April 23, 2025

The Impact of Rising Gold Prices on Miners’ Profitability

The price of gold – which is often considered to be a “safe-haven asset” – has moved higher recently. Boosted by the elevated level of geopolitical and economic uncertainty globally, it has climbed from around $2,300 per ounce to nearly $3,500 per ounce over the last year.

For gold mining companies that are already producing the commodity, this price rise is leading to higher cash flows and earnings in many cases. Here’s a look at some gold miners that have benefited from higher gold prices.

Alamos Gold

When gold prices are rising, gold producers’ earnings often rise too. In this scenario, producers’ revenues tend to increase at a faster pace than their costs, resulting in an element of operating leverage.

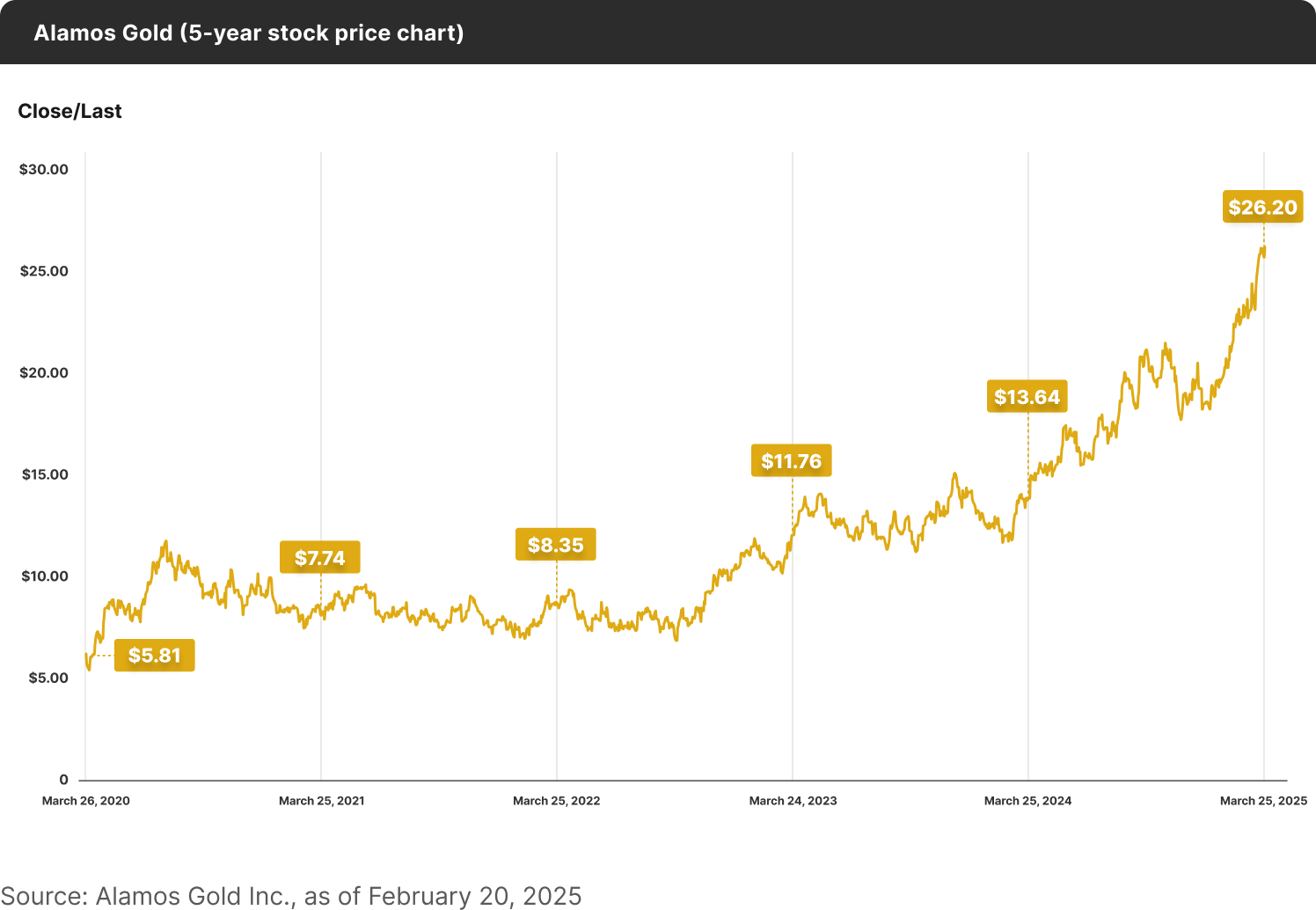

Alamos Gold (4.96%) is a good example here. It’s a Canadian gold producer that has operations in Canada and Mexico and is listed on both the Toronto Stock Exchange (TSX) and the New York Stock Exchange (NYSE).

For the fourth quarter of Q41, the gold producer achieved a realized gold price of $2,632 per ounce versus $1,974 per ounce in Q4 2023. As a result, the company generated Q4 operating revenues of $376 million, an increase of 47% year on year. Adjusted net earnings, however, were up 110% year on year to $103 million while cash flow from operations (before working capital) was up 73% to $208 million.

