Article by Sandeep Rao

Global Banks Post Record Q1 as Stocks Remain Undervalued

June 22, 2026 | Research Insights

The first quarter of 2026 produced a paradox: despite universally strong operating performance across the global banking sector, banks’ equity valuations sharply declined. The KBW Bank Index (BKX) posted its worst first-quarter since the 2023 mini-banking crisis1. The S&P Financial Select Sector Index (IXM) fell approximately 10% year-to-date through May 31. Yet the S&P 500 Financials sector was expected2 to deliver 15.1% EPS growth - the third-highest of all eleven sectors - above the 14.6% consensus at the start of the quarter.

Three macro shocks defined investor psychology throughout the period. First, the Iran-Israel war drove energy prices sharply higher, creating uncertainty about second-order effects on consumer balance sheets, corporate borrowing costs, and Middle East credit exposure. Second, a private credit market shakeout — involving redemption requests at Apollo, Blue Owl, BlackRock, Carlyle, and others3, most of whom imposed 5% quarterly redemption limits — raised systemic concerns about shadow banking leverage. Third, numerous industry leaders – led by Jamie Dimon – warned that the next credit crisis will be worse than people expect4. All together, these were sentiment depressants that no EPS beat could fully counteract.

Transatlantic and Japanese Banks Beat the Odds

The dominant theme across all major U.S. banks – who reported Q1 2026 results in April 2026 – was record trading revenue driven by Iran-war volatility, combined with a sharp investment banking fee recovery. One outlier was Wells Fargo, whose Net Interest Income (NII) miss exposed the fragility of a retail-heavy, interest income–dependent model.

The picture among leading international banks was, if anything, more impressive.

Note: “Verdict”, the strength of “Wealth” and “NII Trends” are qualitative assessments synthesized from analyst consensus and earnings call commentary by the banks themselves

Canada's Big Six - which report their fiscal Q1 results in late February - opened 2026 with the kind of broad-based momentum that most banking systems can only envy. RBC delivered net income of C$5.8 billion, up 13% year-over-year, with its adjusted ROE of 17.8% comfortably above its own 17%-or-better target. CIBC’s net income of C$3.1 billion surging 43% year-over-year and adjusted ROE of 17.4% overshooting its 15% medium-term target by more than two percentage points. TD Bank delivered adjusted EPS of C$2.44 with adjusted net income up 16% to C$4.2 billion. The characteristics of the oligopoly model - three or fewer dominant banks in most product categories, prudent regulatory oversight, and a culture of conservative provisioning - produced a consistent, high-quality result in Q1 2026 that stood in contrast to the volatility seen in U.S. stock prices despite stronger headline earnings. BMO and Bank of Nova Scotia similarly posted record or near-record revenues as provisions for credit losses fell sharply.

Japan's three megabanks - MUFG, SMFG, and Mizuho - reported their fiscal year results ending March 2026, and the numbers were uniformly extraordinary5. For the better part of 25 years, Japanese bank profitability was suppressed by Bank of Japan policy holding rates at or near zero. The BoJ's normalization - moving rates into modestly positive territory for the first time since the late 1990s - is reversing decades of margin compression from a very low base. Even modest NIM expansion translates into large absolute earnings gains given the scale of the Japanese banking system's domestic loan books. However, the primary risk flagged by management across all three institutions is the geopolitical dimension of the war with Iran.

The UK domestic banks produced a genuinely strong quarter that the wider market largely overlooked. Lloyds Banking Group’s posted profit before tax was up 33% for Q1 2026, with net income rising 9% year-over-year and net interest income up 8% to £3.6 billion. Management raised full-year NII guidance to above £14.9 billion and reiterated a 16%+ ROE target for 2026, which the 17% RoTE achieved in Q1 suggests is comfortably on track.

NatWest’s EPS was up 15.5% year-over-year, with a Return on Tangible Equity (RoTE) of 18.2%, and net loans growing £7.2 billion in the quarter. Net Interest Margin (NIM) expanded 2 basis points sequentially to 2.47%. Barclays delivered a RoTE of 13.5% on income that was up 6% year-over-year.

HSBC delivered a nuanced story: despite reported profit before tax marginally below consensus and operating expenses rising 8% year-over-year, the underlying momentum was solid: banking NII rose 8%, wealth fee income was strong across Asia, and the bank's annualised RoTE of 18.7% remains among the highest of the global universal banks. The miss was deemed a modest miss by the market and the reaction in the stock was positive.

