April 23, 2025

Trump’s “Liberation Day” Tariffs Might Last Several Years

The 2nd of April 2025 was proclaimed by President Trump as “Liberation Day” wherein the U.S. government announced a host of sweeping tariff hikes1 across the board with all of America’s trading partners. These tariffs announced were by far the most sweeping set of hikes announced since the Smoot-Hawley Tariff Act in 1930. What boggled the minds of most economists were the claims made about the “casus belli”: tariffs being levied by other countries on U.S. goods, examples of which were shown to the media on a board wherein the first column held the names of select countries, the second column was titled “Tariffs Charged to the U.S.A. Including Currency Manipulation and Trade Barriers” and the third column was titled “U.S.A. Discounted Reciprocal Tariffs”.

Source: U.S. White House, as of April 2, 2025

Source: U.S. White House, as of April 2, 2025

Source: U.S. White House, as of April 2, 2025

Source: U.S. White House, as of April 2, 2025

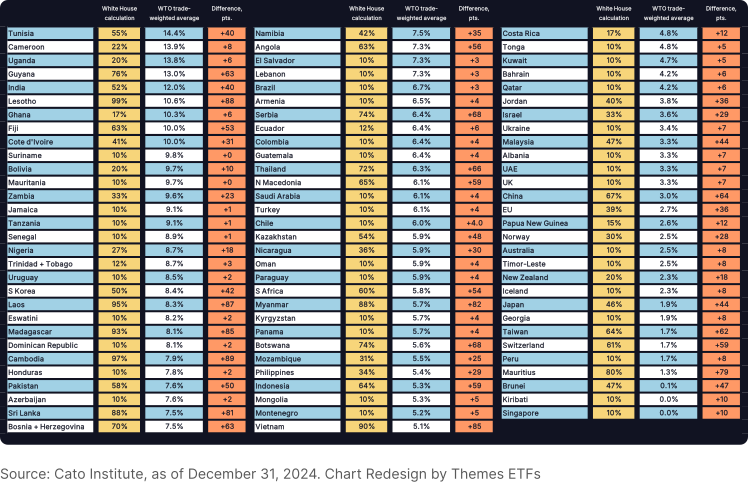

However, in virtually every case — and even when mostly considered on a weighted-average basis (outside of a handful of goods) — actual import duties levied are nowhere close to those stated in the second column. For instance, the Cato Institute estimated2 that the 2023 trade-weighted average tariff rate from China was 3%, but the Trump administration said it was 67%. Similarly, the administration said India imposes a 52% tariff on the U.S., but Cato found that India’s 2023 trade-weighted average tariff rate was 12%.

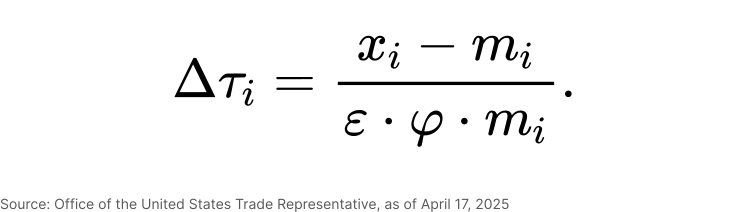

Now, with respect to the third column, the Office of the United State Trade Representative (USTR) stated3 that the tariffs assigned to each country was calculated on the basis of a formula:

wherein ∆τ represents the change in tariff rate for country “i” while “x” and “m” stand for exports to and imports from country “i” respectively. Meanwhile, “ε” is a factor calculated as the elasticity of import demand with respect to import prices and “φ” is the elasticity of import prices with respect to tariffs. These factors are set at 4 and 0.25, respectively, which effectively cancel each other out. The total tariff estimated is then discounted by 50%, which the White House described as being “very kind”4 to the countries on which these were levied.

Minus the discounting, this formula (as it stands) represents the trade gap relative to imports — which doesn’t really translate to a decision-enabling metric for a tariff decision. The center-right think-tank American Enterprise Institute for Public Policy Research (or simply the “American Enterprise Institute”) examined the literature5 associated with the formula employed by the USTR and determined that “φ” should be set at 0.945 rather than 0.25, since the tariffs seem to be based on the elasticity on the response of retail prices to tariffs, as opposed to import prices. If it were based on import prices, the highest tariff rate levied by the U.S. would be around 14% after discounting — essentially the same rate that the country with the highest weighted-average tariff for U.S. goods in 2023 (Tunisia) charges.

Thus, the “formulaic” argument for tariff calculation doesn’t stand up to scrutiny. However, in terms of policy, this points towards a rubric being mooted as a possible strategy by the administration — dubbed the “Mar-a-Lago Accord”.

Drop the Dollar, Bring Back Manufacturing?