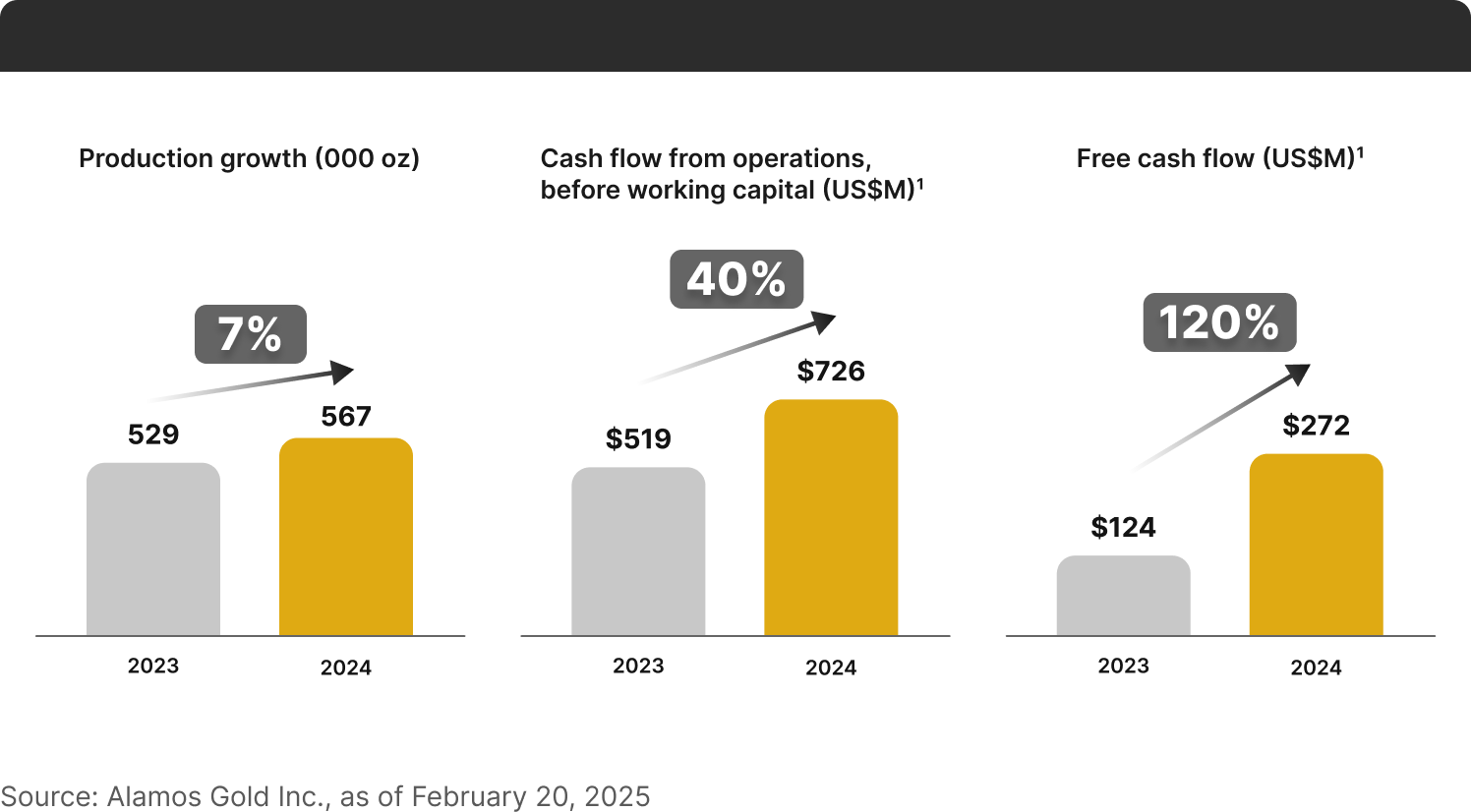

For the full year, Alamos generated revenue of $1,347 million, up 32% year on year. This was despite the fact that production only rose 7% year on year. Adjusted net earnings were up 58% to $329 million, which highlights the operating leverage that gold miners can potentially have when gold prices are rising. Free cash flow for the period was $272 million, up 120% year on year.

Looking ahead, Alamos is expecting to produce between 580,000 to 630,000 ounces of gold in 2025 versus 567,000 ounces in 2024. It expects its all-in sustaining costs (AISC) to be between $1,250 and $1,300 per ounce. Given that the price of gold is currently above $3,400 per ounce, the company appears to be well-positioned in the near term.

