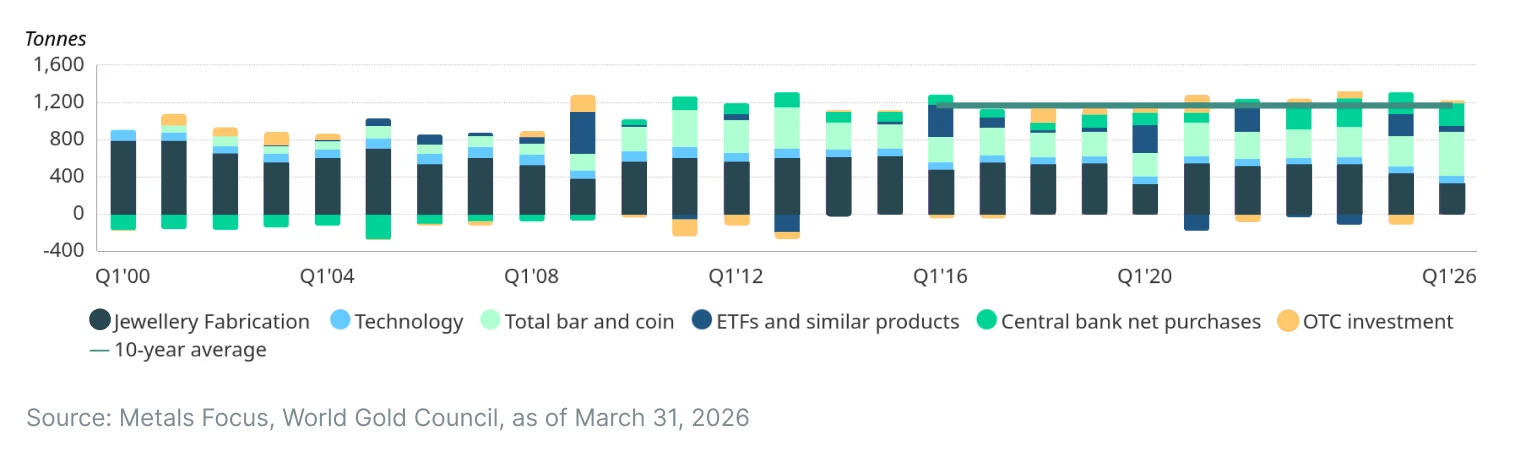

By the end of Q1 2026, overall gold demand in volume was only a modest 2% higher in year-on-year terms. Buy-ins into physical gold bars and coins represented the biggest share of total purchases1 made in Q1 2026 in all of the 21st century.

