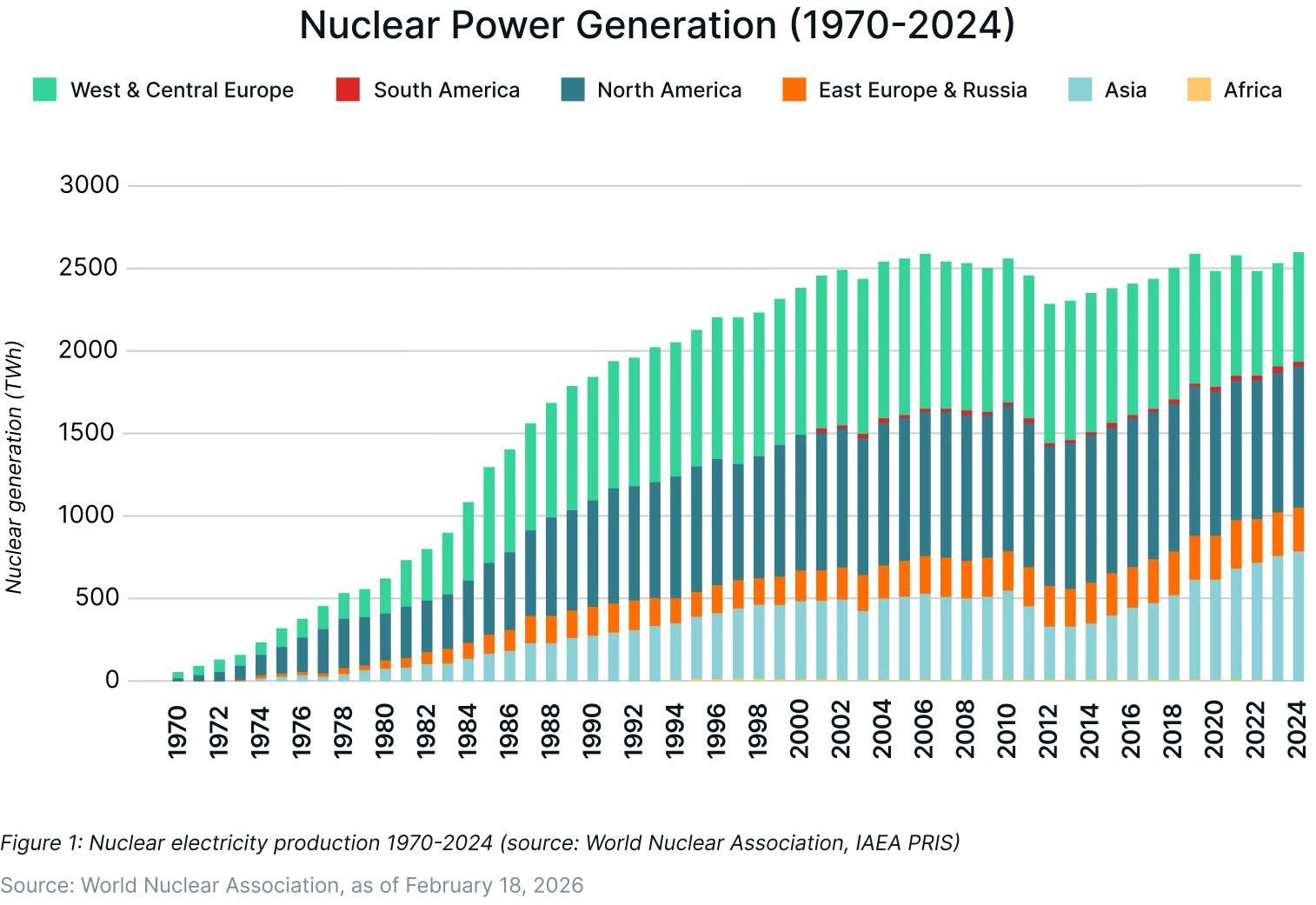

Despite perceptions of slow growth, nuclear output reached a record 2,667 TWh in 2024, reflecting the continued high utilization of the existing fleet.