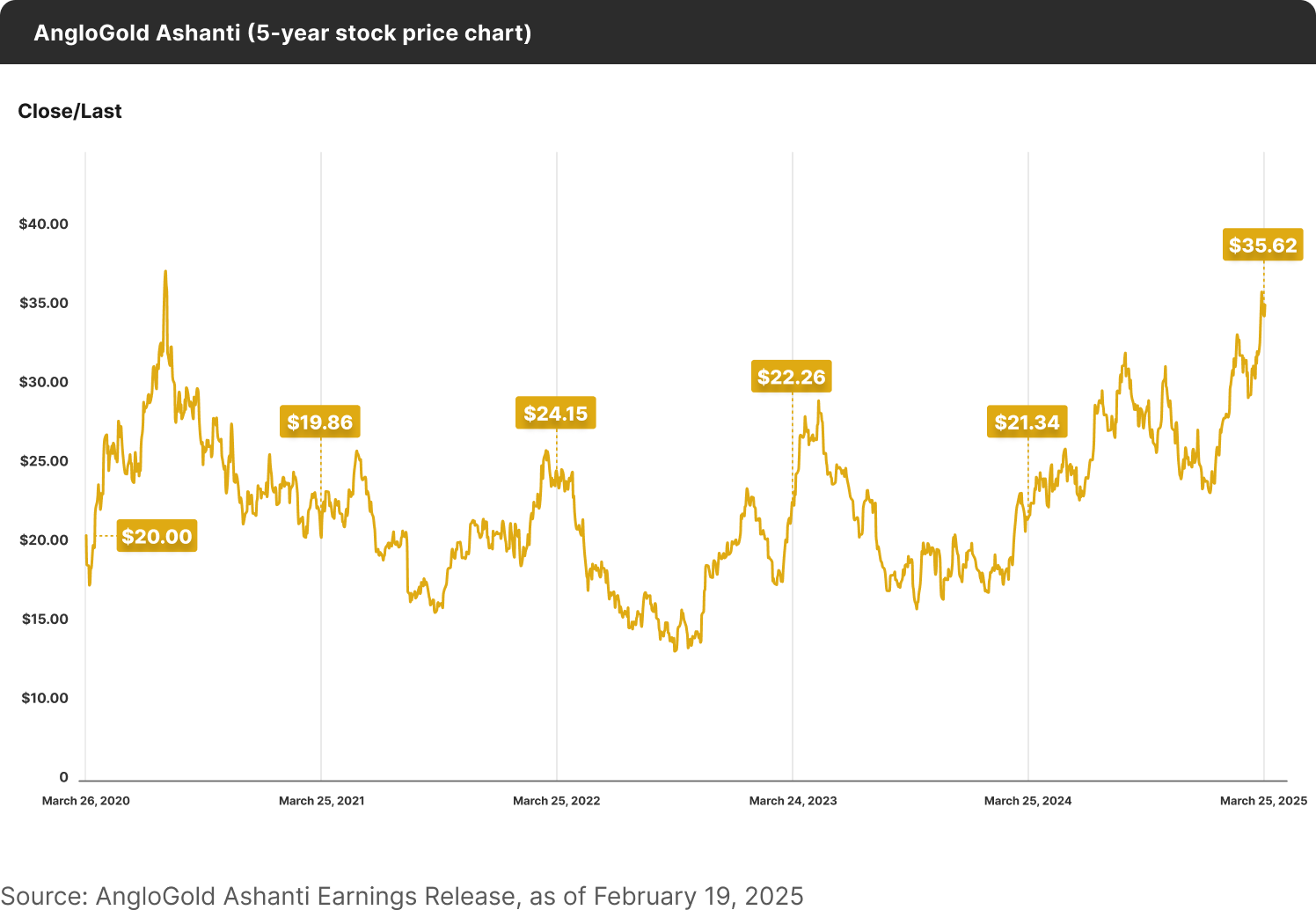

AngloGold Ashanti

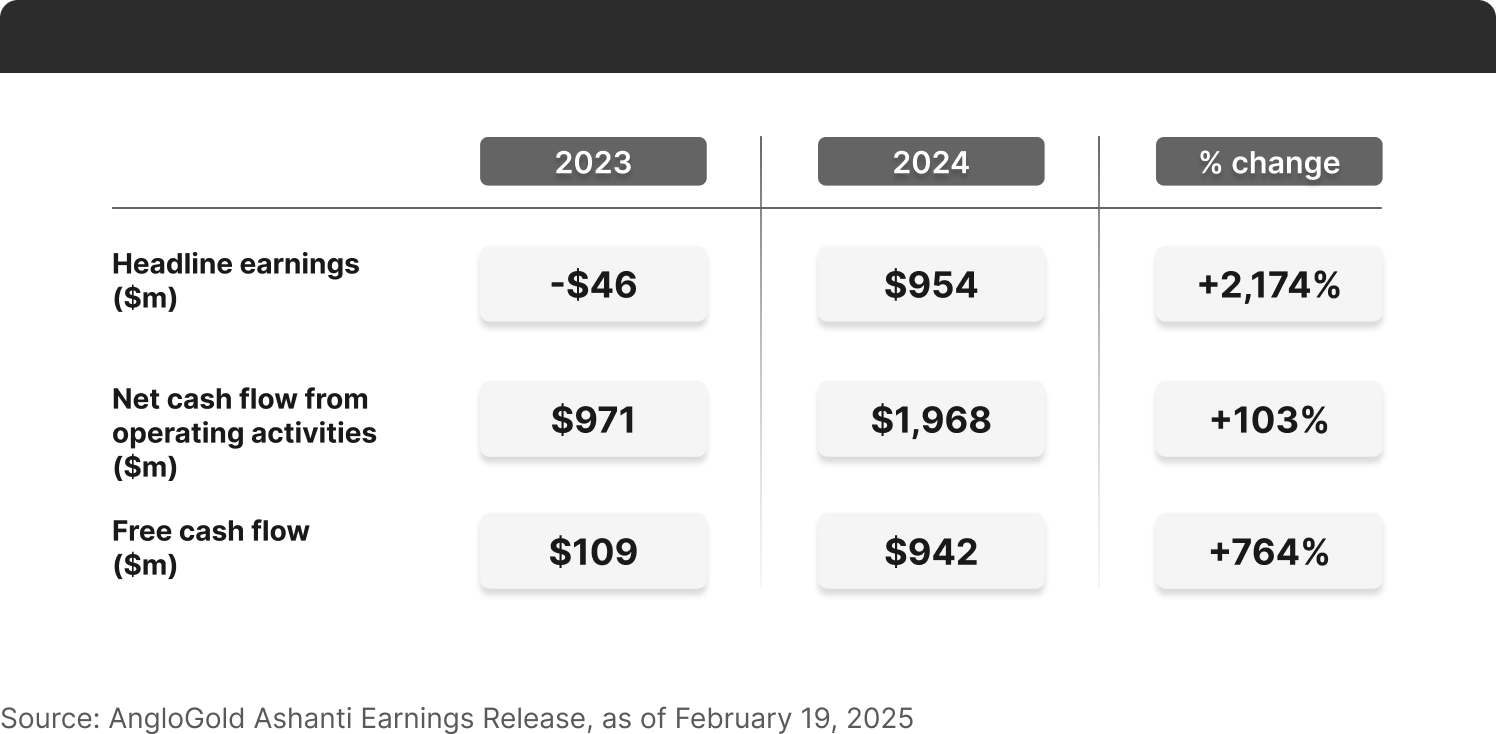

AngloGold Ashanti (5.20%) is another gold miner that has seen its earnings rise recently. It’s a global gold mining company with operations in nine countries including the US, Brazil, Australia, and Egypt, and a primary listing on the NYSE.

Boosted by an average gold price received of $2,653 per ounce, AngloGold Ashanti’s net cash flow from operating activities for the fourth quarter of 20242 was $690 million, up 71% year on year. Headline earnings were $405 million, up 366% year on year.

For the full year, net cash flow from operating activities and headline earnings were $1,968 million (+103% year on year) and $954 million (+2,174%) respectively. This performance enabled the company to reduce its debt pile by 55% and increase its H2 dividend by 263% to 69 US cents per share.

For 2025, AngloGold Ashanti is expecting to produce between 2.900Moz and 3.225Moz of gold versus 2.661Moz in 2024. It expects its AISC for the year to range between $1,580/oz and $1,705/oz.

