Article by Sandeep Rao

Why SpaceX’s Stock Might Slip into Double Digits

June 22, 2026 | Research Insights

On June 12, SpaceX’s IPO raised $75 billion via a $1.75 trillion valuation, thereby making it the largest IPO in history after shattering Saudi Aramco's 2019 record at nearly thrice the value. The share price soared 19% on the first day. Before trading opened on June 18, SPCX was at $191.82 after having hit an intraday high of $225.64 during the week.

By any conventional measure, the IPO “worked”. But conventional measures are precisely where the bear case has begun to build. Among arguably the most quantitatively-oriented cases being presented has been Chicago-based investment research firm Morningstar.

The Overvaluation Trap

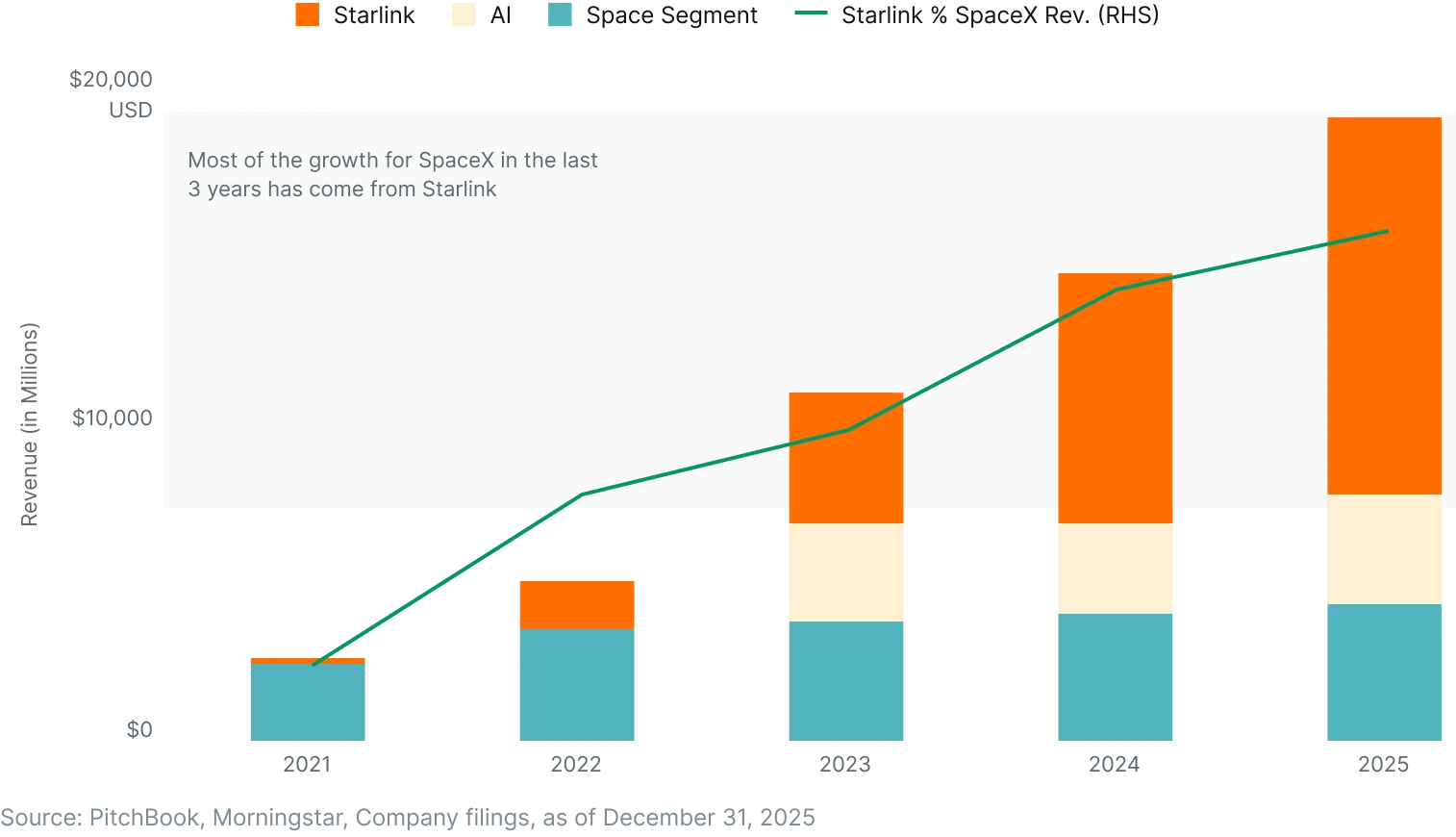

SpaceX generated $18.7 billion in revenue in 2025 and Morningstar projects1 revenues of $36.8 billion for 2026. But even at that figure, the company would only match Micron Technology’s revenue from 2025, while Amazon generated over 19 times as much. Yet, SPCX is trading2 at around 141 times its 2025 sales and nearly 78 times projected 2026 sales - with over 3 times Broadcom’s multiple and 26 times Amazon’s.

A tested bright spot within SpaceX is Starlink, which generated an estimated $15.5 billion in annual revenue run-rate as of mid-2026, with $4.4 billion in operating profit - an 85% recurring revenue stream with SaaS-like margins. The service now has over 9.2 million subscribers across 120 countries. Morningstar identified this as the most significant pillar of revenue that supports the company’s other bets.