Nuclear’s importance is particularly visible at the country level. In 2024, fourteen countries generated at least one-quarter of their electricity from nuclear power.

France sources around 70% of its electricity from nuclear energy, while Ukraine, Slovakia, and Hungary obtain roughly half of their power from nuclear generation. Japan, which previously relied on nuclear for more than one-quarter of its electricity, is expected to move back toward that level as reactor restarts progress.1

Looking ahead, electricity demand from emerging digital infrastructure is expected to rise sharply. The IEA projects that global electricity demand will more than double, from 415 TWh in 2024 to 945 TWh in 2030 and 1,300 TWh in 2035, according to its base-case scenario. Of this, around 220 TWh is projected to be supplied by nuclear power.2

A number of technology companies have already moved to secure nuclear generation to support future energy needs. While the IEA expects most new nuclear capacity additions to contribute after 2030, some companies are pursuing agreements tied to existing, restarting, or advanced nuclear capacity:

Microsoft: 20-year PPA to restart the 880 MWe Three Mile Island Unit 1.

AWS: Long-term nuclear PPA with Talen Energy (~960 MW initial).

Amazon: Investment and offtake rights in X-Energy’s Xe-100 SMR project.

Amazon: MOU with Dominion Energy to explore SMRs at North Anna.

Meta: 20-year PPA for 1,121 MW of nuclear power in Illinois.

Google: Agreement with Kairos Power supporting SMR deployment (~500 MWe by 2035).

Against this backdrop, nuclear capacity is projected to expand. If existing, under-construction, planned, and policy-driven projects are realized, global nuclear capacity could reach approximately 1,446 GWe by 2050.2

#2 Supportive Government Policies

Policy support for nuclear energy has strengthened at both the multilateral and national levels, reinforcing the demand outlook for nuclear power and the uranium fuel cycle.

At the United Nations COP28 climate conference in December 2023, 25 governments signed the Declaration to Triple Nuclear Energy, committing to support a global goal of tripling nuclear capacity by 2050. The declaration recognized nuclear power’s role in achieving net-zero emissions and maintaining the 1.5°C climate objective, while also highlighting its importance as clean, dispatchable baseload power.2

The declaration uses 2020 as its baseline year, when operable global nuclear capacity stood at 393 GWe; tripling that level would imply capacity of nearly 1,200 GWe by 2050. Industry alignment has followed, with 130 nuclear companies also pledging support for the tripling target.2

National policy is reinforcing this momentum. In May 2025, the United States issued executive orders aimed at quadrupling domestic nuclear capacity to 400 gigawatts by 2050, from roughly 100 gigawatts today.3

The policy push extends to the fuel cycle as well. In January 2026, the U.S. Department of Energy announced US$ 2.7 billion in funding to restore domestic uranium enrichment capacity and support uranium supply chains.4

Private capital is also aligning with policy priorities. In 2024, Cameco and Brookfield established a strategic partnership with the United States focused on strengthening the nuclear fuel supply chain.5

Other countries, including China, India, Russia, Turkey, and South Africa, have similarly outlined nuclear expansion plans as part of efforts to reduce fossil fuel dependence and secure stable baseload generation.2

#3 Short-term Supply Deficit

Despite improving demand visibility, the uranium market is widely viewed as structurally tight after years of underinvestment following the Fukushima period. As reactor demand stabilizes and begins to grow, supply has struggled to keep pace.

Industry analysis indicates global uranium requirements could rise to 86,000 tonnes by 2030 and 150,000 tonnes by 2040, while output from existing mines could fall by roughly 50% over that period without significant new investment.⁶ The long lead times required to permit and develop new uranium mines, often stretching a decade or more, further constrain the speed of supply response.

Near-term market dynamics also reflect tightening conditions. U.S. uranium production remains modest at roughly 1 million pounds annually compared with consumption exceeding 50 million pounds, underscoring continued reliance on imports.⁸

Producer discipline has reinforced the tightness. Kazakhstan’s Kazatomprom, the world’s largest uranium producer, announced plans to cut 2026 output by roughly 10%, equivalent to about 5% of global primary supply, citing its market-centric production strategy.⁷ The move highlights the limited elasticity of primary supply even as demand expectations improve.

