April 26, 2025

Defense Stocks Rise Over Tariff Uncertainty and Europe’s Military Plans

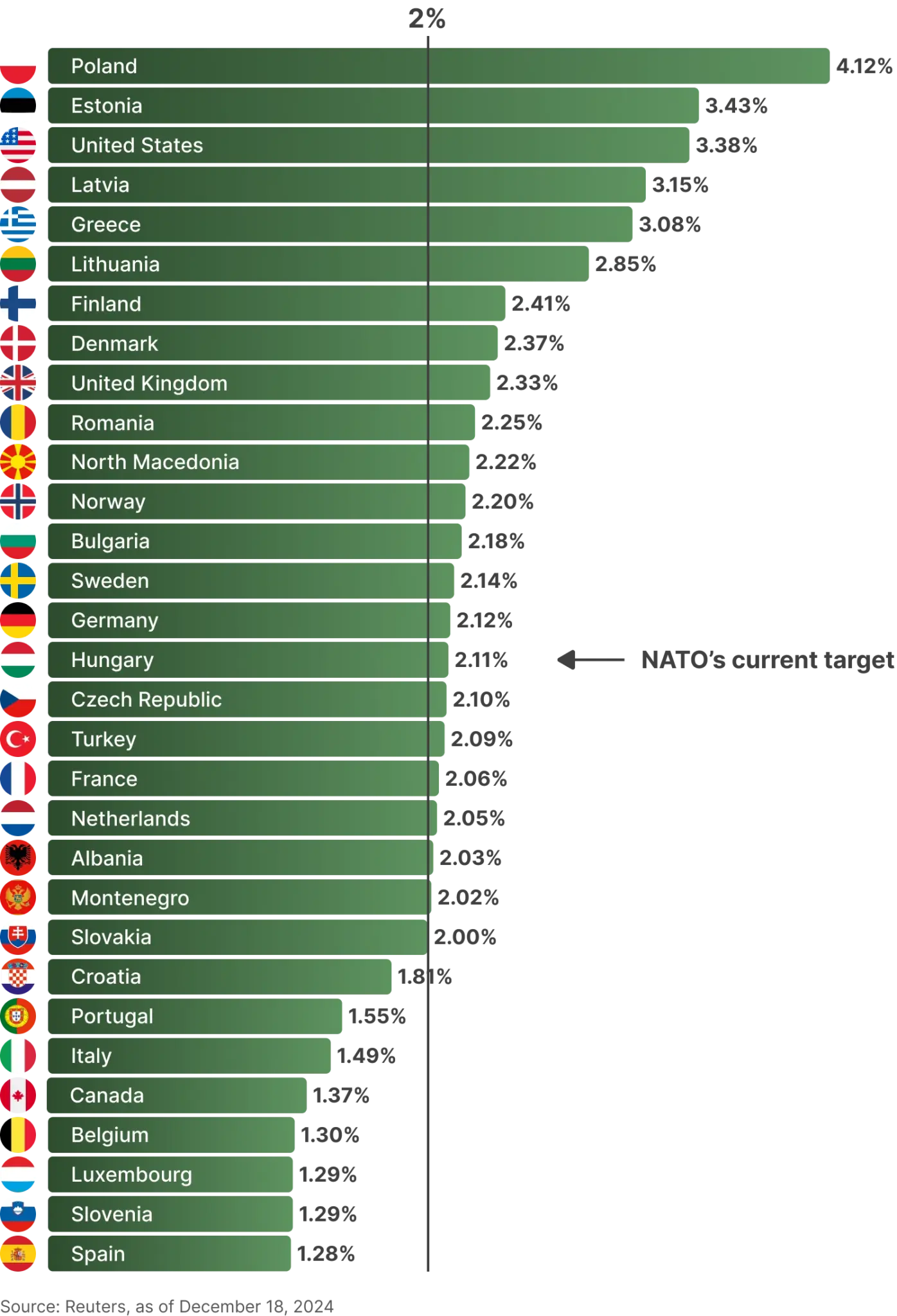

As President Donald J. Trump emerged victorious in the 2024 election and prepared to begin his second term, his team informed European officials that he expects their respective countries to spend at least 5% of their Gross Domestic Product (GDP) on building military capabilities. As of 2024, it was estimated1 that virtually every country – even the U.S. – fell short of this target.