The phrase “Mar-a-Lago Accord”, coined by former Credit Suisse Strategist Zoltan Poszar in June 2024, references the 1985 “Plaza Accords” where France, Japan, West Germany and the United Kingdom agreed with the United States to jointly weaken the U.S. dollar in order to rein in the U.S. trade deficit and maintain American competitiveness in the global market. Mr. Poszar largely framed this idea using the arguments made by President Trump on the campaign trail around the idea that the U.S. could force countries to accept a weaker dollar and lower interest rates on their U.S. Treasury investments in exchange for protection by the U.S. military (effectively combining elements of the Plaza Accords with the Nixon-era deals made nearly a decade prior that had extended U.S. military protection to several OPEC countries in exchange for them exclusively adopting petrodollar contracts).

In November 2024, Dr. Stephen Miran — Senior Strategist at Connecticut-based hedge fund Hudson Bay Capital — expanded on this idea6 in a paper which run relatively under the radar until he was appointed as Chairman of the President’s Council of Economic Advisors. Since then, economists and strategists have been matching the rhetoric with the ideas explored both by the paper as well as the President’s worldview.

According to the President, a strong dollar had led to the dismantlement of the U.S.’ once-vast manufacturing industry. As far as trends go, there is a certain level of correlation here:

As per the USTR, the tariff rates were computed to drive bilateral trade deficits to zero. An inability to balance deficits, it continues, had led to “the closure of more than 90,000 American factories since 1997, and a decline in our manufacturing workforce of more than 6.6 million jobs, more than a third from its peak.”

Needless to say, these numbers are heavily disputed. Longitudinal data are relatively difficult to come by but there are “windowed” studies that belie this. For instance, as per a well-received study published in 2017 by Ball State University researchers Hicks and Devaraj, most manufacturing job losses in the period between 2000 and 2010 were due to increasing automation and skills leveling up:

In other words, it wasn’t the Chinese (or Indian or Vietnamese) worker who caused job losses in the U.S.; it was mostly mechanization and the more-efficient coworker on the production line. U.S. manufacturing output actually increased in absolute terms by roughly 20% between 2000 and 2020, despite a substantial employment decline. Almost 88% of job losses in manufacturing in recent years can be attributable to productivity growth, and the long-term changes to manufacturing employment are mostly linked to the productivity of American factories.

This was backed by the “Caliendo, Dvorkin, and Parro trade model”7 published in 2019 by eminent researchers in Yale, Johns Hopkins University and the Federal Reserve who established that, even in the earlier period that Hicks and Devaraj considered for statistical analysis wherein manufacturing losses might be construed as being relatively higher when compared to the more recent past, losses due to outsourcing towards foreign shores such as China was only about 16%. What makes American exports — which could unlock manufacturing growth — less competitive against global peers is the high dollar value.

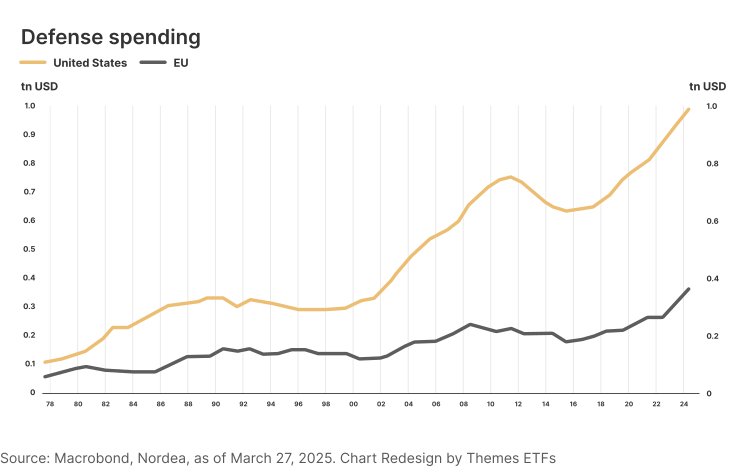

While manufacturing jobs as a percentage of the total workforce reduced, one sector that remained resilient was the U.S. armaments industry. Rising U.S. debt show a very strong correlation with rising U.S. spends on its military, which the U.S. government ostensibly states it does to meet its obligations around the world:

Relative to its well-heeled NATO allies in Europe, the U.S. has been increasingly outspending all of them combined for around 50 years now.

This forms the crux of the doctrine behind the U.S. administration demanding that its NATO peers spend a lot more on their part. While this intuitively makes sense given the gap, the consequences for the armaments industry are striking since the European Union (E.U.) has now proposed rules8 to ensure that E.U.-based manufacturers be the dominant (if not exclusive) beneficiaries of the increase in spending; U.S. and U.K-based companies could effectively be out of consideration for the most part. This sparked an immediate response from Secretary of State Marco Rubio who reportedly said9 that any exclusion of U.S. companies from European tenders would be seen negatively by Washington.

The U.S. administration has been hard at work at trying to hock American military gear to new buyers. During a working visit (a sort of informal meeting that is more of a “Hello” rather than an ‘official’ state visit) by India’s Prime Minister Narendra Modi in the wake of President Trump’s reelection, the President offered India F-35 fighter jets (priced at roughly $100 million apiece) — a move that drew strong objections within India, given the jets’ rated “full mission capable rate” of only 30%10 as of 2023 (while the benchmark for any credible air force is at least 65%), the nearly $2 trillion11 (and rising) operational costs that plagues the U.S. military and its potential to forestall a vast domestic ecosystem on the verge of developing a fully-indigenous fifth-generation jet. The working visit amicably concluded without a positive response from the Indian government.