Emerging Market Exposure Divides European Banking

Continental Europe delivered a tale of two models: the emerging-market (EM)-exposed Spanish giants delivered the strongest returns in European banking by a wide margin, while core European universal banks remained structurally constrained by ECB rate normalization and compressed domestic margins. BBVA was the standout and arguably the most underappreciated result in the global sector, with net profit rising 10.8% year-over-year and ROTE of 21.7% - a level that rivals the best-in-class U.S. investment banks. Santander recorded underlying profit rising 12% year-over-year (14% in constant currency), on revenue growth of 4%. The efficiency ratio improved to 42.8% - among the lowest of any global bank of comparable scale - as the ONE Transformation programme drove costs lower even as revenue grew.

BNP Paribas’ CEO Jean-Laurent Bonnafé stated that the quarter confirms “very good momentum”6, with a record net income growth of 9% year-over-year on revenue growth of 8.5%. Deutsche Bank reported record net profit of €2.2 billion, up 8% year-over-year, with all four divisions delivering RoTE at or above 13% - a milestone. Revenue grew 2% year-over-year (6% excluding FX), driven by private banking net inflows, asset management growth, and corporate bank lending. With analyst forecasts anchored to a more sceptical view, the bank is currently deemed mostly undervalued.

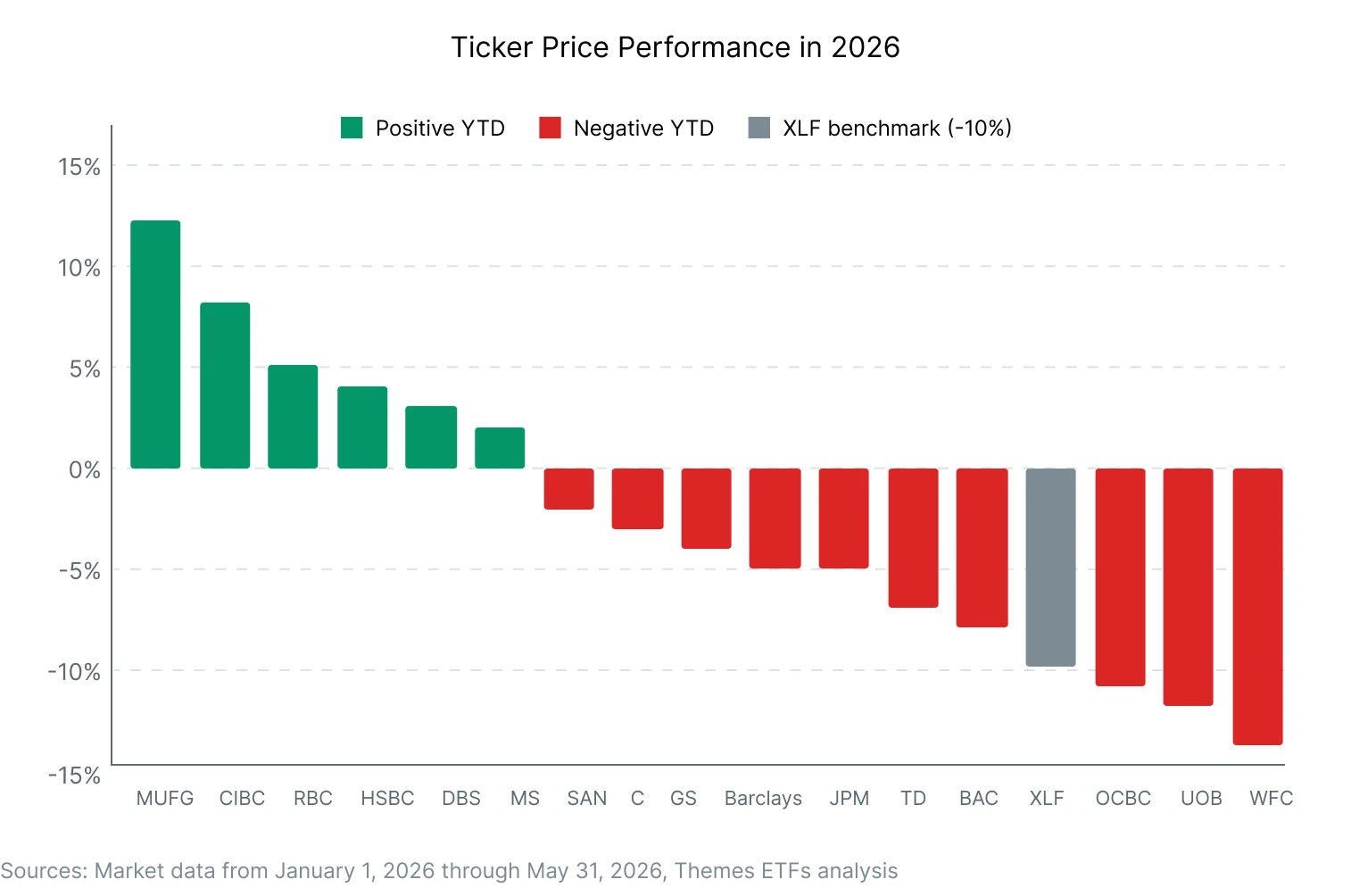

Asian Banks Versus Western Peers

When compared versus the benchmark for US financials – the S&P Financial Select Sector Index (IXM) – Asian banks delivered stronger stock price performance than their Western counterparts.

As indicated in most banks’ earnings calls, the conflict with Iran weighs more heavily on the overall business environment in the West while the East continues to hinge on growth despite the odds. Another factor that weighs heavy on the valuations are investor convictions: despite steady performance, AI-relevant stocks attract greater attention in portfolios in the West, often at the cost of buying into steady and progressively stronger performance – an often-repeated feature evident across multiple quarters.