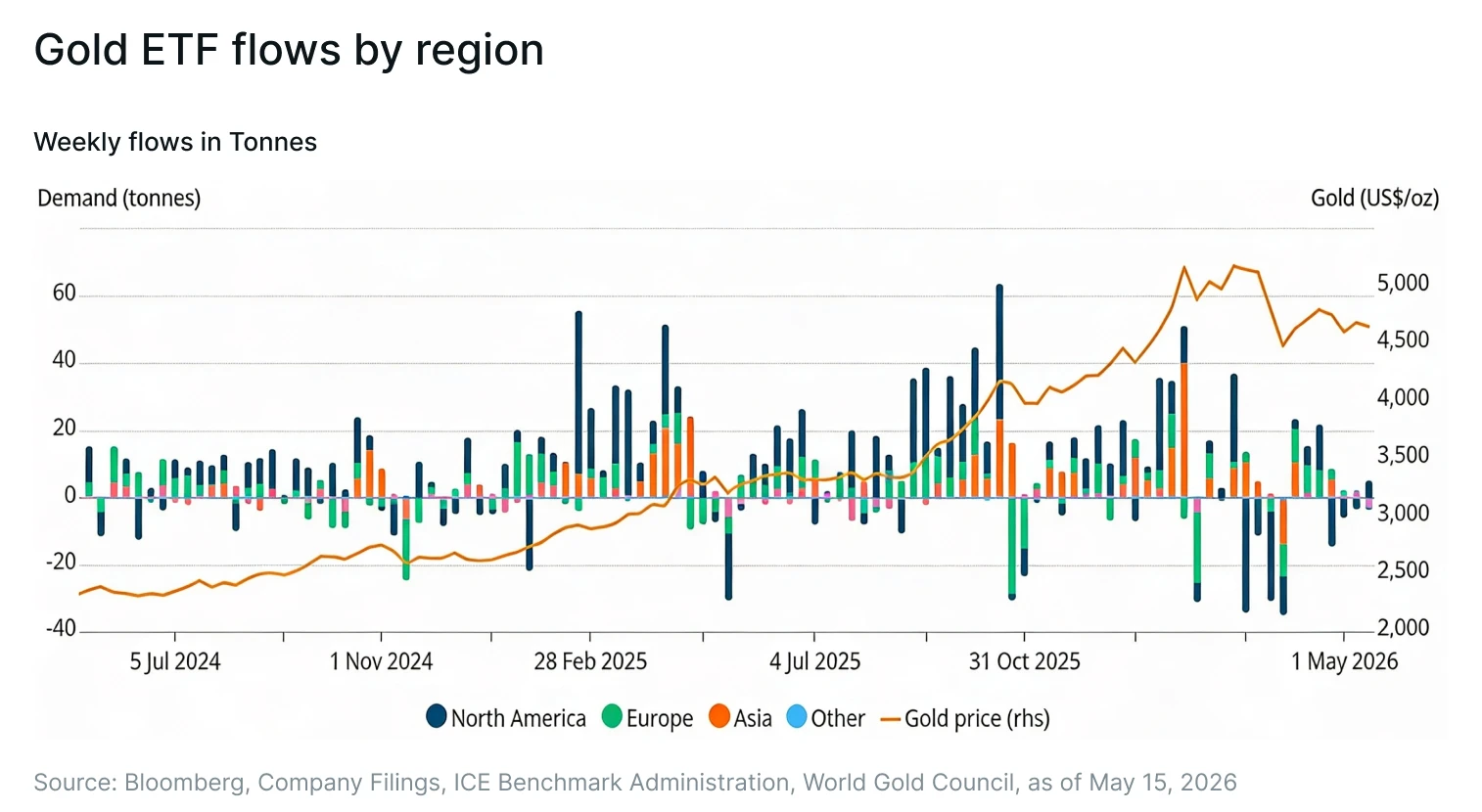

The buying of gold – and its consideration as an investment asset class – had appeared appearing differentiated through geopolitics and traditional preferences. While Western investors mostly turned away – likely in favour of AI-relevant stocks, energy products, and so forth. Asian investors bought in at substantial strength: Chinese investors had supplanted the US as the biggest set of buy-ins into Gold ETFs in net tonnes as falling local equity markets, weakening of currency and a drive for safe‑haven buying propelled interest. US investors, in contrast, were net sellers.

Meanwhile, despite profit-taking in the second half of Q1 2026, Indian investors had registered a net increase for Q1 2026 – with a fair amount of dip-buying manifesting in March.

Japanese investors had also consistently contributed to AUM via both local gold-backed funds and funds investing in gold ETFs listed in other regions.

In April 20262, however, the West once again became net buyers while Asian investors – led by China – sold off.

