Article by Edward Sheldon

Defense Stocks: Is the April Selloff Justified?

April 28, 2026 | Research Insights

Defense stocks have taken a hit in recent weeks. Amid an easing of geopolitical tensions, names such as RTX Corp, Lockheed Martin, and Northrop Grumman have fallen double-digit percentages1 from their 52-week highs. Is this selloff across the sector justified? Let's take a look at recent Q1 earnings for clues.

RTX Corp: Full-Year Guidance Raised

RTX Corp’s Q1 earnings showed that the aerospace and defense company has been performing well recently. For the quarter2, sales amounted to $22.1 billion, up 9% year-over-year (+10% organic growth) while adjusted earnings per share (EPS) came in at $1.78, up 21% year-over-year. Zooming in on its defense segment, Raytheon, year-over-year sales growth here was a robust 10%. Driving the strong performance in this segment was demand for the company’s land and air defense systems, including Patriot and GEM-T, as well as higher volume on naval munitions programs.

Looking ahead, RTX increased its guidance for the full year. It now expects adjusted sales of $92.5 to $93.5 billion, up from previous guidance of $92.0 to $93.0 billion, along with adjusted EPS of $6.70 to $6.90 (versus $6.29 for 2025), up from $6.60 to $6.80. Note that at the end of the first quarter, the company had a backlog of $271 billion (of which $109 billion was defense related). So, while there is some uncertainty in relation to the near-term prospects for the group’s civil aviation business Pratt & Whitney due to the conflict in the Middle East, management clearly expects the company to continue performing well in 2026.

Northrop Grumman: Full-Year Guidance Reaffirmed

Northrop Grumman’s Q13 sales came in at $9.9 billion, up 4% year-over-year (+5% organic growth). Breaking its sales down by segment, the company’s aeronautics division – which produces advanced military aircraft – had the strongest growth at 17% year-over-year, while defense systems and mission systems reported 5% and 2% growth respectively. In terms of profitability, net earnings for the period amounted to $875 million versus $481 million a year earlier. Net awards for the quarter were $9.8 billion.

Looking ahead, the defense company reaffirmed its 2026 financial guidance for sales, segment operating income, MTM-adjusted EPS, and free cash flow. Note that in January, the company projected mid-single-digit sales growth and continued strong performance and free cash flow for 2026. At the end of the quarter, its backlog was $96 billion. That is equivalent to over two times 2025 sales.

GE Aerospace: Low Double-Digit Growth Expected in 2026

GE Aerospace’s Q14 defense earnings were strong, as were its overall group earnings. For the quarter, group adjusted revenue was $11.6 billion, up 29% year-over-year. Meanwhile, operating profit was $2.5 billion, up 18%, and free cash flow was $1.7 billion, up 14%. In the company’s Defense & Propulsion Technologies (DPT) segment, revenue was $3.2 billion, up 19% year-over-year with Defense & Systems revenue up 14%.

Looking ahead, the company expects low double-digit top-line growth from last year’s figure of $42.3 billion. Operating profit is expected to amount to $9.85 billion to $10.25 billion for 2026 versus $9.1 billion in 2025, despite high oil prices and an expected reduction in global flight activity. Free cash flow is forecast to come in between $8.0 billion and $8.4 billion compared to $7.7 billion in 2025. Within its DPT segment, it is anticipating revenue growth in the mid-to-high single digits for 2026.