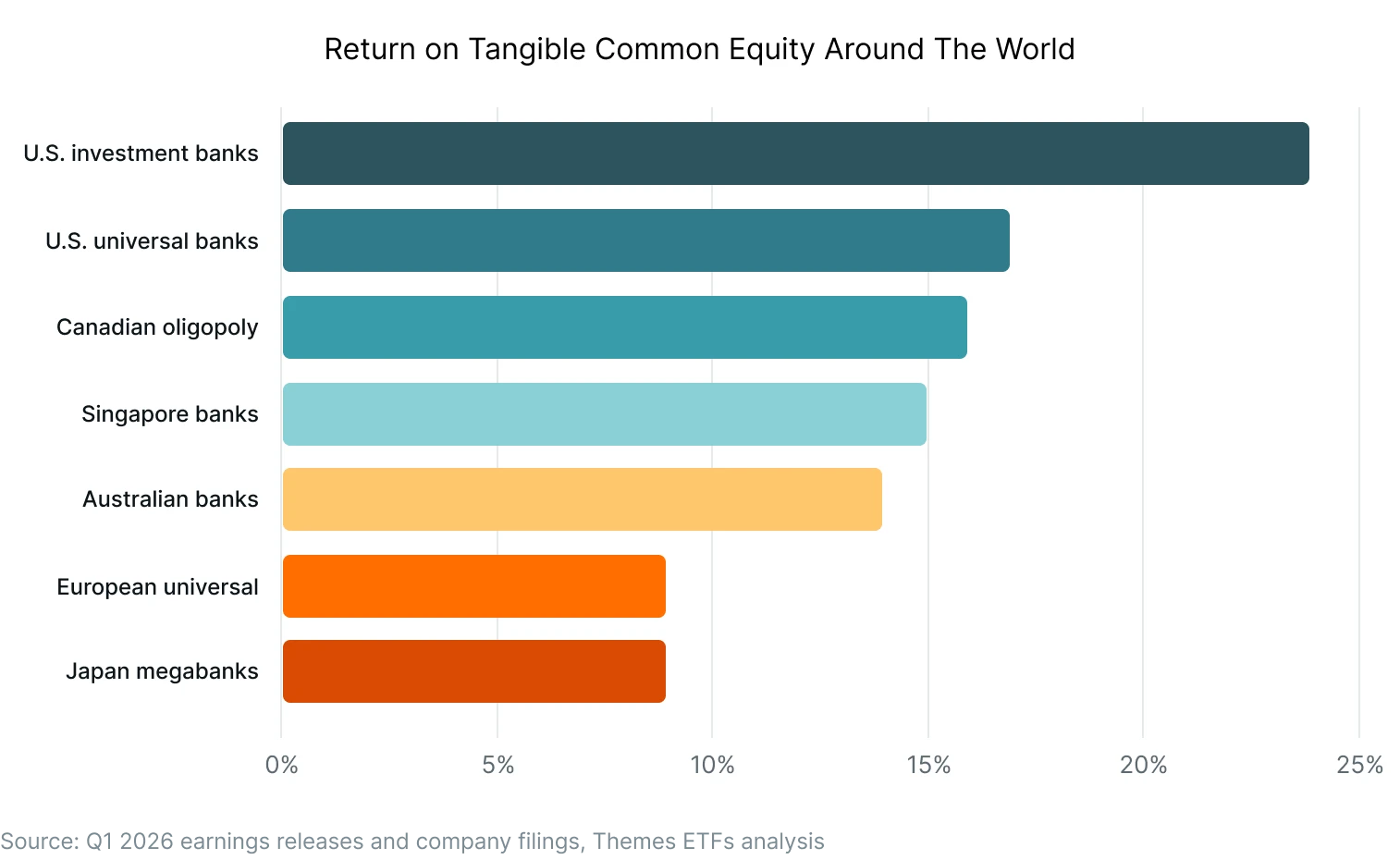

Franchise size is potentially of significant impact among European banks, where Return on Tangible Common Equity (ROTCE) runs at par with Japanese megabanks.

This is the nuance driving HSBC's simplification programme, which included the Q1 completion of its German custody disposal to BNP Paribas and the January privatisation of Hang Seng Bank. As a result of this, the bank is estimated to be on track to deliver $1.5 billion in annualised cost savings by mid-2026, with CEO Pam Kaur reiterating that the group will achieve its 17%+ RoTE target through 2028.

Outlook and Risks

On balance, Q1 2026 delivered two interesting and varied takeaways. First, the integrated investment banking and wealth management model delivers. Fee diversification provides earnings resilience across rate cycles, capital markets optionality monetizes volatility, and a wealth flywheel compounds with asset prices regardless of the interest rate environment.

Second, oligopolies – as seen in Canada and Japan – foster growth in the right environment. Canadian banks’ pricing power, regulatory protection from domestic competition, moderate credit cycles, and deep retail deposit franchises generate predictable, high-quality returns that institutional investors systematically underweight relative to their reliability. Meanwhile, in Japan, the normalization of monetary policy coupled with corporate Japan's demand for capital to fund AI infrastructure investment and reshoring provides volume growth that Japan’s megabanks are richly capitalizing on.

However, risks abound. Both US and Asian banks indicated that the conflict with Iran drives high potential for economic stress from elevated energy prices, with the full consumer and corporate credit impact yet to play out as of Q1 2026. Next regulatory evolution in the form of Basel III endgame rules, potential capital requirement changes, and the continued growth of non-bank lending create unquantifiable but material regulatory tail risk for the sector. Non-bank lending – including “Buy Now Pay Later” (BNPL) – has linkages with the health of the sector.