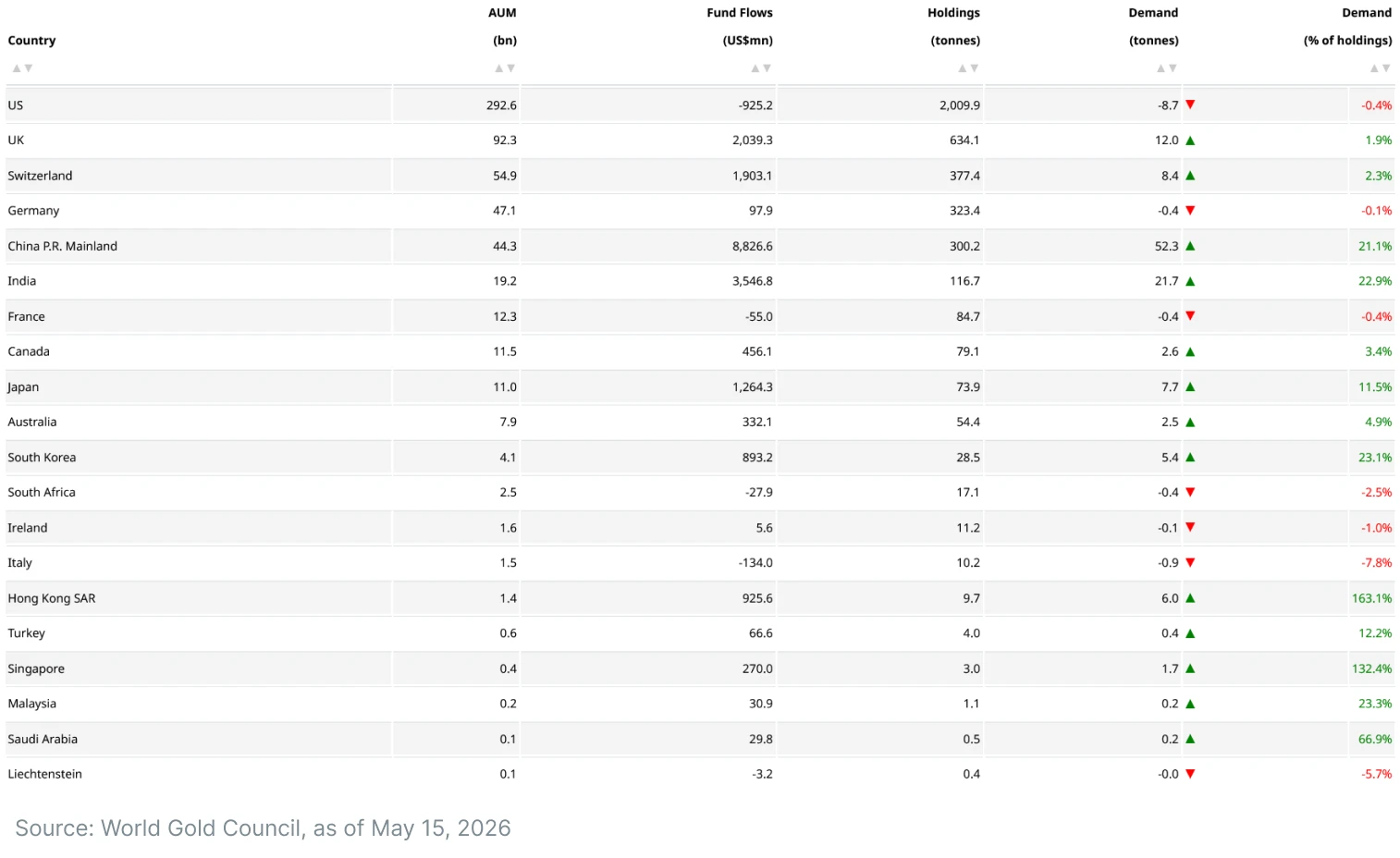

While U.S. funds have the largest reported fund holdings by tonnage, demand still reads soft in the Year Till Date (YTD) – given the outflows in Q1 2026. By contrast, Indian and Chinese funds are running neck and neck in terms of demand across the same period.

One massive development is that Hong Kong and Singapore funds – both operating in Asian markets with favourable tax rates along with strong linkages to and appetite for both Western tickers and high-conviction Chinese tech names have seen a three-digit increase in favour.