However, it bears noting that the U.S.’ spending is significantly higher than that of almost every one of its European allies combined. Additionally, given the significant deployment of U.S. military assets over in Europe to buttress its defense from threats, it is intuitively logical that Europe could ideally stand to be more invested in its own defense (and an idea supported2 by many a U.S. think tank as well).

In the wake of President Trump’s re-election, plans were underway within the European Union (E.U.) to increase spending by €500 billion per year, which the European Commissioner for Defense Industry and Space Andrius Kubilius argued was only enough to cover3 an air defence programme. Also, many of the bloc’s nations balked at the prospect of raising the annual target from 2024’s 2% to a mere 3% (which would cost the E.U. around €200 billion), due to economic difficulties and already-stretched balance sheets. Poland, an already-aggressive spender owing to its proximity to the ongoing Russo-Ukrainian conflict, suggested one of two methods4 to raise the required capital: the E.U. could sell more joint bonds backed by its own long-term budget or create a new special purpose vehicle modelled on the euro zone bailout fund, the European Stability Mechanism, to provide loans by selling bonds backed by paid-in and callable capital from participating countries.

The first option found few takers but the potential for non-E.U. countries such as the United Kingdom and Norway to participate in the second option created some buzz; however, markets expect that this “new borrower” would have pay a premium over the interest the E.U. pays for its bonds – thus adding to the cost burden.

In light of these difficulties, President Trump’s demand for spending to go up by an ever larger margin had found few enthusiastic takers. On the 6th of March this year, the European Commission proposed the “ReArm Europe” plan5, which aimed to raise €650 billion over four years (i.e. an average of €175 billion each year) by allowing member nations to increase their military budgets to up to 1.5% of GDP without being counted in their national deficits and raising €150 billion through EU-issued bonds, which would then be lent to member states at low-interest rates and long repayment terms.

The plan almost instantly ran into trouble6, with Italy and Spain demanding broader definition of the plan to include anti-terrorism, satellite communication, artificial intelligence and quantum computing capabilities. Both nations also expressed discomfort with the name, with Spain stating outright that southern Europe faces threats that are altogether different from those faced by Eastern Europe. The plan’s name was amended to “Readiness 2030”.

Steering Away from U.S. Dependence?

E.U. officials proposed7 that European countries can partake in the €150 billion loan program – titled “SAFE” (Security Action for Europe) – if the products being procured have a definitive Europe connection. For ammunition, missiles and small drones, 65% of the costs must originate inside the E.U., European Economic Area (EEA), European Free Trade Association (EFTA) countries or Ukraine, with the manufacturer being located within these blocs and not controlled by another country. For more complex systems such as air and missile defense systems and larger drones, it must be possible to substitute components that could be subject to restrictions imposed by other countries.

While it is possible for an E.U.-based subsidiary of a British or U.S. company, the cost origination aspect implies that weapons manufactured in a British or American plant might not be eligible – a move that rankled U.S. officials, with Secretary of State Marco Rubio reportedly warning8 Europe that any exclusion of U.S. companies would be seen negatively by Washington.