Nonetheless, Q1 2026 confirmed that the global banking sector is in robust fundamental health with the strongest capital positions in a generation, diversified revenue streams, and improving efficiency ratios across most major franchises. The challenge for portfolio managers isn’t fundamental but psychological: macro and geopolitical forces can decouple stock performance from operating reality for extended periods, as Q1 2026 has demonstrated with striking clarity.

Given the outlook, we believe that the Themes Global Systemically Important Banks ETF (GSIB) might merit consideration by investors seeking assets that are potentially undervalued. GSIB invests in 28 publicly-traded banks around the world that have been identified as “systemically important” by the Financial Stability Board (FSB) and the Basel Committee on Banking Supervision (BCBS) equally in a quarterly-rebalanced manner. The balanced consideration of major banks across multiple geographies can potentially mark a strong argument in favour of investment growth stability.

Important note: All numbers are estimates, based on internal Themes ETFs research analysis, compiled as of Q1 2026 earnings reports.

Footnotes:

1“Bank Stocks Have Worst Start to Year Since 2023 as Results Loom”, Bloomberg, 10 April 2026

2“S&P 500 Financials Sector Earnings Preview: Q1 2026”, FactSet Insight, 13 April 2026

3“Blue Owl limits withdrawals from two funds after historic surge in redemption requests”, Reuters, 2 April 2026

4“JPMorgan’s Jamie Dimon says a credit-led recession would be ‘worse than people think’”, MarketWatch, 29 April 2026

5“Japan’s megabanks post record profits, but analysts warn growth may slow as risks mount”, CNBC, 21 May 2026

6“France's BNP Paribas Posts Higher Profit on Retail Growth, Asset Management Integration”, Morningstar, 30 April 2026

Author is a contractor of Leverage Shares LLC, a U.S. affiliate of Themes Management Company LLC. Leverage Shares LLC provides certain services to Themes under an intercompany services agreement.