Article by Edward Sheldon

Wealth Management Revenues Bolster US Banks’ Q4 Earnings

January 21, 2026 | Research Insights

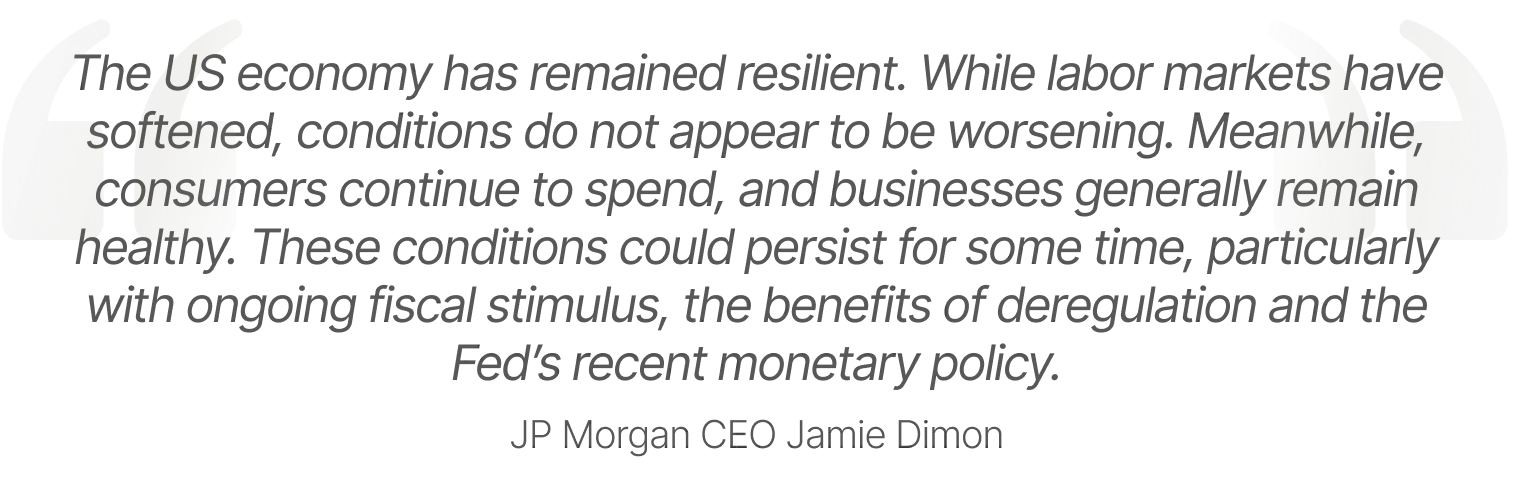

US banks have enjoyed a Goldilocks-type environment over the last few quarters, benefiting from falling interest rates, stable consumer credit, rising equity markets, and a pickup in capital markets activity. As a result, bank stocks have generated strong returns for investors. Recently, the “Big Six” US banks posted their earnings for the fourth quarter of 2025, offering a snapshot of their performance in this favorable environment. Here’s a look at the highlights.

JP Morgan

JP Morgan was the first of the Big Six US banks to post its Q4 earnings1 and it set the scene with a solid print. For the quarter, revenue was $46.8 billion versus the consensus forecast2 of $46.2 billion, while adjusted earnings per share (EPS) was $5.23 per share versus $5.00 expected (excluding a $0.60 charge related to the purchase of Apple’s credit card portfolio). Net interest income for the period was $25.1 billion, up 7% year on year, while return on tangible common equity (RoTCE) was 18%. Provision for credit losses jumped to $4.7 billion versus $2.6 billion a year earlier but this included a $2.2 billion credit reserve for the Apple credit card deal.

One highlight of JP Morgan’s Q4 earnings was its Markets & Securities Services division, which encompasses its equity and fixed income sales and trading operations as well as its custody and asset servicing business. In this division, revenue was up 17% year on year to $8.2 billion, thanks to a strong performance in Equity Markets. Wealth management was another driver of performance for the firm, however. Here, assets under management rose 18% year on year to $4.8 trillion, leading to $6.5 billion in revenue, a 13% increase year on year.

A weak spot in JP Morgan’s earnings was investment banking fees – these fell 5% year on year to $2.3 billion. However, for 2025, the bank held the number one ranking for global investment banking fees with an 8.4% wallet share.

Wells Fargo

Wells Fargo posted fourth-quarter3 revenue of $21.3 billion, up 4% year on year but below Wall Street’s forecast4 of $21.6 billion. Earnings per share were better than expected though, coming in at $1.76 versus the estimate of $1.66. Net interest income for the period was $12.3 billion, 4% higher year on year while RoTCE was 14.5%. Provision for credit losses was $1.0 billion versus $1.1 billion a year earlier.

With global equity markets ending the year near all-time highs, Wells Fargo saw good results in its Wealth and Investment Management division in Q4. Here, revenue was up 10% year on year to $4.4 billion. The company’s Consumer Banking and Lending unit also performed well, however. In this division, revenue was up 7% year on year to $9.6 billion thanks to a jump in revenues in the firm’s Credit Card division.

It’s worth noting that like JP Morgan, Wells Fargo did not see strong results in investment banking in Q4. In this division, revenues were flat year on year at $4.6 billion.