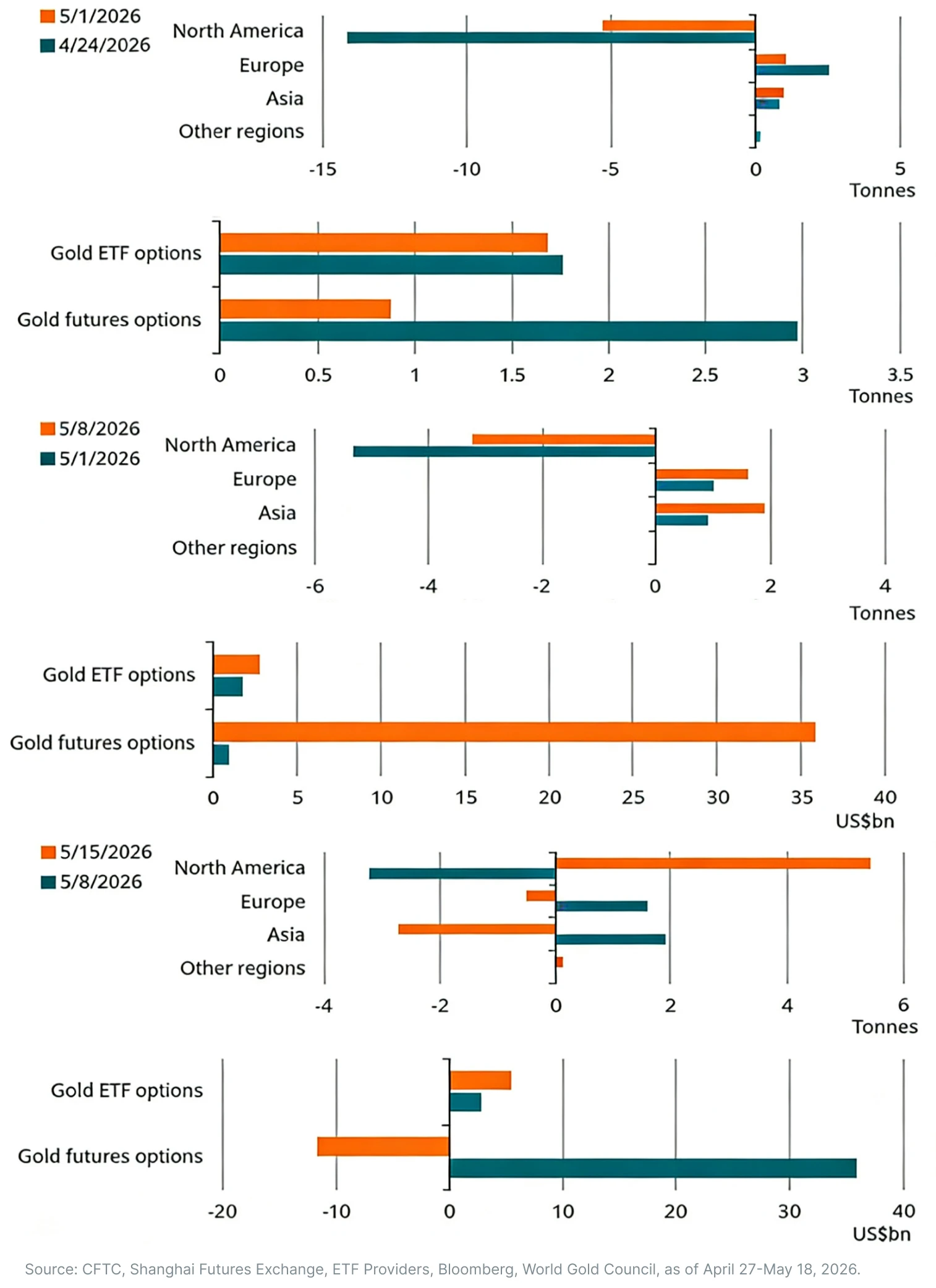

While European funds led in the buy-ins in April, US funds entered in strength3 on the week ending May 15 2026:

A substantial portion of the gold buy-ins is likely correlated with the precipitous drop in futures options volume as investors moved to “hold” rather than “possibly choose to hold”.