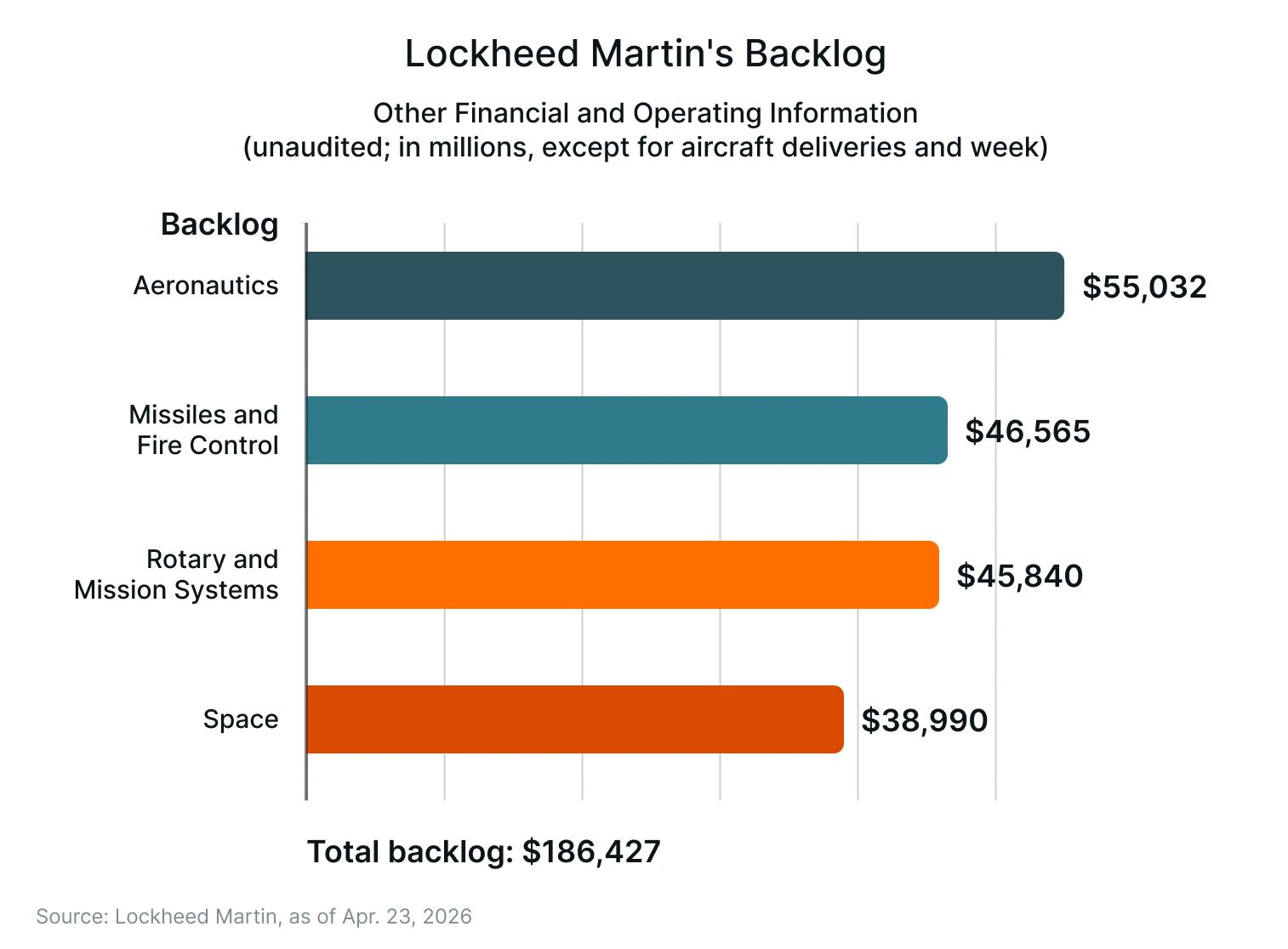

Lockheed Martin: Weak Earnings but a Strong Backlog

Lockheed Martin’s Q1 earnings5 numbers were a little underwhelming relative to those of other US defense stocks. For the quarter, sales were $18.0 billion compared to $18.0 billion in Q1 2025 while net earnings were $1.5 billion compared to $1.7 billion a year earlier. Cash from operations amounted to $220 million, down from $1.4 billion in Q1 2025. Meanwhile, free cash flow was negative $291 million, compared to $955 million in Q1 2025.

However, the company did reaffirm its 2026 full-year guidance. Given the robust defense spending backdrop, it continues to anticipate sales and operating profit growth of approximately 5% and 25% year-over-year with expected free cash flow of between $6.5 and $6.8 billion. At the end of the quarter, the company’s backlog stood at $186 billion. That figure represents roughly 2.5 times 2025 revenue.

An Opportunity in Defense?

Looking at these numbers, the recent share price weakness across the defense sector does not look to be fully justified. While there are some operational risks on the horizon, especially for companies that are more focused on civil aviation such as RTX Corp and GE Aerospace, backlogs and guidance remain healthy. Given the recent pullback, now could potentially be a good time to take a closer look at the sector. With sector hype cooling and valuations compressing, there could be a compelling opportunity for long-term investors seeking to capitalize on the sustained secular tailwinds of global defense spending.

Footnotes:

1Google Finance, as of April 28, 2026

2RTX Reports Q1 2026 Results, as of April 21, 2026

3Norhtrop Grumman Reports First Quarter 2026 Financial Results, as of April 21, 2026

4GE Aerospace Announces First Quarter 2026 Results, as of April 21, 2026

5Lockheed Martin Reports First Quarter 2026 Financial Results, as of April 23, 2026

Author is a contractor of Leverage Shares LLC, a U.S. affiliate of Themes Management Company LLC. Leverage Shares LLC provides certain services to Themes under an intercompany services agreement.