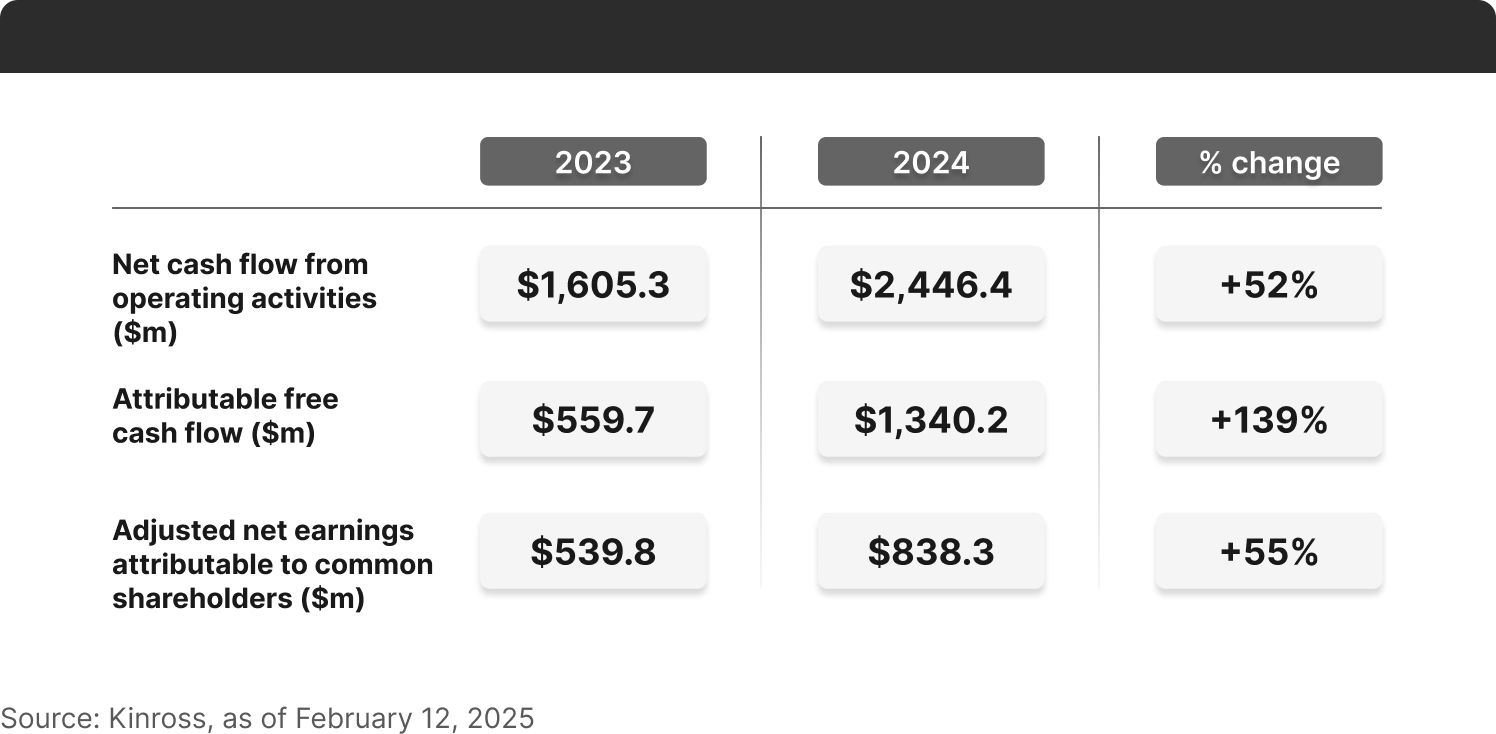

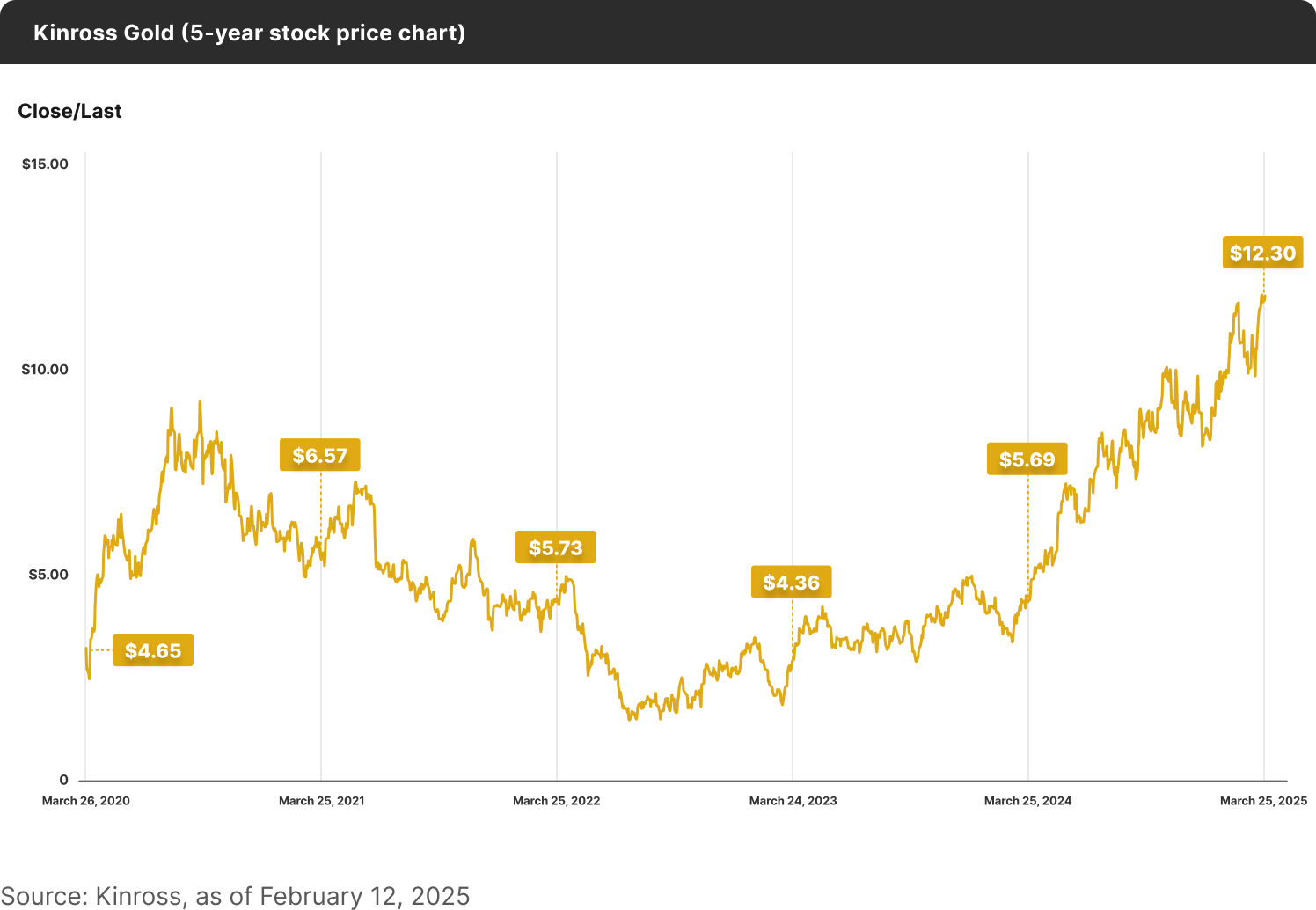

Kinross Gold

Finally, take a look at Kinross Gold (4.91%). It’s an established gold mining company with mines and projects in the US, Canada, Brazil, Chile, and Mauritania and a listing on both the NYSE and the TSX.

For Q4 20243, Kinross posted adjusted net earnings of $240 million ($0.20 per share) versus $140 million ($0.11 per share) a year earlier, helped by an average realized gold price of $2,663 per ounce. Net cash flow from operating activities was $734.5 million versus $410.9 million in Q4 2023.

For the full year, adjusted net earnings per share was $0.68 compared to $0.44 a year earlier while net cash flow from operating activities was $2,446.4 million versus $1,605.3 million in 2023. As a result of this performance, the company was able to repay $800 million in debt, which strengthened its balance sheet.

This year, the company is expecting to produce around 2.0 million ounces of gold. It is forecasting an AISC of $1,500 per ounce.

Investing in Gold Miners Has its Risks

It’s worth pointing out that while these three gold miners have generated higher levels of profitability recently due to rising gold prices, not all gold miners have. In this industry, there can be many obstacles to navigate including operational setbacks, geopolitical instability, environmental liabilities, and the discovery of lower-than-expected ore reserves, and a high gold price is no guarantee of success.

Given that many things can go wrong at individual company level, it can be sensible to diversify when investing in gold mining stocks (although diversification does not guarantee elimination of risk). Diversification can potentially help investors reduce company-specific risks by spreading capital out over a range of different companies.

Footnotes:

1Alamos Gold Inc., Fourth Quarter & Year-End 2024 Results Presentation, as of February 20, 2025

2AngloGold Ashanti Earnings Release, as of February 19, 2025

3Kinross, Kinross reports 2024 fourth-quarter and full-year results, as of February 12, 2025