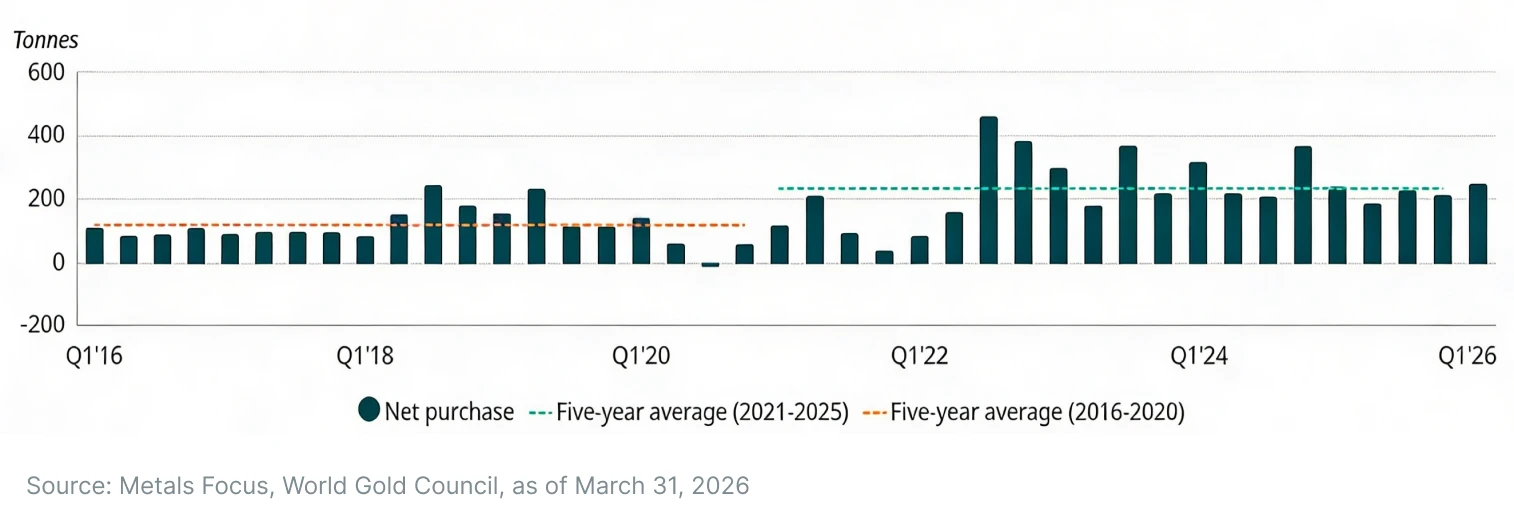

Central Banks’ Gold Trends

Q1 2026 ended with global central banks estimated to have purchases around 244 tonnes

However, not all central banks were aligned in quite the same directions: Developed Economies continued to repose on US Treasury holdings while Emerging Markets economies – particularly those not part of the U.S. security umbrella – continued to buy into gold as a means of “de-risking”.