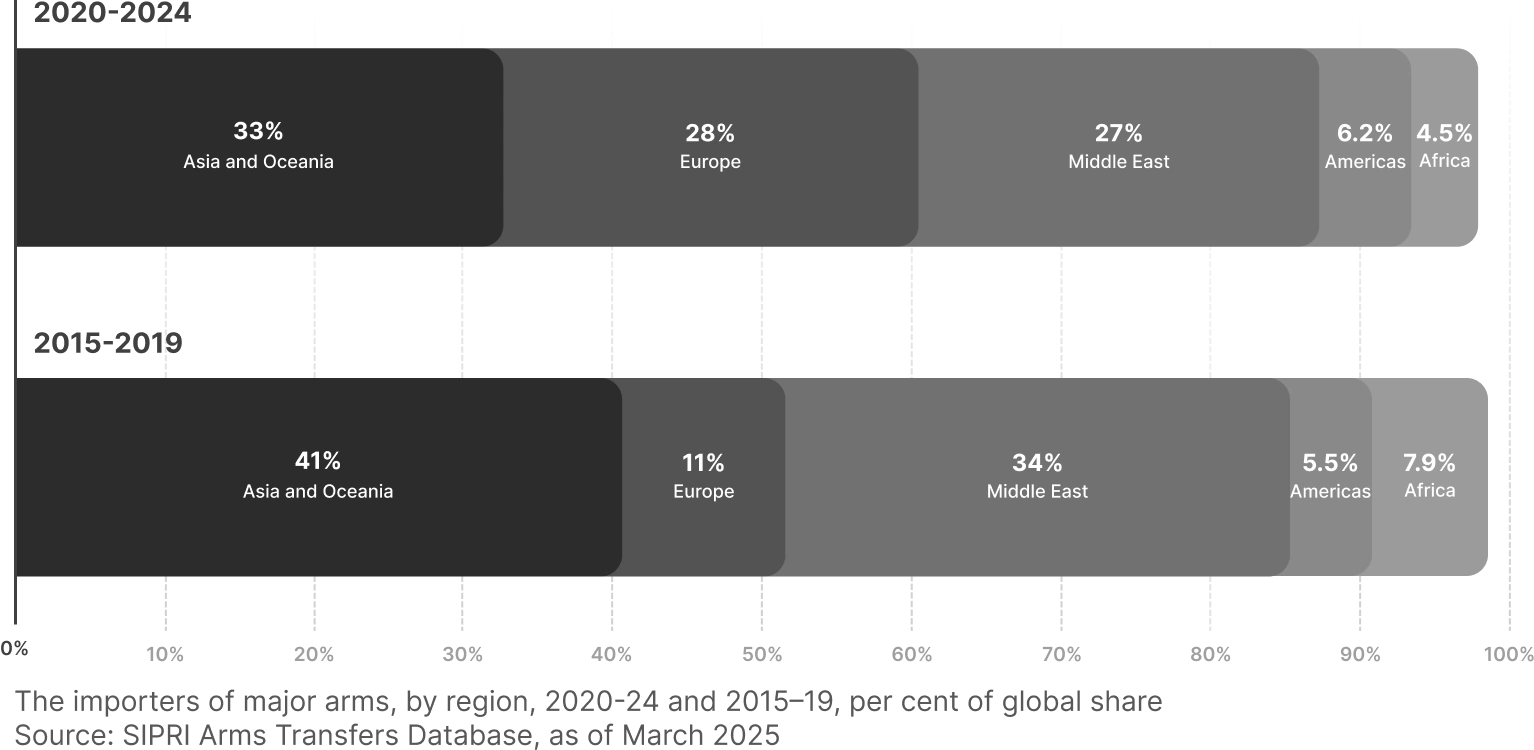

This warning has a certain logic: outside of Ukraine (which became the world’s largest importer of major arms in the 2020–24 period), arms imports by the E.U. more than doubled9 between 2015–19 and 2020–24, with the U.S. supplying 64% of these arms.