Analysts have also warned that these dynamics could contribute to a 20-million-pound market deficit in the near term if new supply does not emerge.⁹

Longer term, the market is expected to require a broader mining expansion, though project timelines and capital intensity suggest supply additions are likely to be staged.¹⁰

For investors, these supply dynamics are likely to remain an important variable to monitor as reactor demand evolves and new mine capacity progresses through the development pipeline.

#4 Strategic Critical Mineral Status

Uranium’s designation as a critical mineral by the U.S., EU, and their allies highlights its growing importance to national security and defence applications, from naval propulsion to power grids.

In response, governments are building strategic reserves and funding exploration to reduce dependence on foreign suppliers, particularly after the supply chain disruptions seen post-2022.

This classification is unlocking billions of dollars in public funding, tax incentives, and streamlined permitting for new mines, echoing the policy support extended to rare earths. It also positions uranium as a geopolitical hedge comparable in some respects to oil.

With President Trump’s 2025 executive orders prioritising domestic critical minerals, U.S. producers could see near-term benefits in a market where roughly 95% of supply is imported.

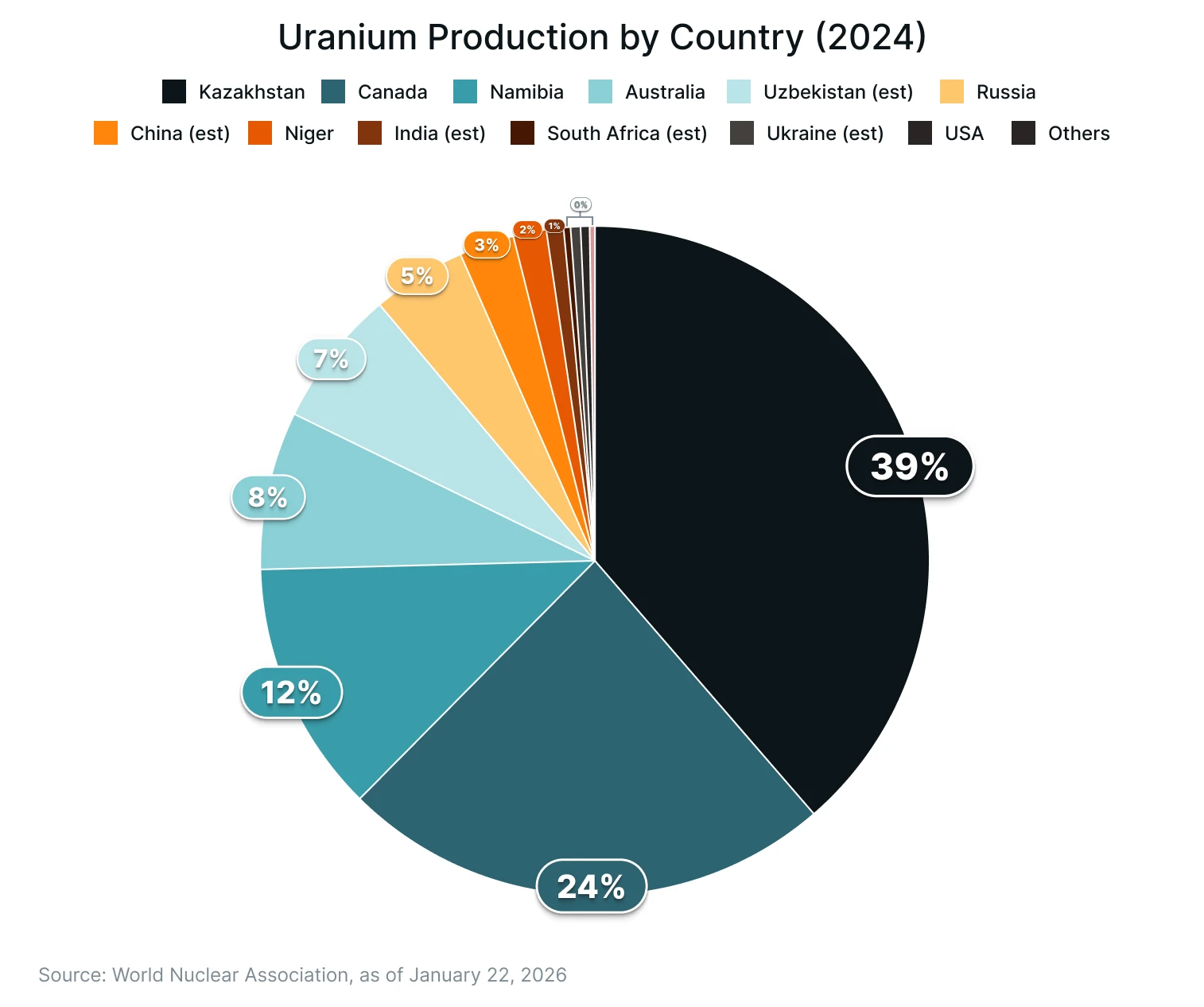

On the supply side, Kazakhstan remains the dominant producer, accounting for about 40% of global uranium mine output, while Canada and Namibia together contribute a significant additional share.¹¹

The relatively limited number of major producing jurisdictions reinforces the importance of supply diversification for utilities and governments reliant on nuclear fuel.

Resource availability adds another dimension to the outlook. Identified global uranium resources are generally considered sufficient to meet long-term demand under most scenarios, but bringing new supply online typically involves lengthy permitting timelines, sustained capital investment, and supportive price signals.¹²