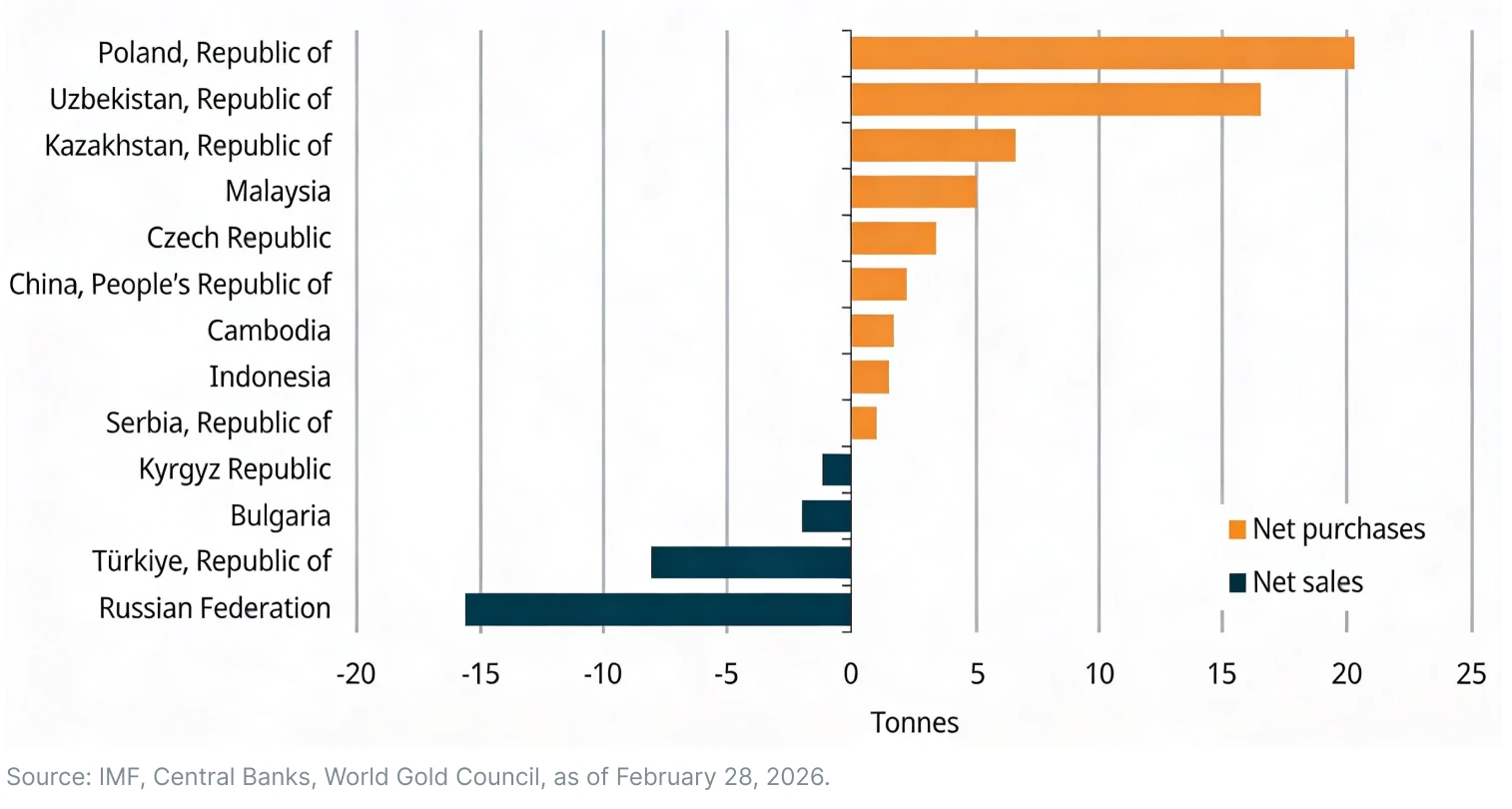

In data for the quarter through February4, gold selling was led mostly by the central banks of Türkiye and Russia.

Meanwhile, the National Bank of Poland was the largest buyer of gold in Q1 2026 at 31 tonnes. The central bank appears to be fixed on its goal of reaching 700 tonnes (it’s currently at around 582 tonnes).