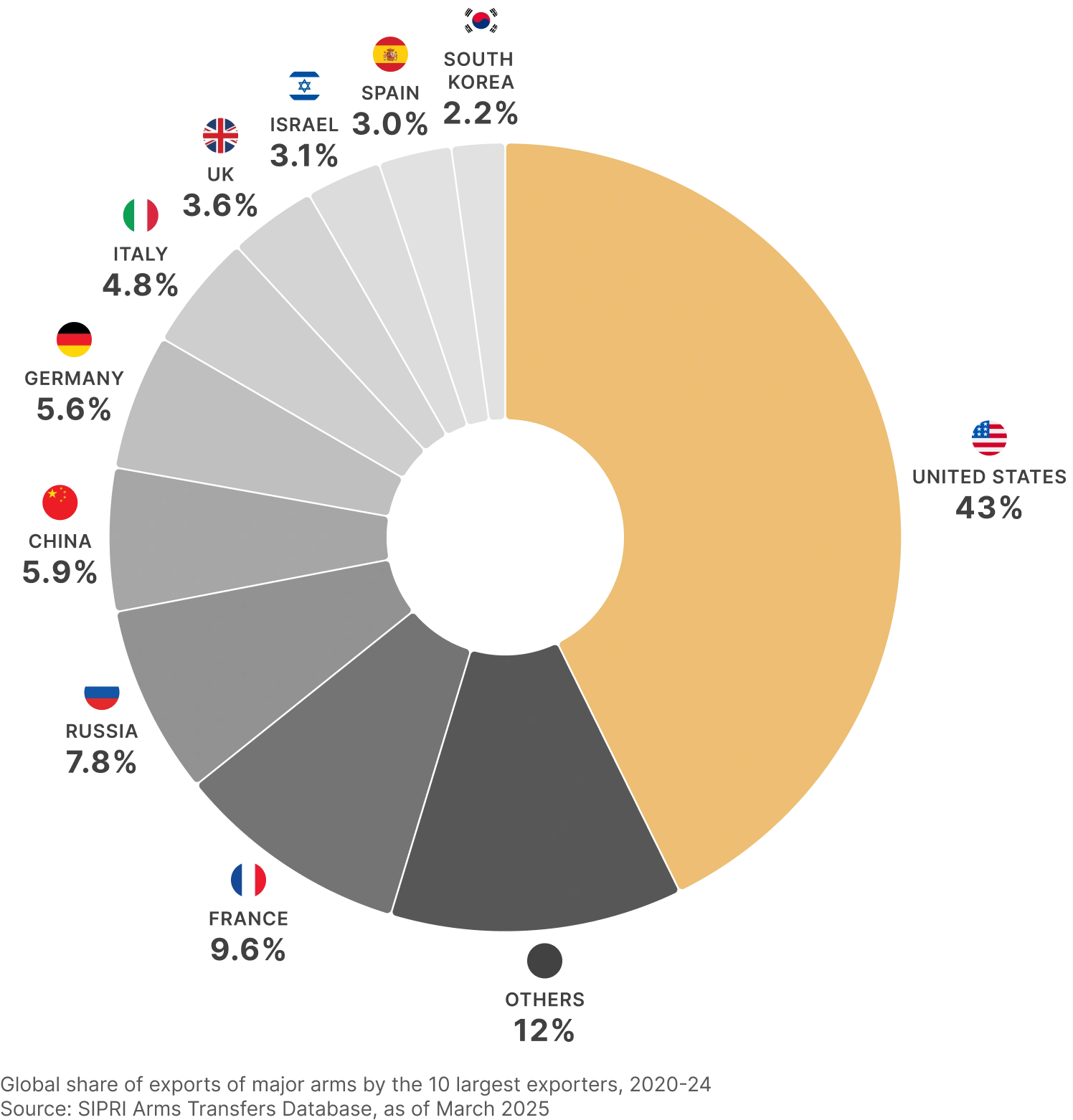

With arms supplied to 107 countries in 2020-24, U.S. arms exports increased by 21% between 2015–19 and 2020–24, with its share of global arms exports growing from 35% to 43%. In effect, the U.S. is resolutely the world’s largest arms exporter – with France a very distant second.

For the first time in two decades, the largest share of U.S. arms exports in 2020–24 went to Europe (35%) rather than the Middle East (33%), thus possibly underlining Secretary Rubio’s concerns.

Despite calls from within Europe to limit dependence on U.S. imports, European NATO members have over 500 combat aircraft and many other complex weapons systems still on order from U.S. suppliers10. However, with “smaller” weapons and systems, it is likely that European manufacturers might be net beneficiaries.