This combination of adequate geological resources but slow project development continues to keep fuel security in focus for policymakers.

In the United States, nuclear power still accounts for a meaningful share of electricity generation, yet domestic uranium resources represent only a small portion of global reserves.⁴ This import dependence has sharpened policy attention on strengthening the domestic fuel cycle.

As part of this effort, the Department of Energy’s HALEU Availability Program is intended to build domestic capacity for high-assay low-enriched uranium used in advanced reactors and to reduce reliance on foreign enrichment services.¹³

For investors, uranium’s strategic classification suggests that policy direction, fuel-cycle investment, enrichment capacity expansion, and supply diversification will remain key factors to monitor in the market.

#5 Expanding Investor Access

Against this tightening policy and supply backdrop, investor access to the uranium theme has also broadened meaningfully.

Historically, exposure was largely limited to mining equities or opaque physical markets. Today, exchange-listed vehicles and physical uranium funds have made the theme more accessible to a broader range of investors.

Market pricing already reflects renewed interest. Uranium spot prices briefly rose above US$100 per pound in early 2026 before moderating, with recent trading around the mid-$80s per pound range.14 This represents a sharp recovery from the prolonged lows of the previous decade.

Historically, uranium prices have tended to reprice during periods when utilities return to long-term contracting following phases of under-procurement.5

Equities provide additional leverage. Uranium miners typically exhibit high operational sensitivity to price movements, meaning earnings and valuations can expand quickly in rising price environments, albeit with higher risk.