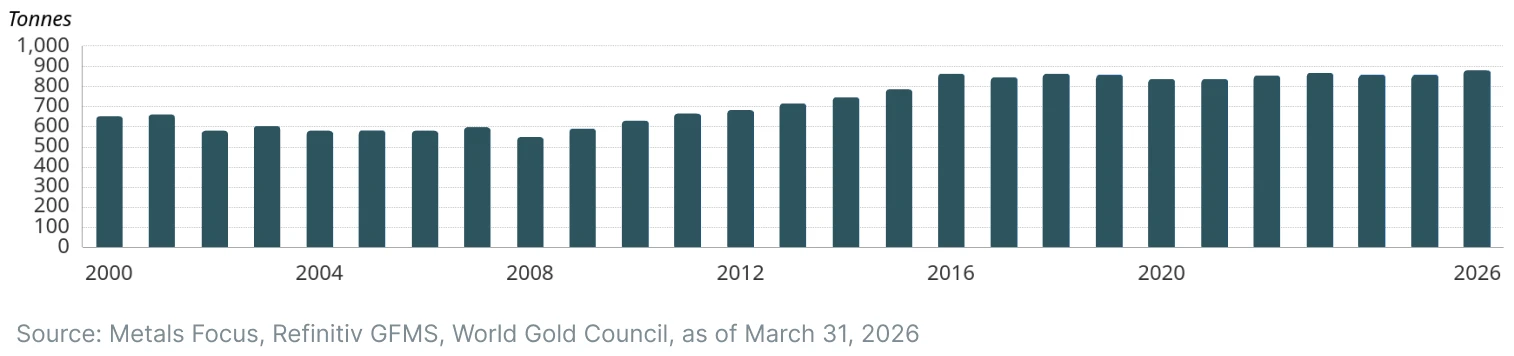

Meanwhile, the supply of gold via mining saw a modest increase: Q1 2026 was in all-time high in the 21st century in terms of gold production in the first quarter of the year.

The End of “Global Order”?

Given that central banks are grappling with supply shocks in their economies from the war in the Middle East, the pressure on government bonds – leading to a rise in yield – are likely to remain elevated until a clearer path for policy rates emerges. The clearest indicator of this is the spike in US 30-Year Treasury yields almost perfectly coinciding with the massive spike in gold buy-ins via US funds.

With central banks increasingly buying into gold amidst a non-trivial likelihood of the post-Cold War global order fragmenting, the selloff in long-term US Treasuries (resulting in a rise of yields) is a natural outcome. The non-triviality of the likelihood is perhaps best exemplified by India, a rapidly growing global power that moves with great deliberation before every step it takes – and one wooed with progressively increasing conviction by Western powers since the end of the Cold War and the advent of the technology age.

As of March 2023, the Reserve Bank of India had5 348.6 tonnes of its gold deposited in the Bank of England (BoE) and the Bank for International Settlements (BIS) in Switzerland. Since March 2023 through September 2025, 274 tonnes of gold were repatriated into vaults distributed across India while the central bank continued to buy gold assets globally.

One possible scenario being modelled is the treatment of Russian assets in the immediate aftermath of the present Russo-Ukrainian conflict breaking out. Even if the conflict were to end, Russia likely faces an uphill battle in recovering all of its assets. This is a situation any sovereign central bank could reasonably be expected to avoid – especially if fragmentation is deemed a given.

If the AI Hype were to fade among retail investors – with questions swirling on whether the churn seen in AI-relevant instruments are being influenced by stock repurchases and Stock-Based Compensation (“SBC”) activity – then the current yields seen in Treasuries would act as an additional tailwind for buy-ins into gold and other storehouse metals. In addition, persistence in Middle Eastern conflicts practically ensures that the energy supply situation would continue to be volatile as inflation would continue to eat away at purchasing power in the Western Hemisphere. Here too – and more so than government debt – the allure for gold is likely to be burnished further.

Central bank demand alone is likely to provide strong structural support for further growth in the mining of gold. With institutional and retail demand added to this, there is ample cause to estimate a rosy outlook for gold mining companies. Thus, we believe that there is strong cause for investors to consider the Themes Gold Miners ETF (AUMI) anew. AUMI seeks to track the Solactive Global Pure Gold Miners Index (SOLGLPGM), which identifies the largest 30 companies by market capitalization that derive their revenues from gold mining.

Footnotes:

1World Gold Council, Gold Demand Trends: Q1 2026, as of April 29, 2026

2World Gold Council, Gold ETFs, holdings and flows, as of May 18, 2026

3World Gold Council, Weekly Markets Monitor, as of April 27, 2026, May 11, 2026, May 18, 2026

4World Gold Council, Central Bank Gold Statistics: Central banks stay the course on gold in February, as of April 2, 2026

5FirstPost, How and why RBI is flying more of India's gold back home, as of October 29, 2025

Author is a contractor of Leverage Shares LLC, a U.S. affiliate of Themes Management Company LLC. Leverage Shares LLC provides certain services to Themes under an intercompany services agreement.