There's More to Come

In his paper (which he was careful to state was not to be considered as “Policy Advisory”), Dr. Miran stated that a massive consequence of the U.S. serving as the world’s reserve producer is that reserve demand for American assets (both cash as well as Treasury assets) pushes up the dollar, leading it to levels far in excess of what would balance international trade over the long run. Since nations accumulate reserves in part to stem appreciation pressures in their own currencies, there is a contemporaneous negative correlation between the exchange value of the dollar and the level of global reserves. Because the reserve asset is “safe,” the dollar appreciates during recessions while other nations’ currencies tend to depreciate — meaning their exports become cheaper while U.S. competitiveness erodes. Dr. Miran postulates that a mixture of tariffs and currency policy might help preserve American competitiveness in high-value-added manufacturing, these sectors aren’t known to be high-volume employment generators.

Meanwhile, in the very study that the USTR referenced as the basis of the tariffs, the authors Cavallo, et al highlighted (as a case in example) from past instances that, say, 10% tariff would be associated with a 0.6% lower ex-tariff price (i.e. at the exporters’ end) and a 9.4% higher overall price faced by the importer — which is inevitably passed down to the consumer. When retaliatory tariffs were announced by the exporters’ country, however, a 10% tariff imposed on US exports reduces US ex-tariff export prices by about 3.3%. This is a repeated pattern that indicates that a “strong” dollar essentially teeters U.S. exports to the brink of non-competitiveness, forcing exporters to slash prices or exit altogether — which could go on to impact employment numbers. Given how outsized the imposed tariffs have been on the U.S.’ trading partners, retaliatory tariffs are essentially inevitable. The hiked tariffs have begun to be levied12 across U.S. ports as of the 5th of April.

If petrodollar contracts, nearly-consistent top-tier ratings to U.S. Treasury debt and successive U.S. governments’ insistence on enshrining the U.S. dollar (and debt assets) into the world’s reserves hadn’t been in place, the tariff system might have created room for parley and discussion. When left intact (i.e. if the currency policy is left as-is), tariffs become a sword’s edge against America’s industrial base and workforce itself. Given that President Trump has even threatened countries13 of increased tariffs if they were to “de-dollarise” their reserves, the U.S. administration’s only option would be to pursue currency depreciation via tariffs over a period of several years. The Plaza Accords took two years before the U.S. dollar depreciated with the assistance of major trading partners; in this day and age, the number of trading partners and debt holders are manifold, complex, heavily distributed, and disinclined to assist for various reasons.

As it stands, the tariffs will be a tax on the American consumer. It is likely for that reason that the U.S. administration announced a 90-day halt on tariffs – with China excluded – on the 9th of April14 and then announced a further relaxation of specific goods15 (mostly phones, computers and related electronics) on the 12th. However, the U.S. administration is likely to tighten these

Massive bouts of choppiness in the U.S. markets and ripple effects elsewhere can be expected as the tariff war ratchets up. The actions in the war won’t just be Washington’s call; measures are also being deliberated upon and a series of actions can be expected from Brussels, Beijing, Tokyo, and New Delhi in several ways.

Footnotes:

1“Regulating Imports with a Reciprocal Tariff to Rectify Trade Practices that Contribute to Large and Persistent Annual United States Goods Trade Deficits”, U.S. White House, 2 April 2025

2“Tariff rates Trump ascribes to other countries are vastly higher than World Trade data shows”, CNBC, 4 April 2025

3“Issue Areas: Reciprocal Tariff Calculations”, Office of the U.S. Trade Representative

4“Economists take issue with Trump’s tariff formula, arguing rate is inflated”, CNBC, 5 April 2025

5“President Trump’s Tariff Formula Makes No Economic Sense. It’s Also Based on an Error.”, American Enterprise Institute, 4 April 2025

6“A User’s Guide to Restructuring the Global Trading System”, Hudson Bay Capital, 12 November 2024

7“Trade and Labor Market Dynamics: General Equilibrium Analysis of the China Trade Shock”, Econometrica: Journal of the Econometric Society, Volume 87, Issue 3, May 2019

8“Explainer: Can non-EU companies be part of EU's big defence fund?”, Reuters, 21 March 2025

9“US officials object to European push to buy weapons locally”, Reuters, 2 April 2025

10“View: Why India should say no to Trump’s offer of F-35 fighter jets”, Economic Times, 17 February 2025

11“Donald Trump’s F-35 pitch to India: Will it be a $2 trillion problem in disguise?”, Economic Times, 15 February 2025

12“US starts collecting Trump’s 10% tariff, smashing global trade norms”, Reuters, 6 April 2025

13“Trump repeats tariffs threat to dissuade BRICS nations from replacing US dollar”, Reuters, 31 January 2025

14“Trump temporarily drops tariffs to 10% for most countries, hits China harder with 125%”, CNBC, 9 April 2025

15“Trump exempts phones, computers, chips from new tariffs”, CNBC, 12 April 2025