Chief among their bets is in AI, which accounted for 93% of the Total Addressable Market (TAM) in their S-1 filing prior to the IPO. In this, Morningstar stated that Grok – xAI’s Large Language Model – doesn’t feature in the top LLM-driven services used all over the world. On the 16th, SpaceX announced that it is buying Anysphere, the startup behind the AI coding agent Cursor, in all-stock deal valued at $60 billion. While this led to a slight uptick in the share price, Morningstar promptly lowered its fair value estimate from $63 to $62 and called SpaceX one of the most expensive in its entire coverage universe.

An Elaborate Unlock Schedule

The IPO plus the "greenshoe" (a special clause in an IPO that allows underwriters to sell more shares than originally planned if investor demand exceeds expectations) exercised by investors released around 638.9 million shares of Space X, which stands at around 4.9% of total shares outstanding. Around 6.4 billion shares – approximately 35.2% – is held by early investors and employees who have a staggered schedule to receive an “unlock”, i.e. be released from an obligation to not sell their holdings in the public market.

The first schedule is timed for around the Q2 earnings in July-August wherein up to 20% of the 4.6 billion locked shares would be released (45% more than that released during the IPO). If SPCX holds above $175.50 on 5 of the prior 10 sessions, an additional 10% (around 460 million more shares) would be unlocked as well. This tranche of investors includes the likes of Founders Fund, Sequoia, Alphabet, and Fidelity – among others and this would account for up to 30% of all the locked shares, i.e. around 10.5% of total shares outstanding.

From August through October, 7% of “locked” shares will be released in five tranches every two-four weeks. This would constitute around 17.1% of total shares outstanding. All told, the first schedule will release around 12.3% of total shares outstanding.

The second schedule is timed around the Q3 earnings in October-November, wherein 28% of “locked” shares will be released. Q3 is also when underwriting banks exit their quiet period and independent research from Goldman, Morgan Stanley, and JPMorgan will goes live – which could substantially shift consensus. The second schedule will thus release around 9.8% of total shares outstanding.

After the 180-day post-IPO period, i.e. in December, the remainder of the “locked” shares are released and constitute around 2.6% of total shares outstanding.

In early 2027, a separate cohort of “extended investors” operates on a schedule running into Q1–Q2 2027 holding around 11% of total shares outstanding will be “unlocked”. The earliest window is expected to be at 280 days post-IPO (i.e. late March 2027), with further tranches at 340 and 366 days.

Throughout this period, Elon Musk’s share of 6.4 billion shares – constituting 48.9% of total shares outstanding – remains locked until 366 days post-IPO, i.e. June 12, 2027. After this, he is eligible to release shares as per his will. While Musk has stated he will not sell, even the eligibility change resets institutional risk models.

SpaceX's lockup structure is unlike any major IPO before it and deliberately engineered to avoid a single cliff-edge selloff. However, this doesn’t necessarily eliminate the pressure; it distributes it across a 12-month calendar of smaller crises. There is a precedent that proves the case: Facebook’s 2012 IPO used a staggered lockup and shares had still fallen more than 40% from the offering price by the time it concluded.

Conviction versus Fundamentals

After SPCX fell for the first time since its IPO on June 17, Gary Black – CEO of The Future Fund – remarked4 that early trading patterns resembled “a meme stock more than one driven by fundamentals”, noting that the stock's rise came in a market where selling was severely constrained. Considering the elaborate lockup schedule, it could be argued that SPCX’s currently price is partly a function of artificial scarcity and not purely fundamental conviction. Meanwhile, American investment bank Oppenheimer & Co raised5 its price target from $190 to $250, citing increased visibility for revenue, vertical integration and the AI stack, the strong moat created by a NASA-funded route to a lunar base, and more.

The moat is contested, as Morningstar holds the view that the economic moat is narrow or indeterminate – numerous companies around the world do what SpaceX does. Oppenheimer acknowledges that the key risks are “execution-related”: in other words, whether SpaceX can deliver and hold what it touted.

While index additions are generally being touted as a potential tailwind, it bears remembering that index eligibility is not the same as index inclusion – both decisions are discretionary, not mechanical. The post-IPO $225 peak, the first post-IPO dip, Oppenheimer’s lofty price target of $250 versus Morningstar’s resolute price floor at $63 – all indicate different pictures of the same company early in the public eye and does not generally constitute a strong case for index inclusion. ETFs built on broad indexes are supposed to be relatively stable; adding volatile stocks into the mix detract from this goal.

Positioning for a stock drop as the market absorbs more information, conviction shifts, and “meme stock” behaviour peters wouldn’t necessarily be premature or out of order.

Footnotes:

1“SpaceX Rally Continues, Expanding Sky-High Valuations”, Morningstar, as of June 16, 2026

2“SPCX Stock Jumps Overnight: Cursor Deal Pushes SpaceX Deeper Into 'Most Expensive' Territory, Morningstar Says”, StockTwits, as of June 16, 2026

3“SpaceX IPO Deep Dive: The Hype, the Price, and the Opportunity”, Morningstar, as of June 9, 2026

4“SPCX Stock Suffers First Post-IPO Drop: Locked-Up Shares And Missing Shorts Skewed Debut Run, Analyst Says”, StockTwits, as of June 18, 2026

5“SpaceX stock target raised at Oppenheimer. Here’s the new 12-month forecast”, Investing.com, as of June 18, 2026

Author is a contractor of Leverage Shares LLC, a U.S. affiliate of Themes Management Company LLC. Leverage Shares LLC provides certain services to Themes under an intercompany services agreement.