Bank of America

Bank of America’s Q4 earnings5 topped analysts’ expectations thanks to rising net interest income, asset management fees, and trading revenue. For the quarter, revenue was $28.5 billion versus $27.9 billion expected while EPS was $0.98 versus $0.96 cents expected6. Net interest income increased 9.7% to $15.9 billion while RoTCE came in at 14%. Provision for credit losses was $1.3 billion versus $1.5 billion a year earlier.

Equities trading was a strong point for Bank of America in Q4. Here, revenue rose 23% year on year to $2.0 billion. However, the company’s Global Wealth and Investment Management unit also performed very well. In this division, client balances rose 12% to $4.8 trillion – driven by higher market valuations and positive net client flows – leading to $6.6 billion in revenue, up 10% year on year.

In BoA’s Global Banking division, investment banking fees were $1.7 billion, up 1% year on year. For the year, the company was the number three player in investment banking fees.

Citigroup

Citigroup also posted fourth-quarter results7 that topped expectations, with both revenue and earnings per share exceeding forecasts. Adjusted revenue was $21.0 billion versus the consensus forecast of $20.7 billion while adjusted EPS was $1.81 per share versus $1.67 expected8 (note that this adjusted EPS figure excluded a $1.1 billion after-tax loss tied to its plan to divest its Russian operations). Net interest income for the period rose 14% year on year to $15.7 billion, while RoTCE was 5.1%. Total provision for credit losses was $2.2 billion versus $2.6 billion a year earlier.

In Q4, several divisions at Citigroup performed well. Investment Banking was a standout – revenue here increased 38% to $1.3 billion, driven by growth in Advisory and Debt Capital Markets (DCM). Wealth was another strong point for the bank with revenues here rising 7% year on year to $2.1 billion, driven by a 14% increase in client assets.

Goldman Sachs

Goldman Sachs’ fourth-quarter9 revenue of $13.5 billion was a little below the $13.8 billion figure expected. However, EPS of $14.01 per share was well above the consensus forecast10 of $11.67, even when taking into account a preannounced $0.46 per share gain from Goldman’s sale of its Apple Card business. Net interest income for the quarter was $3.7 billion versus $2.3 billion a year earlier while return on average common shareholders' equity was 16.0%. Provision for credit losses was a net benefit of $2.1 billion compared with net provisions of $351 million for the fourth quarter of 2024.

Equities was a highlight for Goldman Sachs in Q4, with revenue here coming in at $4.3 billion, up 25% year on year, due to significantly higher net revenues in prime financing and portfolio financing. Yet performance in the group’s Fixed Income, Currency, and Commodities (FICC) unit was also strong. Here, revenue amounted to $3.1 billion, up 12% year on year, on strength in wagers tied to interest rates and commodities.

Zooming in on the firm’s investment banking division, revenues here amounted to $2.6 billion, 25% higher than in the fourth quarter of 2024. This strength was fueled by significantly higher net revenues in Advisory, reflecting a substantial increase in completed mergers and acquisitions volumes as well as growth in debt underwriting.

Morgan Stanley

Morgan Stanley posted a strong fourth-quarter11 print that was ahead of forecasts. For the period, revenue was $17.9 billion versus $17.8 billion expected12 while EPS was $2.68 versus the consensus forecast of $2.44. RoTCE for the period was 21.8% – the highest among the big five money center banks. Provision for credit losses was $18 million versus $115 million a year earlier.

Investment banking was a standout area for Morgan Stanley. Here, net revenue surged 47% year on year to $2.4 billion thanks to a large increase in fixed income underwriting revenues. Wealth management also performed very well though. This unit posted $8.4 billion in net revenue for the quarter, up 13% year on year, with total client assets rising to $9.3 trillion.

The Bank Stock Rally Could Have Further to Run

Overall, the fourth quarter of 2025 was a very solid quarter for the Big Six US banks. While results in investment banking were mixed, equities trading was strong and wealth management emerged as a reliable anchor for the group. Encouragingly, provisions for credit losses generally fell – signaling optimism about the economy and the ability of borrowers to repay their debts – and CEOs were upbeat in relation to near-term trading conditions. This suggests that the rally in bank stocks could have further to run in 2026.

Footnotes:

1JPMorganChase, Q4 2025 Earnings Press Release, as of January 2026

2CNBC, JPMorgan Chase tops estimates as trading revenue exceeds expectations, as of January 13, 2026

3Wells Fargo, Q4 2025 Earnings Press Release, as of January 14, 2026

4Investing.com, Earnings call transcript: Wells Fargo Q4 2025 beats EPS forecast, stock dips, as of January 14, 2026

5Bank of America, Q4 2025 Earnings Press Release, as of January 2026

6CNBC, Bank of America tops estimates on better-than-expected net interest income, equities trading, as of January 14, 2026

7Citi, Fourth Quarter and Full Year 2025 Earnings Results, as of January 14, 2026

8CNBC, Citigroup tops estimates on stronger net interest income, smaller loan loss provision, as of January 14, 2026

9Goldman Sachs, Full Year and Fourth Quarter 2025 Earnings Results, as of January 15, 2026

10CNBC, Goldman Sachs tops profit estimates as equities, asset and wealth management outperform, as of January 15, 2026

11Morgan Stanley, Fourth Quarter and Full Year 2025 Earnings Results, as of January 15, 2026

12CNBC, Morgan Stanley earnings top estimates driven by wealth management, as of January 15, 2026

Author is a contractor of Leverage Shares LLC, a U.S. affiliate of Themes Management Company LLC. Leverage Shares LLC provides certain services to Themes under an intercompany services agreement.