Market Impact and Possible Factors

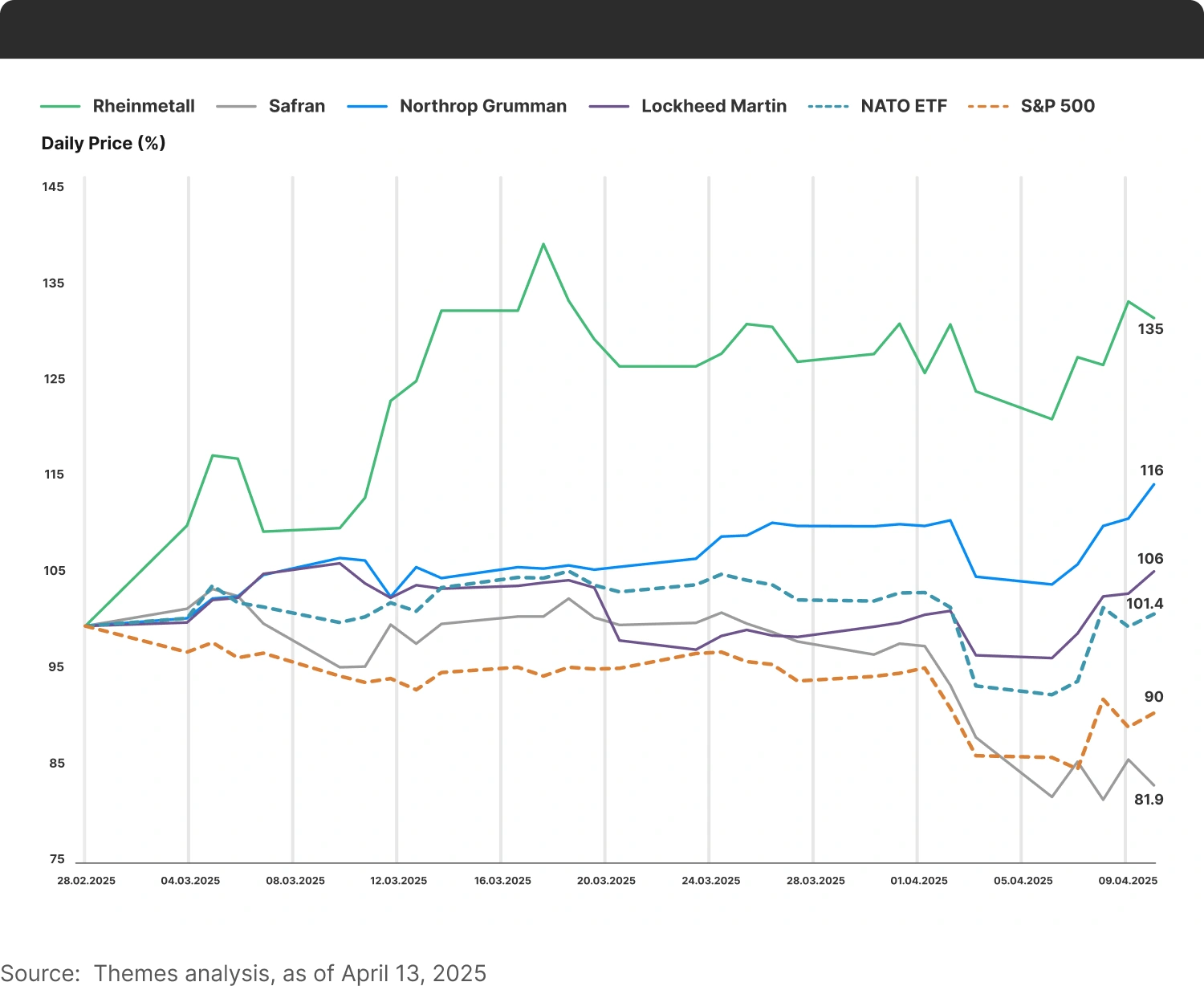

While it is by now common knowledge that the broad market S&P 500 (SPX) has been under significant pressure and volatility in the lead-up to President Trump’s “Liberation Day” tariff announcement, defense stocks have shown a widely varying trajectory as driven by investor convictions:

Despite both being European companies that are potentially beneficiaries of the E.U.’s largesse for arms buying, German arms manufacturer Rheinmetall substantially outperforms relative to France’s engine manufacturer Safran. Despite being in the same industry as Safran (i.e. aviation systems) while potentially impacted by E.U. limitations, U.S. aviation technology majors Northrop Grumman and Lockheed Martin have been somewhat resurgent.

A growing spearhead of NATO’s air forces has been Lockheed Martin’s F-35, a fifth-generation combat jet whose center fuselage and various electronics suites are produced by Northrop Grumman. The F-35 has a decidedly checkered history: as per the nonpartisan nonprofit government watchdog group Project on Government Oversight (POGO)11, which analyzed the reports made available by the U.S. military and manufacturers on the U.S.-based fleet, the F-35 has a fleet-wide Full Mission Capable (FMC) Rate – which measures what proportion of jets are capable of executing all assigned missions – of only 30%. The average fleet-wide monthly availability rate – defined as the percentage of time individual aircraft are “available” to perform at least one designated mission – was calculated at 51%, with an average repair time of 141 days to return an aircraft to duty. Despite this, the broad spectrum of missions it is designed to complete has resulted in up to 615 orders either completed or planned across the European Union, the United Kingdom and Switzerland alone12. Alenia Aermacchi’s Cameri facility in Italy (jointly operated with Lockheed Martin) is one of three global F-35 assembly lines13 and serves as Europe’s hub for F-35 production and maintenance. Northrop Grumman is also partnered with Rheinmetall to establish a second production line for the center fuselages in Weeze, Germany14.

