Article by Edward Sheldon

SpaceX IPO Creates $500 Million Payday for US Banks

June 16, 2026 | Research Insights

The $1.75 trillion SpaceX IPO has been lucrative for a broad range of stakeholders. Beyond generating substantial wealth for long-term backers, retail investors, and employees, the deal represents a massive windfall for Wall Street. According to CNBC1, banks involved in the IPO are set to pocket an estimated $500 million in fees. So, we could be looking at strong earnings from these financial institutions in the near term.

A Huge Windfall for the Banks

SpaceX raised $75 billion2 in its IPO by selling 555.6 million shares at $135 each. The deal valued the space powerhouse near $1.75 trillion at pricing.

Fees paid to banks who underwrote the deal amounted to around 0.67%3 of the $75 billion. That translates to approximately $500 million in commissions.

According to CNBC, Goldman Sachs and Morgan Stanley – who were the lead underwriters and shouldered the vast majority of the institutional heavy lifting for the blockbusting listing – are set to pocket fees of around $100 million apiece. Meanwhile, Bank of America, Citigroup and JP Morgan, who also played a role in the offering, are set to land about $75 million each.

Note that prior to this IPO, the biggest underwriting payday from an individual stock listing was $300 million4. This was the amount generated by the banks from Alibaba’s 2014 IPO.

Multiple Benefits for Goldman Sachs

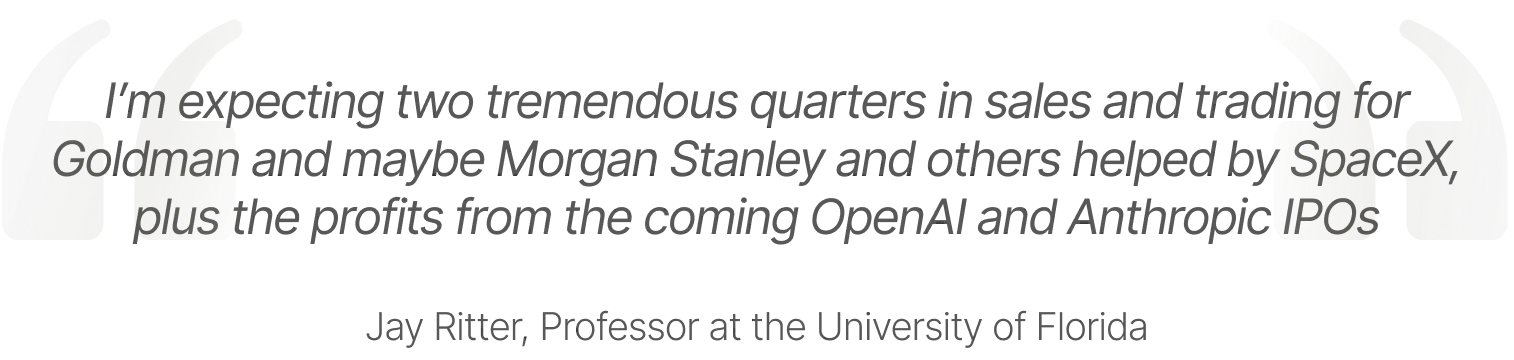

It’s worth pointing out that hedge funds and other money managers who receive allocations in a successful IPO (and benefit from immediate risk-free gains) often return some of their gains to the lead underwriters in “soft dollars” – fees paid for trade execution that exceed the actual cost of executing the trades. According to Jay Ritter4 (aka “Mr IPO”), a professor at the University of Florida who is an expert in IPOs, about 30% of first-day profits typically come back to the bankers in soft dollars, with most of this going to the lead underwriter.

So, Goldman Sachs – who was the left lead underwriter on the SpaceX Prospectus – is likely to have profited handsomely from the event. Given that SpaceX stock rose almost 20%5 on the first day of trading and those who were allocated stock in the IPO generated significant gains, the firm will most likely have received a substantial amount of soft dollars from clients.

One other thing to note is that the IPO was very successful in terms of pricing and post-IPO gains. In institutional finance and underwriting, a 20% post-IPO gain is widely considered the "sweet spot" because it perfectly balances the competing interests of the three major parties involved: the company going public, the early investors, and the investment banks.

The fact that it was so successful puts Goldman Sachs in a strong position for upcoming IPOs such as Anthropic and OpenAI. Ultimately, it could be a very big year for the bank in terms of investment banking fees.

Bank Stocks: The Outlook is Promising

In light of all this, the next few quarters could be very strong for the major US banks. Combine investment banking fees with trading revenues and wealth management income, and you have a recipe for strong bottom-line expansion that could easily outpace consensus estimates.

Those looking for exposure to the banking industry may wish to explore the Themes Global Systemically Important Banks ETF (GSIB). This offers exposure to a range of bank stocks for a low ongoing fee of 0.35%.

Footnotes:

1CNBC, SpaceX IPO takeaways: SPCX closes at $161, jumping 19% after record debut, as of June 13, 2026

2CNBC, SpaceX raising $75 billion in record-setting IPO as Nasdaq debut awaits, as of June 11, 2026

3Yahoo Finance, SpaceX Strikes Rare Deal to Pay $0 to Bankers for IPO Greenshoe, as of June 13, 2026

4Fortune, SpaceX lowballed its bankers on fees. Goldman Sachs has another way to win big, as of June 11, 2026

5Google Finance, as of June 15, 2026

Author is a contractor of Leverage Shares LLC, a U.S. affiliate of Themes Management Company LLC. Leverage Shares LLC provides certain services to Themes under an intercompany services agreement.