How to Play It

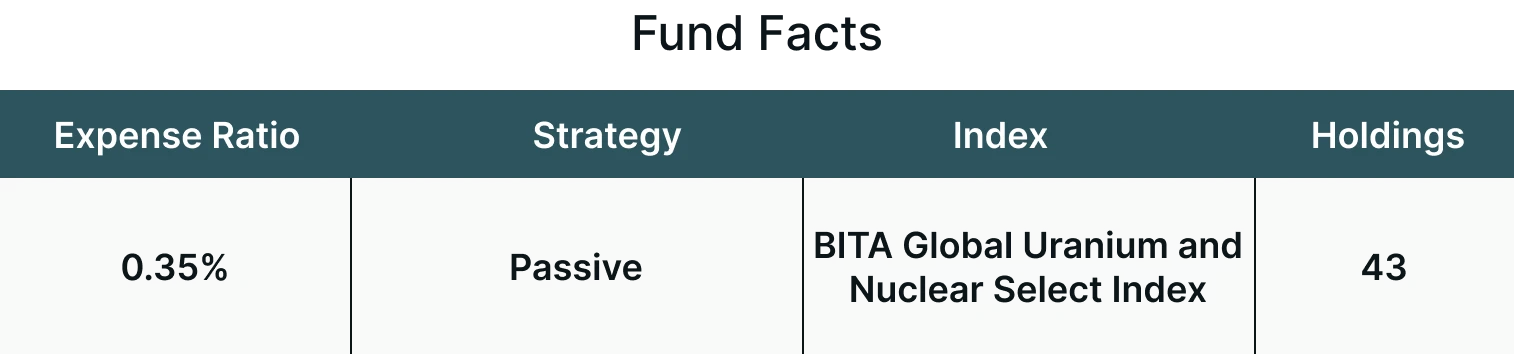

The Themes Uranium & Nuclear ETF (URAN) seeks to track the BITA Global Uranium and Nuclear Select Index (BGUNSI), which identifies companies that derive their revenues from uranium mining, explorations, refining, processing, and royalties, as well as nuclear energy, equipment, technology, and infrastructure.

URAN seeks to provide investment results that correspond generally to the price and yield performance, before fees and expenses, of the BGUNSI Index.

Conclusion

As electricity demand rises, driven by electrification, digital infrastructure, and energy-security priorities, nuclear energy is increasingly being reconsidered as part of the long-term generation mix.

Yet the supply side has changed far more slowly. New uranium production remains difficult and time-intensive to bring online, and output is concentrated in a relatively small number of jurisdictions. This combination has left the market more sensitive to shifts in reactor demand and utility procurement than in past periods.

In a portfolio context, exposure to uranium and nuclear energy provides sensitivity to these structural power-demand trends rather than relying solely on traditional commodity cycles.

However, the sector remains closely tied to utility contracting activity, reactor build progress, enrichment capacity, and government policy.

Tracking how demand growth interacts with the pace of new supply and fuel-cycle investment will remain central to assessing the uranium market’s trajectory.

For more information about the fund, including fees/expenses, holdings, standardized performance, risks and more, please visit https://themesetfs.com/etfs/uran.

Footnotes:

*Diversification does not eliminate risk. Investors cannot directly invest in an index.

1World Nuclear Association, Nuclear Power in the World Today, as of February 18, 2026

2World Nuclear Association, World Nuclear Outlook Report, as of January 22, 2026

3World Nuclear News, Trump sets out aim to quadruple US nuclear capacity, as of May 24, 2025

4US Department of Energy, U.S. Department of Energy Awards $2.7 Billion to Restore American Uranium Enrichment, as of January 5, 2026

5Cameco, Cameco and Brook-eld establish transformational partnership with United States Government, as of October 28, 2025

6Financial Times, Uranium Shortfall Threatens Nuclear Energy Renaissance, as of September 5, 2025

7World Nuclear News, Kazatomprom to lower uranium production in 2026, as of August 22, 2025

8Reuters, Is the US uranium market about to go nuclear in 2026?, as of January 14, 2026

9MarketWatch, This Perfect Storm Could See Uranium Prices Bounce Back to The Year’s Highs Above $100 A Pound, as of August 28, 2024

10S&P Global, Uranium’s next decade: from tight supply to a broader mining boom, as of February 18, 2026

11World Nuclear Association, Uranium Production by Country, as of January 20, 2026

12World Nuclear Association, Supply of Uranium, as of December 9, 2025

13U.S. Department of Energy, HALEU Availability Program

14TradingEconomics, Uranium Price Data, as of 2026

Article by Ayesha Shetty

Author is a contractor of Leverage Shares LLC, a U.S. affiliate of Themes Management Company LLC. Leverage Shares LLC provides certain services to Themes under an intercompany services agreement.