Perhaps the strongest factor for its continuing service in Europe is that there is no fifth-generation equivalent currently among European manufacturers. The nearest possible competitor is the Future Combat Air System (FCAS) under development by Dassault Aviation, Airbus and Spain’s Indra Sistemas – with a first test flight expected around 2027 and entry into service around 204015. Switching out of American aviation will be a very expensive proposition for European militaries; therefore, they’re likely to continue to hold on and run out the sunk cost over the decades-long shelf life of the systems. This is one likely factor buoying Rheinmetall, Northrop Grumman and Lockheed Martin together, who also outperform the broad market by a comfortable margin.

On the other hand, the acquisition of the likes of “smaller-ticket” items – drones, munitions, artillery, armoured vehicles, etc. – will potentially have little room to spare for U.S. manufacturers, who might instead be involved with the inevitable European-origin awardees of these contracts by way of technical consulting, guidance on manufacturing, etc. (as they have been for decades now). Rheinmetall is expected to be a wide-ranging beneficiary from increases in E.U.’s expenditure on projectile weapon systems and munitions while historical “big-ticket” buy-ins of aviation systems such as the F-35 are unlikely to be substituted out before said systems’ end of life. Also, given the performance characteristics of these systems, it’s unlikely that European militaries would be willing to settle for less or not be receptive to next-generation products by geographically-diversified/connected U.S. manufacturers such as Lockheed Martin and Northrop Grumman. This creates some bottlenecks for the likes of Safran as they’re found predominantly in French/European-produced aircraft.

Thus, while “Readiness 2030” might vigorously moot a “European” character to military spending, U.S. manufacturing expertise can be expected to be well-represented, regardless.

A "Balanced" Investing Style?

The Themes Transatlantic Defense ETF (U.S. ticker: NATO) – which includes Rheinmetall, Lockheed Martin, Northrop Grumman and Safran along many other manufacturers – pulls at nearly 10% outperformance** on a net basis relative to the S&P 500 as measured from the end of February till the 11th of April. After a period of decline, the “NATO” ETF is now drawing flat relative to the end of February and has a slight bullish momentum being imputed.

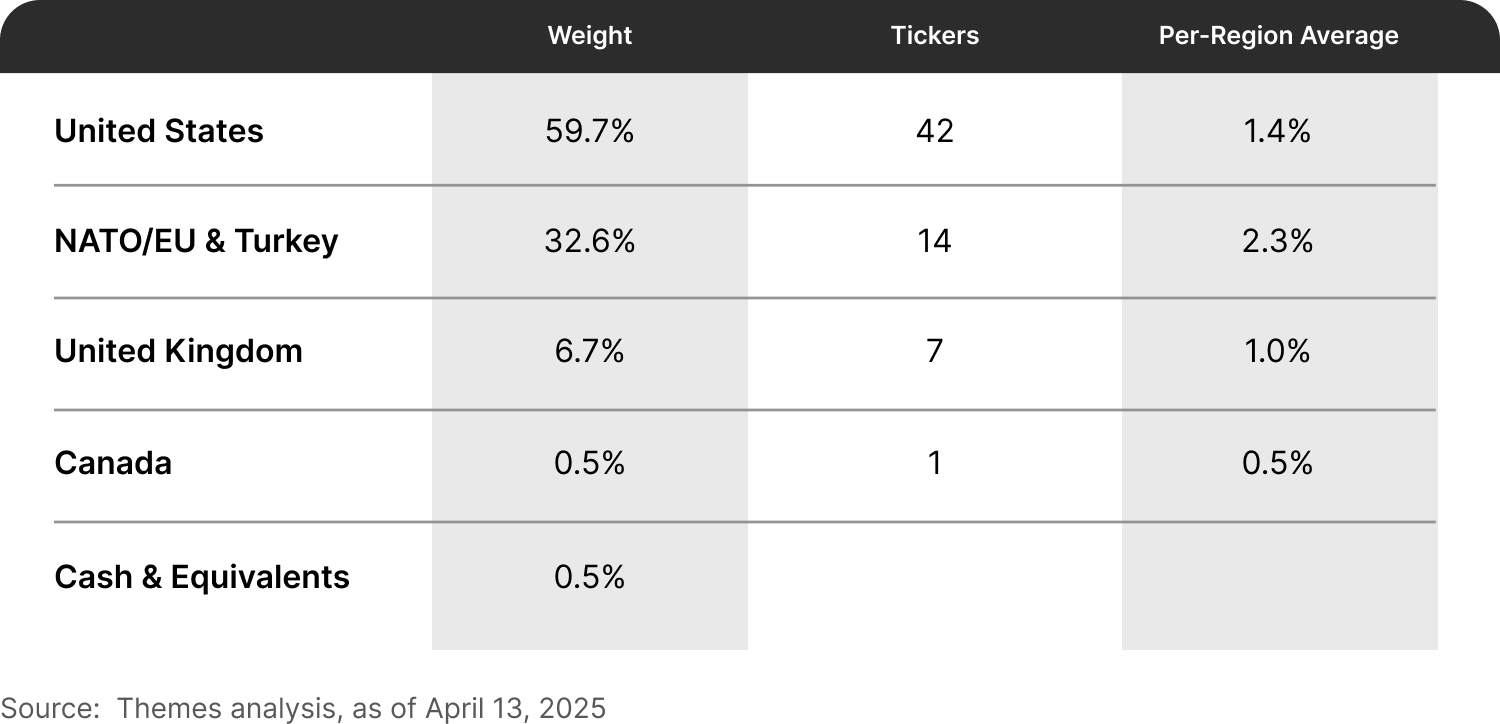

In terms of holdings, the “NATO” ETF is both balanced and “international”:

While the Top 10 holdings by weight have a near-even balance between U.S. and E.U. tickers, U.S. tickers do make up almost 60% of the “NATO” ETF by total weight. But with the remainder being driven by tickers mostly from the Continent, it has quite a distinctive profile.

An interesting feature is that the ETF assigns a slightly higher average constituent weight to European (i.e. EU, EEA and EFTA) tickers than it does to tickers from other regions, including the U.S.

In Conclusion

The favourable representation of European tickers in the “NATO” ETF might prove to be an interesting feature that might enable investors to capture the uptrend in European military spending. At the same time, it is possible that European countries would not commit vast sums of capital to develop alternative “high-ticket” weapon systems that are entirely distinct or free from U.S. suppliers.

Overall, regardless of economic conditions, it is increasingly likely that nations in the Western Hemisphere remain locked into sustained and increased military spending, potentially creating ample opportunities for outperformance versus the market. The “NATO” ETF’s distribution of weights across regions adds an interesting layer of consideration for investors looking to capitalize on spending patterns being implied by Western governments. Investors might recognize the possible benefits of the balancing act built into the “NATO” ETF and consider diversifying their portfolio with this relatively recent instrument.

Footnotes:

*Investors might recognize the possible benefits of the balancing act built into the "NATO" ETF and consider diversifying their portfolio with this relatively recent instrument.

**Past performance does not guarantee future returns.

1"Europe's conundrum: how to fund defence spending", Reuters, 18 December 2024

2"Trump's Five Percent Doctrine and NATO Defense Spending", Peterson Institute for Internation Economics, 5 February 2025

3"Hearing of Andrius Kubilius", Confirmation hearings for the European Commission, 6 November 2024

4"Joint EU defence funding mulled in era of Ukraine war, Trump return", Reuters, 11 December 2024

5"The ReArm Europe Plan: Squaring the Circle Between Integration and National Sovereignty", IRIS France, 12 March 2025

6"Brussels rebrands 'Rearm Europe' plan after backlash from leaders of Italy and Spain", Euro News, 21 March 2025

7"Explainer: Can non-EU companies be part of EU's big defence fund?", Reuters, 21 March 2025

8"US officials object to European push to buy weapons locally", Reuters, 2 April 2025

9"Ukraine the world’s biggest arms importer; United States’ dominance of global arms exports grows as Russian exports continue to fall", Stockholm International Peace Research Institute, 10 March 2025

10"US dominates European weapons purchases: report", Politico, 10 March 2025

11“F-35: The Part-Time Fighter Jet”, Project On Government Oversight, 26 February 2024

12“Lockheed Martin F-35 Lightning II operators”, Wikipedia, accessed on April 15, 2025

13“The first Italian F-35 rolls out of the hangar”, Leonardo Company Newsroom, 16 March 2015

14“Advancing Aeronautics Through F-35 Manufacturing Excellence”, Northrop Grumman Newsroom, 15 April 2025

15“New trinational deal paves way for FCAS demonstrator program”, Defense News, 17 May 2021

Тhis is not an offer, or recommendation or professional advice.